Intro: A Rare Divergence In Oil Stocks And Oil Prices Is Creating An Investment Opportunity

The XLE ETF (XLE) is a market-cap-weighted, exchange-traded fund that invests primarily in US energy companies along with some energy equipment and services firms classified as “oil and gas” by GICS. Since a big chunk of XLE is concentrated in oil majors like Exxon Mobil (XOM), Chevron (CVX), and Schlumberger (SLB), I think viewing XLE as a basket of oil stocks is fair.

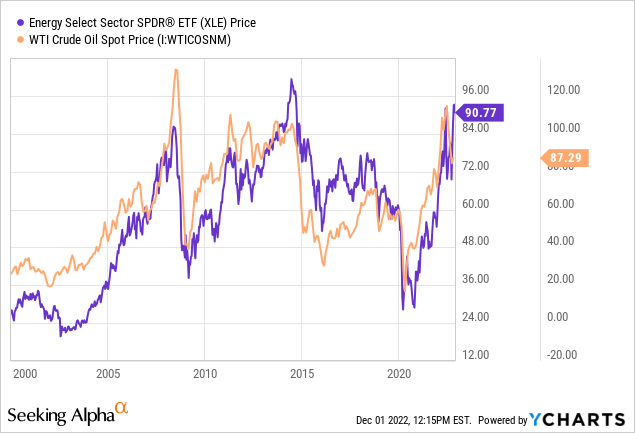

As you may know, oil and oil stocks have a deep historical relationship. Generally speaking, when oil prices are high, oil stocks tend to be high as well, and when oil prices are low, oil stocks tend to be low. This is because investors tend to invest more money in oil stocks when they expect the price of oil to rise, and they sell off their holdings in oil stocks when they expect the price of oil to fall.

Data by YCharts

That said, the relationship between oil prices and oil stocks is not straightforward. The prices of oil stocks may not move in lockstep with the prices of oil, and they may not always rise and fall together.

In some cases, falling oil prices may be accompanied by rising stock prices for oil companies (this is what we are experiencing right now). This divergence may be due to expectations that the oil companies will be able to weather the storm and maintain profitability, even with lower oil prices.

Another potential reason could be that investors may be piling into energy stocks for the sake of dividends (and/or stock buybacks), and since commodity investors/traders are looking for capital gains, oil is not catching a bid.

Additionally, there could be a multitude of unpredictable macroeconomic and geopolitical factors at play, such as the ongoing war in eastern Europe, production cuts from OPEC+ (or lack thereof), lockdowns in China, and the looming threat of a global recession. In such a situation, it is not necessarily surprising that oil stocks would rise even as oil prices fall.

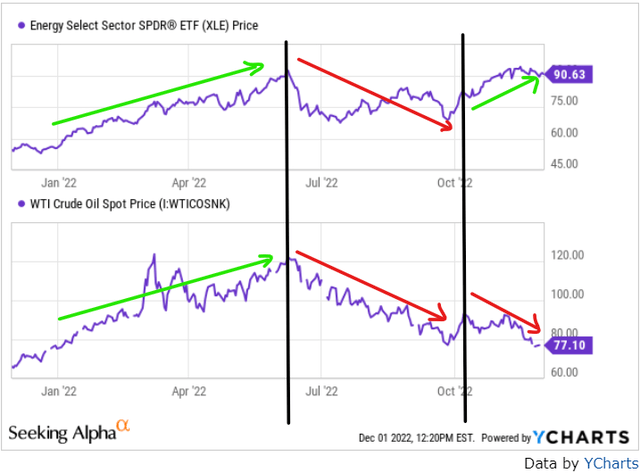

As you can see on the chart below, such a divergence is happening right now:

YCharts, Author

Going into 2022, oil prices were climbing higher across the globe primarily due to a stronger-than-expected economic re-opening after the horrors of the COVID-19 pandemic had ravaged oil demand and prices in 2020. A lot of helicopter money was printed out of thin air to deal with the COVID crisis, and the continuation of such extremely loose monetary and fiscal policies stoked multi-decade-high inflation across the globe. And then Russia invaded Ukraine in February 2022 to make matters worse!

As a result of concerns about the stability of the global energy supply amid coordinated sanctions on Russia’s oil and gas industry from the West and its allies, oil prices kept soaring higher, with WTI crude oil hitting $125 per bbl by March 2022. As oil rocketed higher, oil stocks (XLE) followed suit as investors warmed up to an industry that had been in the gutter for years before this ongoing inflationary episode.

However, the withdrawal of fiscal and monetary stimulus to fight inflation is stoking fears of a recession, i.e., a decline in demand for oil. Furthermore, China is still struggling with COVID, and the second-largest economy in the world once again finds itself in widespread lockdowns due to the draconian COVID-zero policies of the Chinese government. While these demand-side factors, in concert with Biden’s oil releases from US’s strategic petroleum reserves, are creating downward pressure on oil prices.

Since peaking out in mid-2022, oil prices have been declining throughout the second half of this year. When this decline in oil started, oil stocks moved lower in tandem until mid-October 2022. The historical relationship between oil and oil stocks was holding up quite well. However, In the last month or so, oil has continued lower, but oil stocks have rallied higher. As you can see above, XLE is now sitting at record highs, whilst the oil price is sitting way below its recent peak.

As of now, there is a massive divergence between oil and oil stocks. And historical data shows that such a divergence is a rare anomaly. Sooner or later, this divergence will be resolved in one of three ways –

1. Oil prices go up, and Oil stocks go down

2. Oil prices stay flat, and Oil stocks go down

3. Oil prices go down, and Oil stocks go down even more

In my view, the third scenario is the most likely one to materialize.

Let’s find out why.

Inflation, Recession, Crude Oil, Energy Stocks, and More

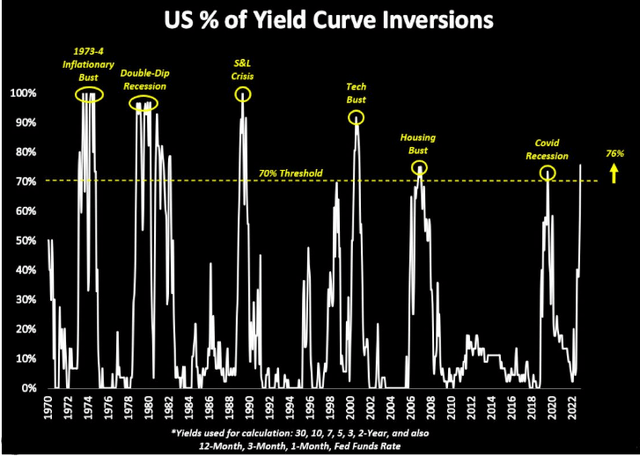

An aggressive Quantitative Tightening program from the FED has seen federal funds rates jump up from near-zero to ~4% in the space of just a few months. While inflation is starting to show signs of rolling over, leading economic indicators are flashing warning signs of a recession in 2023. And to make things worse, the FED is hiking into a heavily inverted yield curve.

I recently discussed these factors in my 2023 outlook note for tech stocks, where I also said the following:

At November’s FOMC meeting, the FED raised rates by another 75 bps to 3.75-4%, and the projected hike for the December meeting now stands at 50 bps (with recent CPI prints showing signs of cooling down in inflation). While many market participants see slower rate hikes as the beginning of the end of this ongoing rate hike cycle, I think these investors are ignoring the fact that the FED is still looking to tighten into a massively inverted yield curve.

Bloomberg

As inflation cools down, the FED could go slower from here on rate hikes; however, the FED’s resolve to hold rates higher for longer at terminal rates of 5-5.25% is dangerous for the economy.

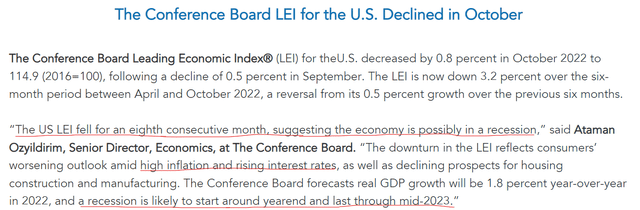

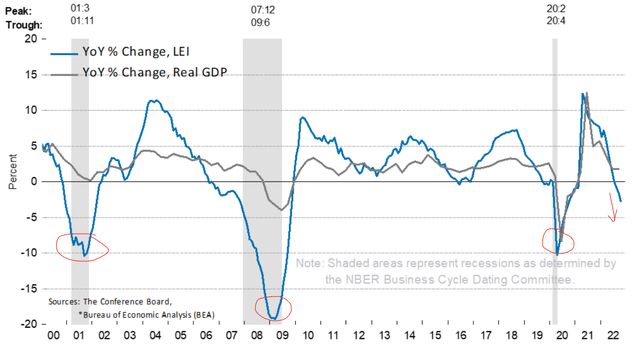

As per leading economic indicators, the US could be about to enter a recession in the first half of 2023. For months, I have insisted that recession is a far greater threat than inflation, and considering the FED’s aggressive monetary tightening actions, I think we are likelier to see a hard landing in the next few months. An earnings recession is coming, and even in a garden variety recession, we tend to see a 15-20% contraction in EPS.

The Conference Board

The Conference Board

Now, technology companies (not stocks) have traditionally shown secular growth, i.e., less vulnerability to economic cycles. However, unlike 2007-08, technology is now ubiquitous, and big tech giants are severely exposed to economic cycles, as evidenced by the ongoing growth slowdown and earnings recession seen in their Q3 reports:

PE Ratio

Forward-PE Ratio

Q3 Revenue Growth (y/y)

Q3 EPS Growth (y/y)

Apple (AAPL)

22.65x

22.08x

+8.14%

+4.03%

Microsoft (MSFT)

23.86x

23.21x

+10.60%

-13.28%

Amazon (AMZN)

83.61x

82.6x

+14.70%

-9.68%

Tesla (TSLA)

64.10x

49.91x

+55.95%

+97.92%

Alphabet (GOOGL) (GOOG)

17.19x

17.97x

+6.10%

-24.29%

Meta (META)

8.65x

9.99x

-4.47%

-49.07%

Unlike technology, the oil and gas industry is cyclical by nature. oil prices are typically cyclical, meaning that they go up and down based on economic cycles. This is because oil is a commodity, and its price is determined by supply and demand.

When there is more oil demand than supply, the price goes up.

When there is less oil demand than supply, the price goes down.

In a recession, consumers and businesses cut back on spending, which leads to a drop in demand for oil. As demand drops, so do oil prices and oil stocks. Now, I have heard a lot of arguments that oil companies will print cash above $60 per bbl and that oil stocks are still cheap on a P/E basis.

However, cyclical stocks appear to be the cheapest at the peak of market cycles, and the same is true for oil stocks. Yes, the dividend yields are attractive, but when the economy turns bad, oil prices tank, margins collapse, and dividends decline. Some dividend aristocrats from the oil industry will keep paying those dividends, but that will happen at the cost of their balance sheet strength.

In summary, oil prices and oil stocks generally fall during economic recessions, and that’s where we are headed. This is because demand for oil falls as people and businesses reduce spending, leading to lower oil prices. Oil stocks also fall because profitability (and free cash flow) declines, and investors sell out of them to raise cash to invest in more defensive sectors like Healthcare or Utilities to guard against the recession.

Even if the economy stays resilient next year, I would still expect the divergence between oil and oil stocks to close out eventually. Why? If oil prices are low, producers won’t invest in capacity expansion, curtailing the supply of oil. When the demand-supply equilibrium tilts in favor of demand, oil prices go up, and any divergence between oil and oil prices closes out.

How To Benefit From This Divergence In Oil And Oil Stocks?

In my view, the following pair-trade strategy is a great way to play the divergence between oil and oil stocks:

Buy Oil (USO), Short Oil Stocks (XLE)

For the purpose of this note, I am using US oil Fund as a proxy for oil.

A pair trade is an investment strategy that involves two correlated assets, with a long position in one asset and a short position in the other asset. The goal of a pair trade is to profit from the price difference between the two assets. For example, if an investor buys oil [via US oil ETF] and sells oil stocks [via XLE ETF] in the same dollar amounts, then he/she will have a positive return when the divergence between the prices of oil and oil stocks is resolved (in any of the three ways we discussed earlier in this note).

Final Thoughts

For over two decades, the prices of oil and oil stocks have moved in tandem with each other. I am confident that the current oil and oil stocks divergence is a fantastic opportunity for traders and investors to make money. While I can’t predict the exact timeline for this divergence to close out, I think the suggested tactical pair trade could yield rewards within the next 12-18 months.

Key Takeaway: Buy oil (USO) and short oil stocks (XLE)

As always, thank you for reading, and happy investing. Please feel free to share any questions, concerns, or thoughts in the comments section below.

, Short Oil Stocks (XLE) (NYSEARCA:USO)")