By Kostya Etus, CFA, Senior Portfolio Manager, CLS Investments

In performance reports, time periods over one year are often annualized. Annualized returns may seem small, but compounded over a long period, they result in significant cumulative returns. As returns get higher and the time period stretches, small differences begin to have a more exponential impact. But it is important to note that returns do not typically exclude the impact of inflation. Inflation erodes your wealth behind the scenes, and you would be well served not to forget about it.

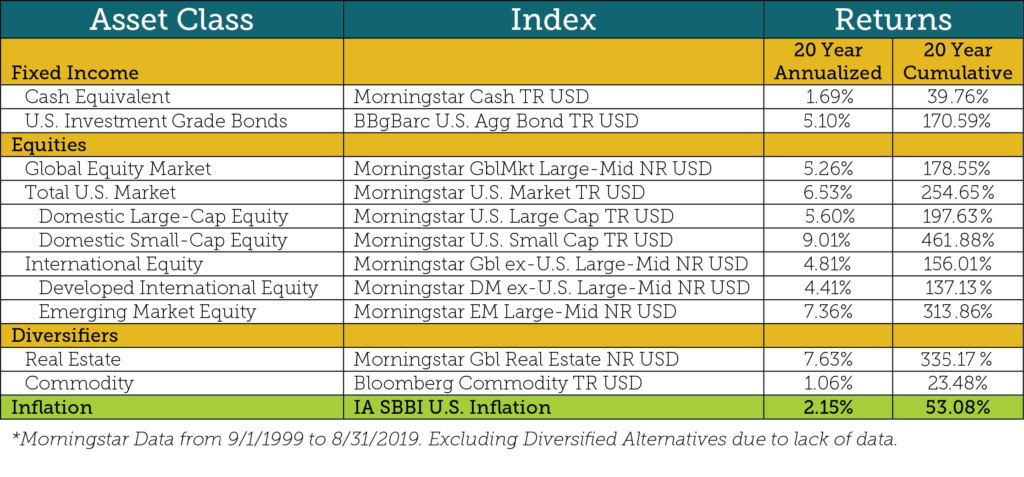

The table below shows the long-term annualized returns as well as the cumulative 20-year returns of major indices.

ANNUALIZED VS. CUMULATIVE

Investment returns for a given asset class are often stated in annualized terms. For example, the total U.S. market has had about a 6.5% annualized return over the last 20 years, which seems like a wimpy number. But that doesn’t mean your total return during the entire period is 130% (6.5% return multiplied by 20 years). The beauty of compounding is that you earn returns not only on your initial investment but also on the returns generated from last year. This really starts to add up over time. Thus, a 6.5% annualized return actually equates to a 254.7% return over a 20-year period (this means that you more than tripled your money). This is the ultimate benefit of staying invested for the long term.

INFLATION – THE SILENT KILLER

The safest place for your hard-earned cash may appear to be under your mattress (or at least in a safe), but the truth is you must take on at least a little bit of risk to avoid losing money. The reason: inflation, i.e., the constantly rising prices of goods and services. For example, the average cost of a movie ticket in 1999 was $5.08; by 2018, it was $9.11.

Over the last 20 years, aggregate annualized inflation has been about 2% per year. But let’s not forget about compounding, which means that 2% creates a cumulative increase in prices of more than 50%. Keeping your money in the bank would have earned you an annualized 1.7%, or 39.8% cumulative, over that same time period. That is less than the rate of inflation, meaning you would have lost money simply by leaving it in the bank.

EXPONENTIAL STRENGTH

As annualized returns get higher and the time period stretches, even small differences can have a large impact on cumulative returns. For example, emerging markets (EM) returned an annualized 7.4%, while U.S. small-caps returned 9.0%. That’s an increase of just under 2% (remember that 2% inflation compounded to about 50%). But the cumulative returns are 313.9% for EM and 461.9% for small-caps. That’s almost a 150% difference! Much higher than inflation at 50%. So, the next time you are comparing annualized returns, be mindful that a small increase can have exponential benefits when compounded over the long term.

As Albert Einstein famously said: “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

Kostya Etus, CFA, is a Senior Portfolio Manager at CLS Investments, a participant in the ETF Strategist Channel.