[ad_1]

A little over a month and a half ago, I recommended that investors consider buying the United States 3x Short Oil Fund ETF (USOD). Since then, shares have increased by about 60% as the price of WTI crude has collapsed. Along the way, I suggested that investors take profit in the position due to resurgence of bullish fundamentals. In this article, I am going to revisit the thesis which led to the recommendation and discuss why I believe that even though the fundamentals are now bearish, it’s time to completely close out long positions in USOD due to a rapid oversell in price.

The Instrument

If you’re unfamiliar with USOD, it is an ETF that gives three times the inverse daily return of the price of crude oil. It follows a very similar methodology to USO in that it rolls exposure in similar fashion to maintain a triple levered exposure to futures. This said, the usual caveats about roll yield and leverage decay apply.

- Roll yield – When the market is in contango, USOD will benefit in that short positions higher up in the curve will decrease in value as time approaches expiry, and the opposite holds true for backwardation. The market is currently in contango, so those who are long USOD are reaping benefits from the roll.

- Leverage decay – When you hold a leveraged ETF, you really need to be aware that a long-term hold isn’t that good of an idea, regardless of direction. The reason for this is leverage decay can lead to severe underperformance depending on how volatility unfolds. If the market just chops sideways for lengthy periods of time, you have a higher likelihood of seeing decreases in the value of your holdings of leveraged instruments. To read more about that, I’d suggest this piece.

The Original Thesis

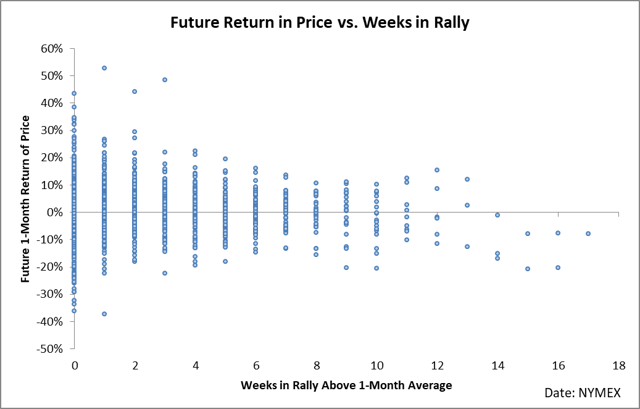

At the time of writing my initial long USOD recommendation in late April, I was bullish crude oil from a fundamental standpoint, but was concerned that the rubber-band was stretched too thin in terms of upside momentum. Specifically, I was concerned by the number of consecutive weeks in which price had closed above the one-month moving average. At the time of writing, WTI was in a 15-week trend of above-average prices, and the following chart of future returns versus consecutive runs strongly suggested that a correction was overdue.

From the simple numbers, the market was likely due for a correction of 10-20% over the next month. Since writing, we have seen a correction of over 20% in a fall which has increased the value of USOD by 60%.

The Fundamentals Changed

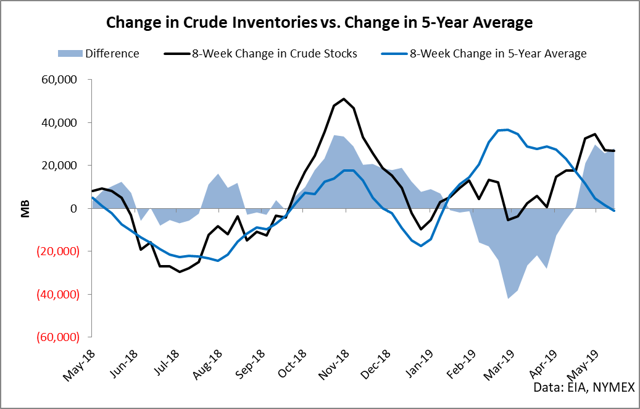

The fundamental landscape since my initial piece has changed in that the market is now structurally bearish due to a growing number of factors. An examination of the balance shows that inventories are growing against the five-year average, which indicates that the market is swinging further into oversupply. The following chart shows the eight-week change in inventories versus the eight-week change in the five-year average of inventories.

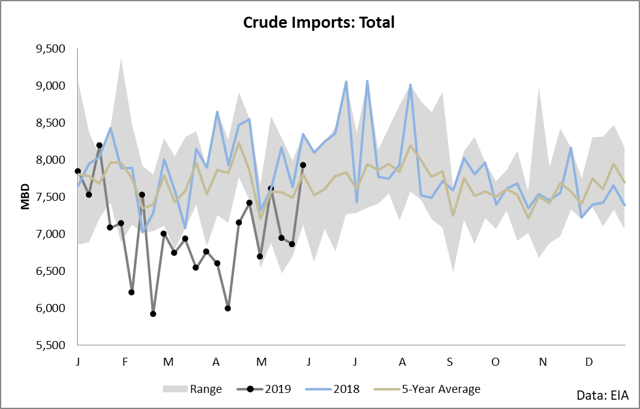

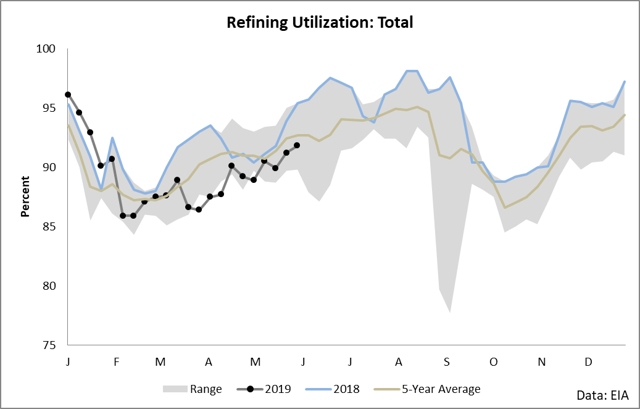

We are currently in one of the largest seasonally-adjusted builds of inventories seen since price began falling in late 2018. Inventories continue to surge in a time of the year in which they tend to fall. The culprit is a resumption of imports coupled with weak refining runs.

The basic problem with increasing imports is simply that this isn’t supposed to happen. Or at least, not when OPEC cuts are in force and imports from OPEC nations have collapsed.

OPEC is almost guaranteed to maintain cuts (or even increase the cuts) if it hopes to bring balance to the price of crude oil. I believe that we will see continued fundamental bearishness until something structurally changes in the supply equation as expressed by either substantial cuts in U.S. production or further OPEC supply cuts.

Technically Speaking

Despite the clear fundamental bearishness in the market, traders of USOD need to be aware that the rubber-band has now stretched a little too far to the downside in the price of crude oil.

Simply said, the market is strongly oversold in this downtrend with the price of crude oil seeing a handful of recent closes beneath the Bollinger Bands. Markets tend to oscillate between periods of with-trend and against-trend strength. In other words, they don’t travel in one direction without pausing and pulling back to some sort of average or support price before continuing once again in the direction of the trend. Crude oil is currently very oversold, and new positions initiated at these levels will likely not see exceptional returns or will see higher levels of volatility than necessary. Given the current depressed levels of price, I would suggest that investors in USOD wait until price pulls back towards support (which I see in the $56/bbl range) prior to initiating new shorts to capture the bearish thesis or completely close out positions until the next cycle in crude oil begins.

The Wildcard

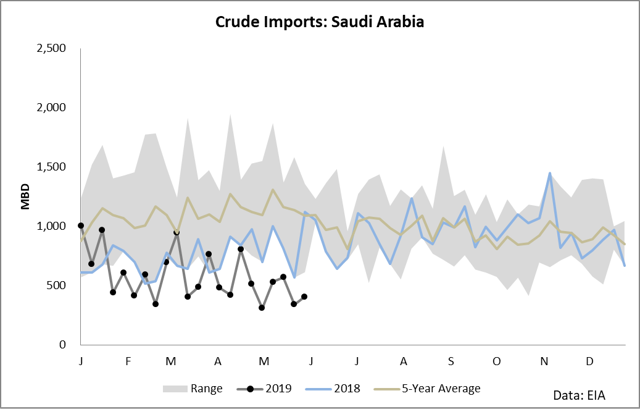

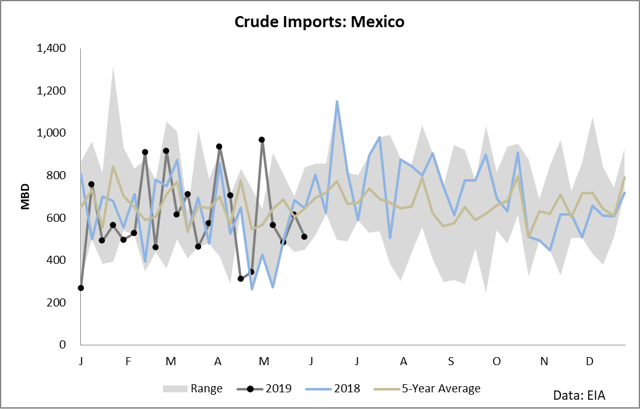

There is one wildcard to the fundamental thesis of bearishness which would derail the market pretty substantially, and that is Mexican tariffs. Trump is currently considering imposing a 5% tariff on the import of all Mexican goods in a bid to force Mexico’s hand in dealing with immigration issues. If Trump actually goes through with this, then a substantial portion of crude oil will immediately be uneconomic for Gulf Coast refineries and the price of crude will likely increase as the marginal barrel changes to a more expensive alternative. This displacement is not insignificant in that we import a substantial amount of crude from Mexico and securing this same equivalent supply would require some effort.

If Mexican tariffs happen, all bets are off, and we will likely see an immediate end to the bear market in crude oil. Until then, however, the market remains fundamentally bearish, and investors looking to capture the downside should consider USOD as a suitable instrument. However, the rubber-band is stretched too far to the downside in the price of crude, and I believe that shorts initiated at these levels will likely lose money for at least the next few weeks.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

[ad_2]

Source link Google News