[ad_1]

choness/iStock via Getty Images

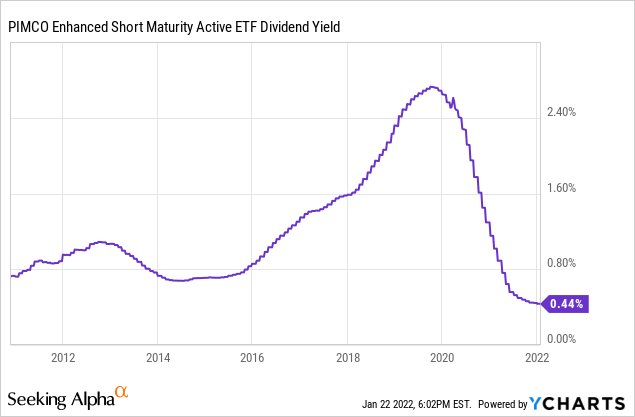

The PIMCO Enhanced Short Maturity Active Exchange-Traded Fund (NYSEARCA:MINT) is an actively-managed high-quality, ultra-low duration bond ETF, meant to act as a replacement to cash and cash alternatives. Although the fund has its merits, lower interest rates have caused its dividend yield to plummet to 0.44%, an extremely low figure. At this point, the fund offers investors only marginally higher yields than most savings accounts or bank CDs, with more volatility. In my opinion, although the fund is not a bad investment per se, it does not offer sufficient benefits to warrant an investment. For most investors, leaving their money in the bank is a simpler, more appropriate choice, and looking for a particularly attractive CD rate a better use of their time.

MINT Basics

- Investment Manager: PIMCO

- Dividend Yield: 0.44%

- Expense Ratio: 0.36%

- Total Returns 10Y CAGR: 1.43%

MINT Overview

MINT is an actively-managed high-quality, ultra-low duration bond ETF. It is administered by PIMCO, the most successful fixed-income investment managers in the world. PIMCO bond funds tend to be quite good, but the company can only do so much with rock-bottom yields.

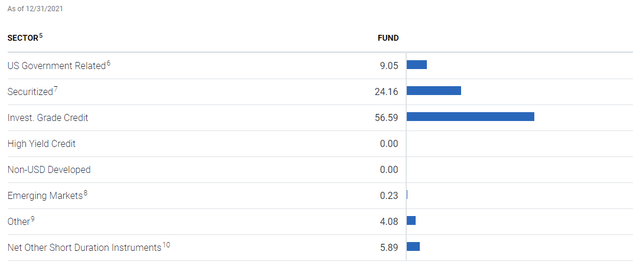

MINT itself invests in investment-grade U.S. bonds, focusing on high-quality corporate bonds, with a smaller allocation to U.S. treasuries and similar. The fund currently holdings 717 different securities. Asset allocations are as follows.

MINT Corporate Website

MINT’s holdings are almost all short-term securities, with an average maturity of 0.85 years, effective duration of 0.78 years.

MINT Corporate Website

MINT’s holdings are almost all extremely safe securities. U.S. treasuries and other government-backed securities have effectively zero credit risk: the U.S. Federal Government is the most credit-worthy institution in the world, and is at no real risk of bankruptcy. U.S. investment-grade bonds are incredibly safe too, especially considering their short maturity dates. Companies like Apple (NASDAQ:AAPL) and Microsoft (NASDAQ:MSFT) are at no material risk of default, and if they do go default it will almost certainly be a long, drawn process, not something that occurs in the coming months.

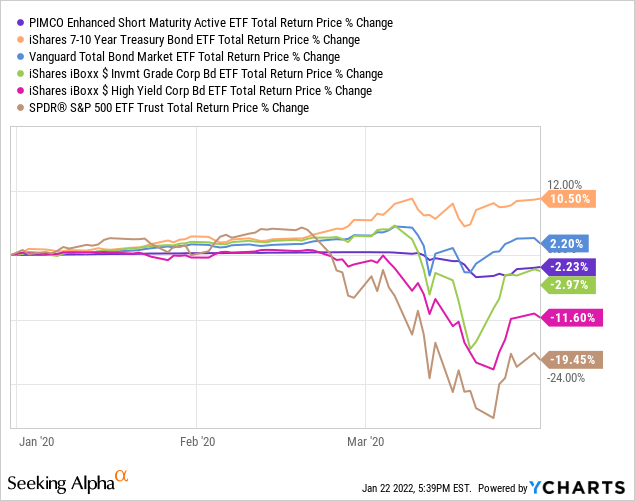

Due to the above, MINT should perform reasonably well during downturns and recessions. This was the case during 1Q2020, the onset of the coronavirus pandemic, during which MINT outperformed most bonds, bond sub-asset classes, and equities. The fund did underperform relative to treasuries, due to a flight to quality effect.

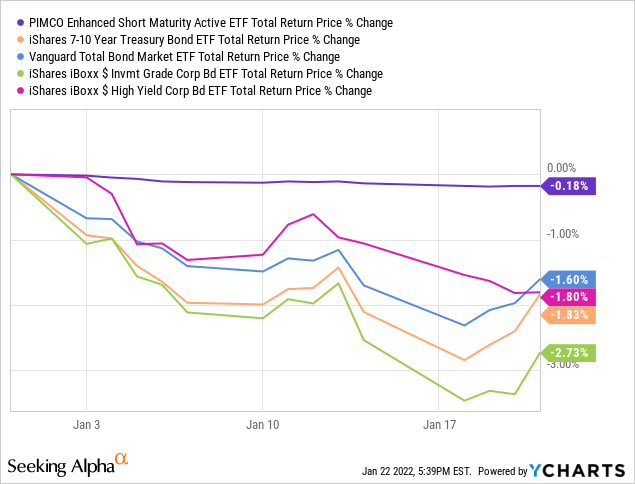

MINT should also perform comparatively well during periods of rising interest rates, as has been the case this past month. The fund underperformed relative to high-yield bonds, as these securities tend to trade alongside broader economic conditions, not just rates.

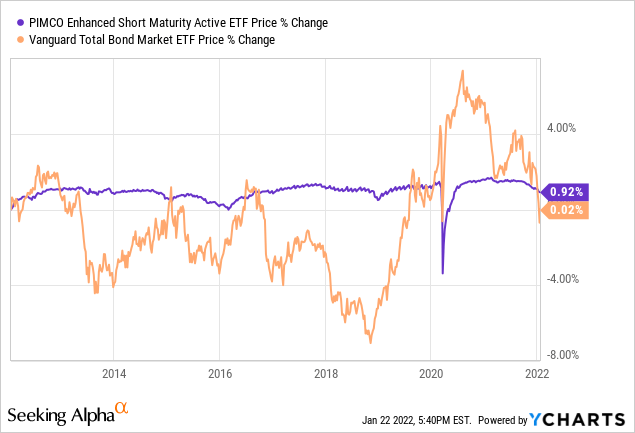

As MINT has almost no credit or duration risk, overall volatility and risk are both quite low. The fund tends to trade with a very stable price, of between $101 and $102. Volatility is low, and losses rare and short-lived.

Due to the above, MINT is used by investors as an alternative to lower-yielding savings accounts, CDs, and other similar extremely low-risk assets. The fund is generally a good alternative to these other products, but that is less true now than for most of the fund’s history. Due to the coronavirus pandemic, the Federal Reserve has slashed short-term rates to effectively zero. This, combined with a strong economy and government support / stimulus, has caused yields on short-term investment-grade corporate bonds to collapse. As MINT focuses on these securities, the fund’s yield has collapsed too, and currently stands at 0.44%, a historical low.

MINT’s ultra-low dividend yield means that the fund no offers investors meaningfully stronger income relative to cash or most cash alternatives. In my opinion, an extremely safe fund with a dividend yield of +1.0% has its uses, and this was the case for most of MINT’s history. An extremely safe fund with a dividend yield of 0.44% does not, as this is simply not a material yield. For most investors, a savings account is simpler, less of a hassle, and safer to boot.

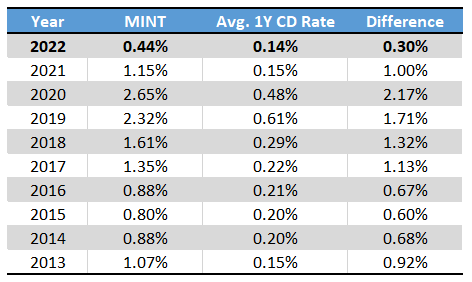

To illustrate the above, I thought it would be interesting to compare MINT’s historical dividend yield with the average 1Y CD rate, a close analogue to the fund. MINT yields 0.30% more than the average 1Y CD rate, the smallest difference in the fund’s history, and by far.

Bankrate

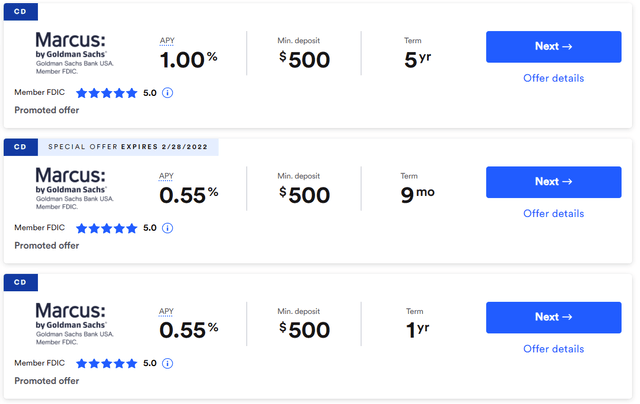

Importantly, the above are average CD rates. Different banks have different rates, and there are sometimes special offers. Marcus, the retail arm of Goldman Sachs (GS), is offering a special rate of 0.55% for new costumers, and so are other banks. MINT is fine, but if investors really wish to scalp a couple extra tens of a percentage point for their cash holdings there are better choices out there, at least under current market conditions.

Bankrate

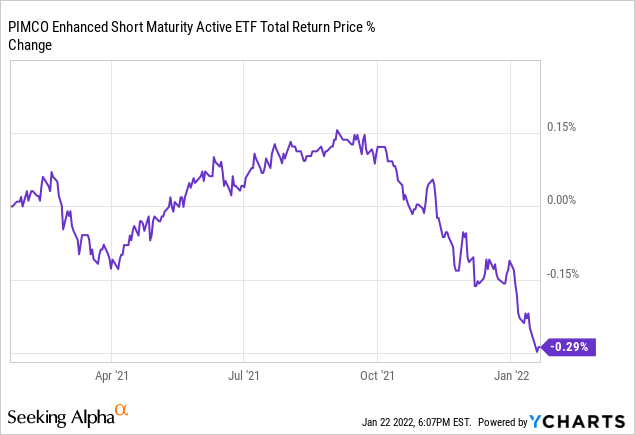

MINT’s paltry 0.44% dividend yield also comes with a tiny amount of risk, and the risks, tiny as they are, seem to outweigh the benefits. MINT’s holdings do sometimes see losses, and these could plausibly outweigh the fund’s paltry yield. As an example, the fund is down 0.29% on a total return basis these past twelve months, due to capital losses from lower bond prices. These are tiny losses, but very real, and cut against the fund’s overall investment thesis and value proposition.

MINT is likely to see further capital losses as the Federal Reserve hikes rates. These losses should be tiny, as the fund focuses on short-term investment-grade bonds, but could easily outweigh the fund’s dividends. In my opinion, MINT’s higher dividend yield does not adequately compensate investors for these added risks.

On a more positive note, the fund should start seeing higher dividends as the Federal Reserve hikes rates. As the fund focuses on short-term bonds, it should be able to quickly replace its maturing low-yield bonds for newer higher-yielding alternatives, leading to rapidly increasing dividends. Due to this, I believe that the fund will offer investors a materially stronger yield and overall value proposition in the coming months, and could then be an interesting investment opportunity.

Conclusion – Not a Buy At These Levels

MINT is a short-term investment-grade bond ETF, which functions as an alternative to cash, savings accounts, and similar investment vehicles. The fund’s current 0.44% dividend yield is not materially higher than that of the fund’s peers, nor does it adequately compensate investors for its increased risk. As such, I would not be investing in the fund at the present time.

[ad_2]

Source link Google News