Kevin Carmichael: Maybe companies are finally ready to take the baton from Canada’s over-extended households

Article content

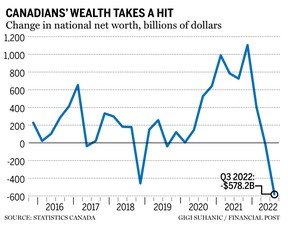

The country was more than $500 billion poorer in the third quarter, according to Statistics Canada’s latest tally of assets and liabilities, but there might be a silver lining, as there was evidence households and companies were getting ready for a recession that many economists say is inevitable next year.

Advertisement 2

Article content

National net worth — which includes Canada’s net foreign asset position — dropped 3.3 per cent, to $17.1 trillion, the biggest decline since the fourth quarter of 2008, when a wave of bank failures in the United States and Europe triggered the global financial crisis.

Article content

That’s a foreboding point of comparison. The value of residential real estate fell $287 billion, to $8.4 trillion, Statistics Canada said, while the value of natural resources plunged 13.4 per cent from the second quarter, to $2.2 trillion, as commodity prices dropped from their post-pandemic heights.

Article content

The numbers are a concern because the psychological effect of seeing so much paper wealth wiped out could dull the propensity of households and businesses to spend and invest. With the market value of their hard assets falling, households could become preoccupied with the debt they piled up chasing runaway real estate prices over the past decade.

Advertisement 3

Article content

Statistics Canada said seasonally adjusted household debt to disposable income increased to 183.3 per cent in the third quarter, up from 180.6 per cent at the start of the year, and comparable to the record of 184.6 per cent in the third quarter of 2018.

The ratio was 156.8 per cent at the end of 2008, when central banks dropped interest rates to essentially zero, kicking off the era of ultra-low-borrowing costs that ended this year when policymakers abruptly reversed course in an attempt to constrain the most threatening burst of inflation since the early 1980s.

“High household indebtedness remains a key vulnerability for the Canadian economy, and one that the Bank of Canada will monitor closely as it evaluates the impact of its aggressive rate hikes,” Shelly Kaushik, an economist at the Bank of Montreal, said in a note to clients.

Advertisement 4

Article content

The Great Recession got as bad as it did because the U.S. housing bust that preceded it destroyed consumer demand, which had been fuelled by low interest rates and debt.

Canadian debt levels today mirror the U.S. before that crash, which is why Statistics Canada’s quarterly report on the national balance sheet attracts so much attention. There was some evidence that negative wealth effects and the increased cost of carrying debt, or both, have begun influencing household consumption, which only grew 0.5 per cent in the third quarter.

Slower consumption will be necessary to get inflation under control. The Bank of Canada’s outlook predicts the economy will stall over the next several months because of slowing housing investment and consumer spending. Governor Tiff Macklem insists inflation is no longer simply about commodity prices and supply shortfalls, but also the result of “excess demand” generated by low unemployment and elevated wage increases.

Advertisement 5

Article content

“I take no pleasure in the idea that unemployment has to come up, but it is unsustainably low,” Macklem told the Toronto Star in an interview published last week. “Our economy here in Canada is overheated. We can’t just wait for these global factors to dissipate and expect inflation is going to come back down. We do need to get demand and supply in better balance.”

The severity of any downturn will be determined by the extent to which indebted households can ride it out, and whether business investment steps up to replace household consumption as the driver of economic growth. Statistics Canada’s latest wealth numbers have something to say about both.

-

Kevin Carmichael: Why Big Labour should be thanking the Bank of Canada, not bashing it

-

Kevin Carmichael: Bank of Canada has established its inflation fighting cred. Now it’s up to the numbers

-

Bank of Canada raises interest rate to 4.25% in what may be the last hike

Advertisement 6

Article content

Comparisons with U.S. household debt circa 2007 are often superficial, stopping at the headline numbers. Canadians tend to be far more credit worthy than their American cousins, and they’ve historically tended to prioritize debt payments when things start to get tight, rather than carrying on spending money they don’t have. Financial regulation is also stronger now than it was then, and Canada’s mortgage stress test will have limited the number of households who took on debt they can’t afford.

Indeed, if a recession comes, Canadian households will be facing it with a buffer. The savings rate rose to 5.7 per cent in the third quarter from 5.1 per cent in the second quarter, as disposable income increased faster than spending. That’s a remarkable number because even relatively thrifty Canadian households weren’t stashing away a lot of money ahead of the pandemic. The average savings rate over the decade prior to 2020 was 3.4 per cent, Statistics Canada said.

Advertisement 7

Article content

At the same time, non-financial private corporations are loading up on debt like never before, probably because their owners and managers sensed interest rates would only be going higher. Those companies took out non-mortgage loans worth $36.5 billion in the third quarter and $32.5 billion in the second quarter, the second- and third-highest totals on record. (Companies borrowed $69.9 billion in the first quarter of 2020, piling up low-interest debt to survive the pandemic.)

To be sure, more corporate debt could be another vulnerability. Some economists worry that low interest rates have created “zombie firms” that survive on credit lines rather than profits. But with equity markets in turmoil, a jump in non-mortgage loans could signal that companies were keen to raise capital by whatever means was available. The economy could be headed for a recession in the short term, but the energy and digital technology transitions mean companies that don’t invest now will be left behind.

After years of demonstrating a lacklustre commitment to investment, maybe Canada’s companies (and their lenders) are finally ready to take the baton from the country’s overextended households.

• Email: kcarmichael@postmedia.com | Twitter: CarmichaelKevin