[ad_1]

Antoine2K/iStock via Getty Images

Over the last couple months, I have spent a lot of time following current events, supply chains, and markets. One of the things that gets me wound up is the US energy policy. We have consistently made the wrong decisions over and over for years, and now we are going to pay the price. Consistent underinvestment in fossil fuels through government and manipulative ESG policies have led to supply issues which might mean that high oil prices don’t actually cure high prices this time.

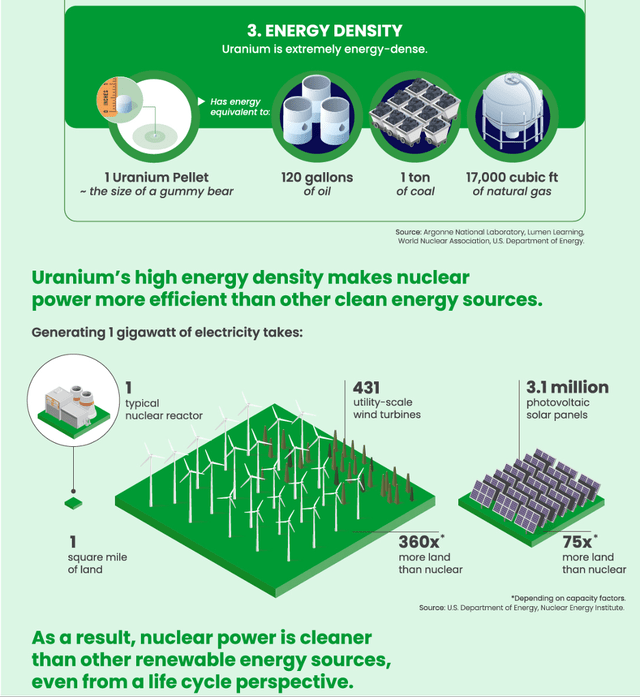

While oil is the most important commodity in the world economy, another commodity that typically flies under the radar came to my attention. I’m talking about uranium. I assume most readers had the same knee jerk reaction that most people have when they think of uranium or nuclear power. Pictures of mushroom clouds and the aftermath are the default for most people. However, uranium and other radioactive materials are the most logical way to meet base load power demands. Best of all, uranium is extremely energy dense, and it is by far the cleanest source of energy in the world.

Energy Density (visualcapitalist.com)

While the government has spent the last decade subsidizing dumb energy (my personal tag for solar and wind), uranium has been hiding in plain sight as the obvious choice. Proponents of solar and wind don’t bother to factor in the energy it takes to create, transport, and setup these forms of energy. They are uneconomical and a bad option for baseload power, while uranium has the potential to bring our energy grid into the 21st Century. It might take another decade or two, but I will say that it’s better late than never.

Investment Thesis

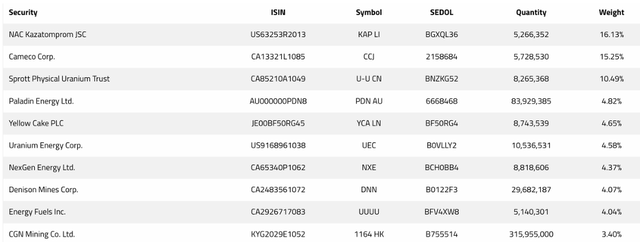

The North Shore Global Uranium Mining ETF (NYSEARCA:URNM) was recently acquired by Sprott (SII), an asset manager focused on physical assets in the mineral space. Investors looking to participate in the coming uranium bull market might want to consider a small position in URNM. Uranium is the logical solution to the coming energy crisis and investors can get a piece of the action with URNM. The capital flows into the sector are just beginning and could provide significant upside for investors that get into positions now. I will include a brief summary of the three largest positions, which are Kazatomprom (KAP.LI), Cameco (CCJ), and the Sprott Physical Uranium Trust (OTCPK:SRUUF).

The ETF

Normally I don’t like ETFs because I am not a big fan of paying institutions to invest my money. I plan to make an exception for URNM. Sprott isn’t the typical Wall Street institution. It is based in Canada, and they have considerable experience and expertise in the commodity sector, with multiple physical commodity trusts and several other ETFs. While the Seeking Alpha page shows that there is no dividend currently, URNM paid out $4.82 for 2021. That is a yield over 6% if the payout stays the same in 2022. I won’t make predictions on the payout, but if uranium prices keep going higher, we could see a juicy dividend in 2022.

Top 10 Holdings (sprottetfs.com)

For a 0.85% fee, investors can get exposure to uranium miners, which are poised for a good run over the next couple years. Investors also get positions in physical uranium trusts which are simply bets on the price of the underlying commodity. Sprott has it set at 82.5% miners with the remaining 17.5% invested in physical trusts and royalty companies. They rebalance the ETF on a semiannual basis. In my opinion, the price of the uranium is a one-way train about to leave the station which could lead to explosive upside for investors buying today.

Kazatomprom

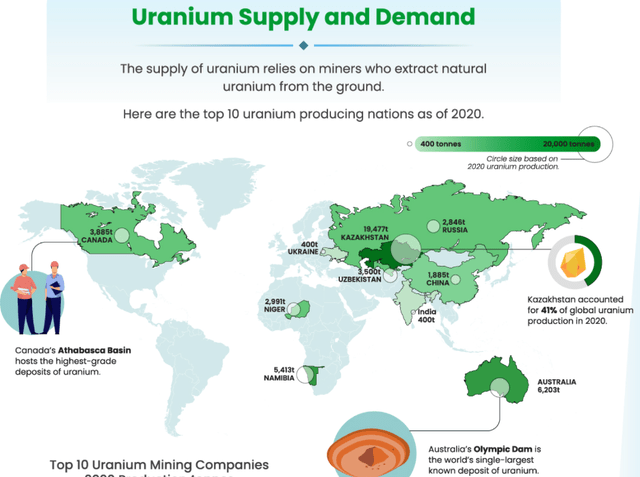

I will start the with the largest and lowest cost producer in the world, which is Kazatomprom. This has allowed them to stay profitable in the last couple years with lower uranium prices. Depending on your source, their cost per pound is in the $10-$12 range. Other companies need higher prices to turn a profit. The company has significant influence on the global uranium market, and I have heard investors compare Kazakhstan to OPEC when it comes to uranium.

Global Uranium Supply (visualcapitalist.com)

With over 40% of world production, they are a dominant player in uranium. Unfortunately, Kazatomprom is difficult to buy for American investors. The KAP.LI ticker is a GDR that trades on the London markets. The company also has a decent dividend, but due to the variable nature of the company’s dividend policy, it’s hard to pinpoint a yield. If you take Yahoo Finance at their word, it will be a 4.3% dividend.

I called Schwab to see if it was available, but unfortunately, it’s not an option for me. If your brokerage allows you to buy Kazatomprom and you’re interested in adding exposure to the uranium sector, it’s a no brainer. If I was able to buy Kazatomprom, it would probably be the first and only company I would buy. Their uranium deposits and market share mean that they will be a driving force of the uranium market in the coming years.

Cameco

Cameco is Canada’s largest uranium miner, with a market cap of $11B. The company’s best assets are in Canada, but they have assets in the US, Australia, as well as a joint venture in Kazakhstan with Kazatomprom. Cameco has a small dividend with a 0.3% yield, but they did hike it by 50% for 2022. I would recommend reading previous articles on Cameco, but I’m not as bullish on Cameco as I am on Kazatomprom. They will benefit from higher uranium prices, but several authors have written articles criticizing the company’s contract structure and facility shutdowns.

Sprott Uranium Trust

This part is straightforward, as the physical uranium trust simply tracks the price of uranium. Sprott has been buying up a significant chunk of the supply of uranium supply for months. Yellow Cake (OTCPK:YLLXF) is a smaller physical trust that has also been buying uranium on the open market. These might not have the same upside as the mining companies (especially smaller miners), but I think there will be material upside to the uranium price as more investors realize the magnitude of the supply and demand mismatch.

Conclusion

Like my article yesterday on Agnico Eagle (AEM) and Newmont (NEM), the URNM ETF is partially driven by a bet on higher commodity prices. It also is going to be driven by the continued flow of money into the sector and the related investments. URNM crossed $1B in AUM recently and I think institutional capital is going to start flowing in over the coming months.

We have already started to see it with Sprott Physical Uranium Trust, but it is going to become more obvious to investors in the coming months how mismatched supply and demand truly are. Uranium is the logical solution to the world’s energy problems, and I think the price of uranium will continue to march higher. If it does, investors buying URNM today could see significant upside.

[ad_2]

Source links Google News