")

[ad_1]

Petrovich9/iStock via Getty Images

In my previous article on the Vanguard Growth ETF (NYSEARCA:VUG) I argued that we were near a peak in the extremely overvalued growth segment of the U.S. market. After rallying another 10% to new all-time highs in November, the ETF has since posed a series of lower highs and lower lows, and I believe a bear market has likely begun. While the VUG holds the who’s who of great American companies that will likely remain market leaders for years to come, there is always a fair price for any asset, and at 39x trailing free cash flow, this ETF is anything but fairly valued.

The VUG ETF

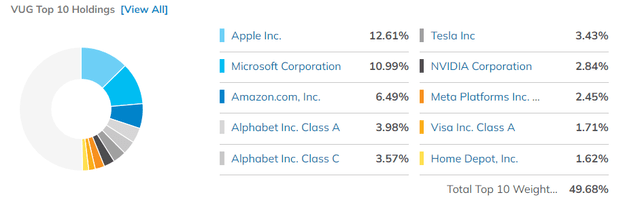

The VUG seeks to track the performance of the CRSP U.S. Large Cap Growth Index, which selects stocks based on six growth factors: expected long-term growth in earnings per share, expected short-term growth in earnings per share, 3-year historical growth in earnings per share, 3-year historical growth in sales per share, current investment-to-assets ratio, and return on assets. As a result, the Technology and Consumer Cyclicals hold a combined weighting of 78%. Fully 38% of the index comprises of the ‘Big 4’; Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), and Google (GOOG)(GOOGL), while Tesla (TSLA) commands a 3.4% share.

ETF.com

Compared to the Vanguard S&P 500 Growth Index (VOOG) the VUG has greater exposure for mid cap companies, with a median market cap of USD354bn versus VOOG’s USD735bn. Another minor difference is the VUG’s dividend yield is just 0.5% versus the VOOG’s 0.6%. However, as both ETFs are dominated by the tech giants, the two have moved in lockstep over the past 10 years.

39x Free Cash Flow Requires Continued Exponential Growth

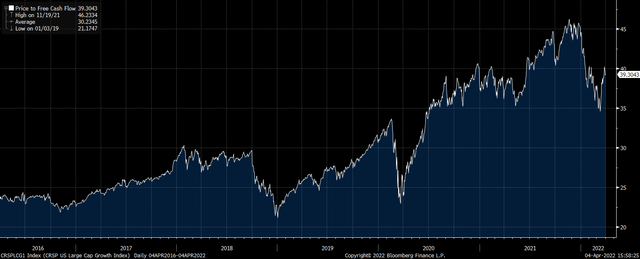

The VUG’s underlying CRSP U.S. Large Cap Growth Index currently trades at a price/free cash flow ratio of 39.3x, which is 20% higher than at the pre-Covid peak of 33.0x. When looking at the past 10 years annualized free cash flow growth rate of 9.0%, a case could be made that current valuations are justified by this exceptional growth track record.

CRSP U.S. Large Cap Growth Index: Price/Free Cash Flow (Bloomberg)

However, there are two key considerations to keep in mind when using past growth performance to value high-growth stocks. Firstly, profit margins have risen at an annualized rate of 4.0% over the past 10 years, leaving the current profit margin at a near-record 15%. Secondly, the 5% annualized sales growth over the period has been the result of the U.S. tech sector increasing its revenues as a share of the overall economy and the S&P 500. Total revenues for the CRSP U.S. Large Cap Growth Index now exceed USD4trn, equivalent to almost 30% of the entire S&P 500.

Therefore, in order for the CRSP U.S. Large Cap Growth Index to continue growing free cash flows at its historical 9% growth rate, we would need to see both a continued increase in profit margins and a continued increase in revenues relative to the overall market and U.S. economy. Considering the host of antitrust bills in the pipeline aimed at curtailing the influence of Big Tech, the headwinds facing globalization amid rising geopolitical tensions, and the ongoing strength in the U.S. dollar, the incredible surge in the CRSP U.S. Large Cap Growth Index profitability looks set to slow sharply. Furthermore, as I argued in ‘SPX: Expect A Bear Market In Profit Margins‘, there are important structural headwinds facing U.S. corporate profitability stemming from the country’s low and falling savings rate.

Rising Rates And Extreme Valuations Mean A Wafer-Thin Risk Premium

Even if profit margins remain at their current record high level and revenues continue to grow at their historical rate of 5%, this would leave the CRSP U.S. Large Cap Growth Index overvalued for years, if not decades, to come. When considering the paltry dividend yield of 0.5%, this means that investors in the VUG should expect to receive total returns of around 5.5% even if valuations remain at current extreme levels indefinitely.

While a 5.5% annual return may seem reasonable in the context of still-low interest rates, it is worth noting that the post-WWII annualized nominal total return on U.S. stocks has been 11.0%, versus a 5.3% return on U.S. 10-year Treasuries, which equates to an equity risk premium of 5.7%. After the recent rise in bond yields, the 10-year Treasury currently yields 2.4%. This means that if VUG returns are expected to come in at 5.5% annually, the current equity risk premium is just 3.1%, just over half of its long-term average.

While stocks are rising, little attention gets paid to the risks inherent in high-flying growth stocks, but keep in mind some simple maths. If investors were to require an equity risk premium on the VUG of 5.7% in line with the long-term average for the S&P 500, the dividend yield would have to rise to 3.1% based on current Treasury yields and assuming 5% long-term profit growth. This would require an 84% decline in stock prices. This is by no means a forecast, but it should highlight the risks of buying extremely expensive stocks, particularly amid rising interest rates.

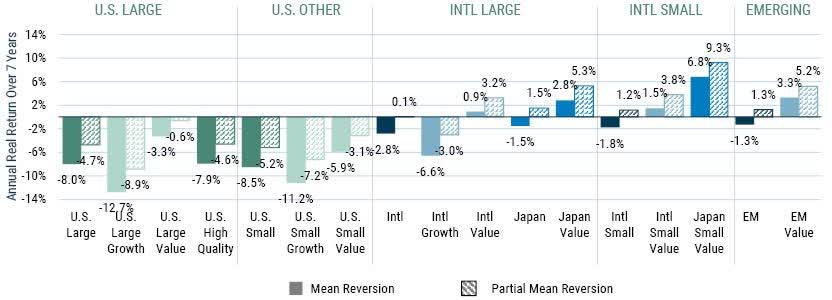

To be clear, my short positions in the VUG are not held in isolation, but form part of an overall portfolio designed to benefit from a narrowing in the valuation gap between U.S. growth stocks and international value stocks, while reducing overall volatility. The below chart from the value-focused investment management team at GMO, while slightly out of date, highlights what they see as being a truly historic opportunity to benefit from such a reversal of fortunes in the value/growth space.

GMO 7-Year Asset Class Forecast, Real Annual Returns (GMO)

[ad_2]

Source links Google News