[ad_1]

peterschreiber.media

From bearish to neural

I initially recommended to sell the S&P 500 (NYSEARCA:SPY) on August 15th, and since then, SPY is down by nearly 15% – and it just touched the June lows. There are good fundamental and technical reasons to close the SPY short trade for now – and remain neutral.

The initial bearish thesis

This was my initial bearish thesis from Aug 15th for September.

- The 10y-3mo curve is likely to invert in September, virtually guaranteeing a recession. (This has not happened yet because the long-term rates increased.)

- The reading on core CPI for July is expected to exceed the print for June. (This in fact happened)

- The Fed to double the QT in September. (This happened and caused the higher long-term rates).

- The Phase 2 selloff of the full bear market is approaching. (This is still to come.)

In fact, I have been consistent in predicting the unfolding liquidity shock selloff in reaction to increasingly hawkish Fed monetary policy tightening. After the ultra-hawkish Fed Chair Powell speech at the Jackson Hole Symposium, the probability of a liquidity shock significantly increased. The liquidity shock selloff happens when the market prices an increasingly hawkish Fed (or it expects a sharp increase in short term interest rates). Thus, as I reiterated in this article, the liquidity shock selloff, or the Phase 1 of the bear market, was still in progress

Additionally, I have been expecting the Phase 2 selloff of the bear market as the recession approaches, which is based on the earnings downgrade and contracting valuations. In fact, the official NY Fed recession probability increased to 25% – and given that the 30% threshold usually predicts a recession, this signals a very high probability of an upcoming recession.

What happened since?

Higher short-term interest rates

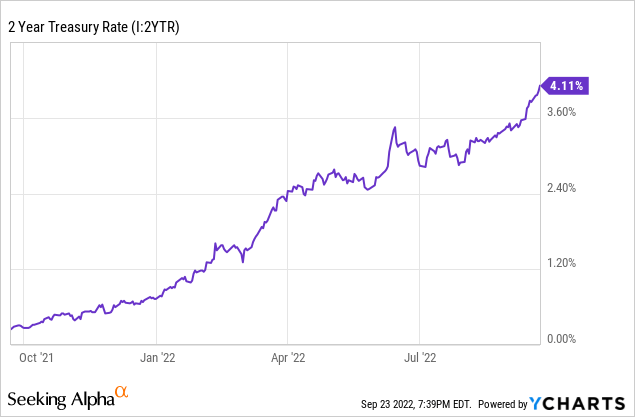

Since the Powell speech on Aug 26th, the yields on 2Y Treasury Bonds increased from around 3.25% to 4.17% (intraday) – this reflects the expectations of a more hawkish Fed tightening. In fact, on August 26th, the market expected the Fed to hike to about 3.5-3.6% by the end of 2022. As of September 23rd, the market expects the Fed to hike to 4.2-4.3% by the end of 2022 – or about 0.75% more.

Higher long-term real interest rates

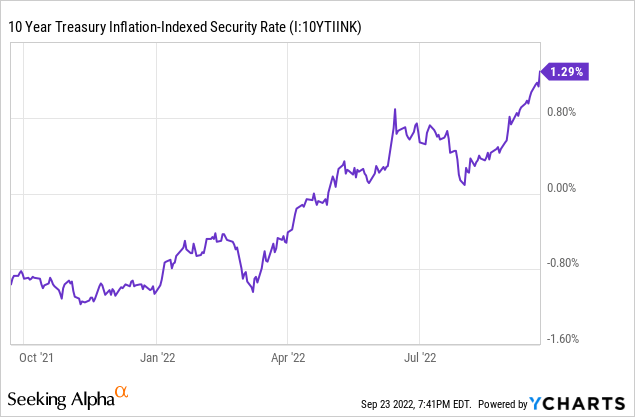

Note, also the 10-year Treasury Bond yield increased from around 3% on August 26th to 3.71% as of September 23rd. More importantly, the move higher in long-term interest rates was driven by the increase in the real interest rates from 0.47% on August 26th to 1.29% on September 23rd. This likely reflects the doubling of the QT program that started in September – which is another form of monetary policy tightening. Here is the chart of real interest rates as measured by the 10-Year TIPS yield.

Sharp correction in the stock market

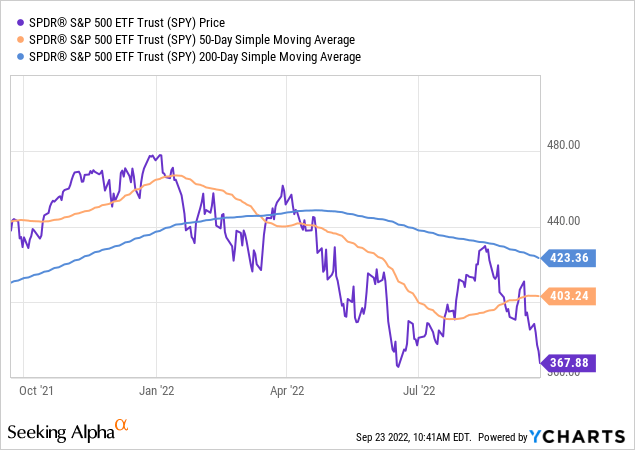

Thus, as expected, the S&P 500 sharply corrected by almost 13% since August 26th. As previously stated, this was mostly the liquidity-shock selloff or the Phase 1 of the full bear market – in reaction to the increasing expectations of the Fed hawkishness.

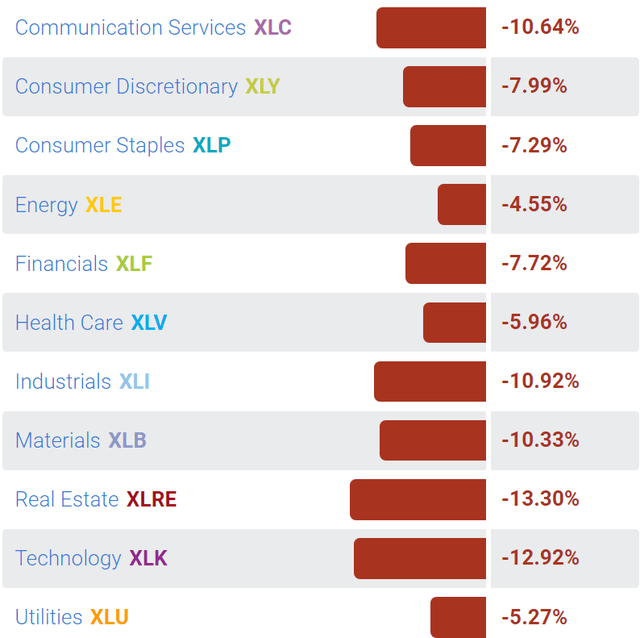

All SPY sectors sharply corrected over the last 30 days, led by interest-rate sensitive real estate sector (XLRE) and the high-beta technology sector (XLK), both of which declined by around 13%. But also note that economically sensitive sectors such as Industrial (XLI) and Materials (XLB) sectors went down by over 10% over the last 30 days. This signals that the market is possibly starting to price an imminent recession or the Phase 2 of the full bear market.

SelectSectorSPY

Why the switch from bearish to neutral now?

The Fed’s hawkishness has likely finally reached the peak.

I don’t think the Fed can be any clearer about its intentions and determination to fight inflation. More importantly, the Fed’s hiking campaign is near the end. The Fed has to signal the intention to slow the interest rate hikes first (from 0.75% to 0.50% to 0.25%) and eventually state that the Federal Funds rate is in the “restrictive” area, which is likely at the 4.25-4.5% level, or around 1-1.25% higher from here (not much higher given the recent pace of 0.75% per meeting hike). Thus, the Phase 1 selloff, or the Fed-induced liquidity shock is likely finished or near the expiration.

Technically – SPY is at the June 16th lows support

The short SPY recommendation produced the targeted profits, and the profit must be eventually booked. Tactically, closing the short position during the deep selloff near the major support (in this case at the previous lows) is preferred to waiting and being forced to cover in an uptrend – and being squeezed.

What’s next?

At this point, I am neutral on the S&P 500. I don’t anticipate another leg lower due to a more hawkish Fed, but this is always a possibility, and it is important to follow the inflation data, the geopolitical situation and the effect on crude oil prices, and the evolution of the long-term inflation expectations.

However, now we have to evaluate 1) whether the unfolding monetary policy tightening will cause the actual recession and how deep the recession will be, and 2) to what extent the market has already priced in the anticipated recession.

The probability of a recession is very high, as previously stated. With recession, the corporate earnings will have to be downgraded. More importantly, the current valuations are still high – the market has not fully priced-in the upcoming recession yet. Thus, recessionary selloff or the Phase 2 of the full bear market is likely.

Yet, the first sign of a slowing labor market could result in the market pricing the Fed’s dovish pivot, especially if it’s established that the CPI inflation has reached the peak and its downtrading. Thus, the stock market could actually start rising with negative economic data.

Let’s not forget that there is a very large short position in S&P500 futures (SPX), which will have to be covered, and the risk of short-covering rally is very high. Thus, at this point the short position is risky.

Implications

Overall, the stock market is still vulnerable to a selloff. We have not seen even the beginning of the weakening of the labor market, and it has to weaken to reach the Fed’s objective. The Phase 2 of the bear market, or recessionary selloff in likely coming. Thus, investors should remain patient. However, the timing of the Phase 2 selloff is uncertain, and the anticipation of the eventual ending of the Fed’s tightening campaign could produce a massive counter rally.

I am willing to play the counter rally on the long side or re-short. At this point I am neutral.

[ad_2]

Source links Google News