[ad_1]

Over the last few weeks, there have been quite a few volatility shocks seen in the VIX as both trade fears and President Trump’s tweets have pushed market action. In this piece, I will take a step back and examine both seasonal and current trends in the VIX as well as a few specific instruments in the volatility ETP space. It is my belief that investors should look to short volatility in the coming weeks both on an outright basis as well as due to the methodologies of key volatility ETPs.

Tradable Instruments

When it comes to the volatility trading space, there are really only a few instruments available to equity investors. The reason for this lack of instrument availability largely has to do with the simple fact that there really are only so many ways of approaching the volatility markets and most of the methodologies from the popular volatility ETPs revolve around one key index: the S&P 500 VIX Short-Term Futures Index.

This index provided by S&P Global is an index which tracks an investment in VIX futures that is constantly rolled across the front two months of contracts. The purpose of this index is to give a weighted-average exposure such that the average contract maturity is roughly one month into the future. The way it does this is through a rolling scheme that heavily weights front-month exposure at the beginning of the month and then on a daily basis shifts exposure to the second-month future contract. This weighting scheme means that as a month progresses, roll yield becomes a progressively larger factor of index returns.

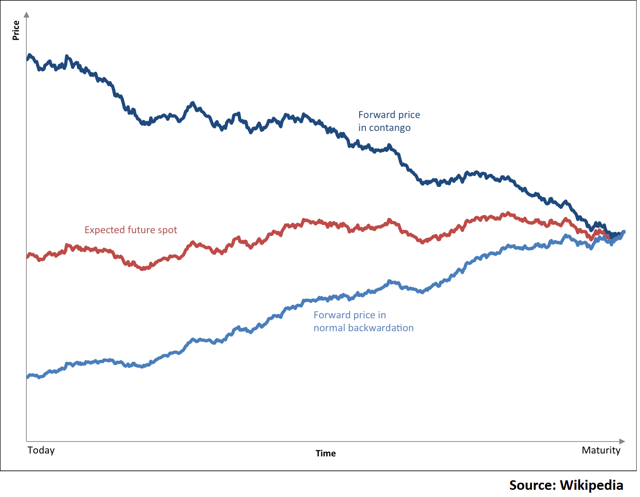

Put simply, roll yield is the gain or loss that arises from holding exposure across a futures curve. The underlying concept of roll yield can be seen in the following chart from Wikipedia:

When a market is in contango (front contract priced lower than back-month contracts), roll yield on a long position will be negative because as time progresses, the back-month futures contracts will tend to trade towards the front-month contract by falling. Conversely, when a market is in backwardation (front-month contract priced higher than back-month contracts), roll yield on a long position will be positive because the contracts held at lower prices will tend to trade up in value towards the front of the curve as time progresses.

This market tendency is the primary explainer of long-term returns for the S&P 500 VIX Short-Term Futures Index. Specifically, as you can see on the index fact sheet, the 10-year annualized return of strategy is an astounding negative 53%. I’d encourage the reader to carefully think this through. Ten years ago, the VIX ended September 2009 at 25.61. Today, the VIX is at 16.07. Over this time period, the VIX itself dropped by an annualized rate of 4.55%. The index which gives direct exposure to VIX futures contracts fell by an average of over 10 times this per year. Over long time frames, the returns of this methodology mean that ETP providers mimicking the index will see returns on capital simply evaporate. Let’s talk about which key ETPs are actually following this methodology.

The most popular volatility ETP is the iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX). You can read the prospectus here, but the title of the S&P index is in its name. It follows the short-term volatility index above and its one-year return is negative 30%. Note that this negative return comes despite the fact that the VIX itself has actually increased by over 22% over the last year. In other words, even if you successfully called the direction of volatility over the last year, buying VXX would have resulted in an astounding 52% underperformance of what actually happened in the index. Roll yield is a force to be reckoned with.

The second most popular volatility ETP is the ProShares VIX Short-Term Futures ETF (VIXY) and just like the name suggests, this ETF follows the same underlying volatility index. The key difference between VIXY and VXX is the fact that one is an ETN and the other is an ETF. With VIXY being an ETF, it actually holds VIX futures (rather than simply marking a value according to a methodology). Since it holds VIX futures and tracking error enters the picture, returns are different. Over the last year, VIXY has fallen by 12% while volatility has increased by 22%. Again, if you had held this instrument over the last year with the intention of capturing a directional increase in volatility, you would have underperformed the actual market you thought you were tracking by a whopping 34%, earning a loss while volatility rose.

Roll yield is an inescapable reality which arises from giving an equity-like exposure to futures markets. You have to constantly shift exposure into next-month futures contracts to keep the non-expiring nature of a stock in force. To do this, you’re forced to assume roll yield. As we will see in the next section, the reason why this has such a large effect on share returns has to do with the fact that volatility is trendless over long time frames.

The Nature of Volatility

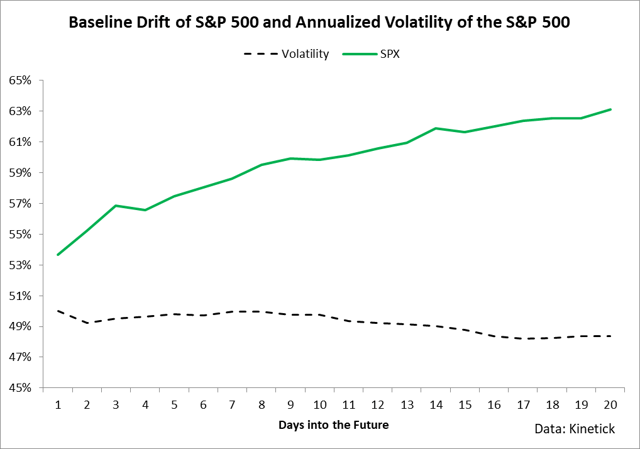

Put simply, volatility doesn’t really trend. What I mean by this is that over long periods of time, when volatility rises, it tends to fall in the future. As a case in point, here is the percentage of times that the S&P 500 increased over a certain time window compared the returns of volatility itself using market data since 1992.

As you can see, the S&P 500 has increased in about 63% of all 20-day periods over the last 27 years whereas volatility has generally gone nowhere. In other words, it simply doesn’t trend.

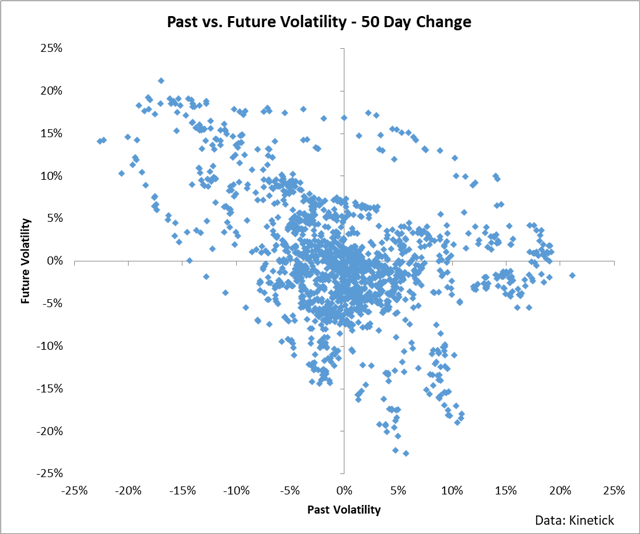

Another way of looking at this data is to compare past movements with volatility versus future movements in volatility.

Again, using all data from 1992 we see the concept of the trendless nature of volatility at work. When it increases over a time period, it tends to subsequently fall over the next time period.

What this means for volatility investors in any of the volatility ETPs is that even in a perfect world in which roll yield did not exist, long-run returns of holding volatility should be in the territory of 0%. When you add in the effects of roll yield, almost every single volatility product becomes a losing proposition because the VIX futures markets are generally in contango most of the time due to the assumption that volatility will be higher in later months.

The Current Market

We’ve talked about some of the most popular volatility ETPs and have shown both why and how returns are strongly negative across most time periods held. In this section, let’s examine the VIX itself to get a general trade recommendation for where the VIX is heading.

In the previous section, we talked about how volatility is trendless over long periods and therefore investments in volatility across long periods will generally have no return (before roll yield). While this truth is simple, it has profound implications for structuring trade ideas in the volatility markets.

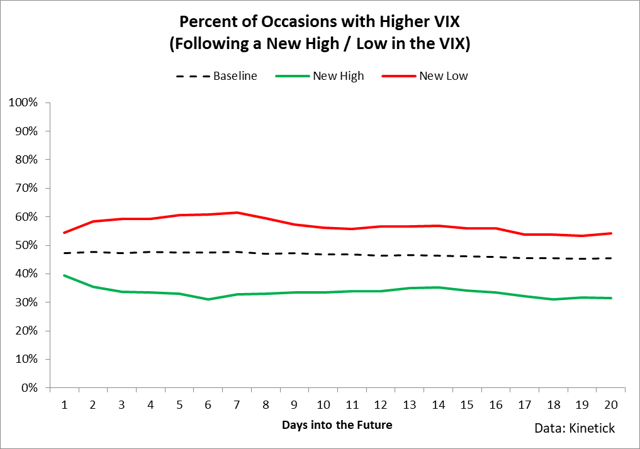

Since volatility increases tend to be followed by decreases in volatility, we can structure trades around statistical departures from the norm. For example, over the last week, the VIX hit the highest level in two weeks in a brief shock sell-off in the S&P 500. We can numerically quantify what happens following the VIX hitting fresh two-week highs or lows, the results of which are seen below.

At present, we are in a statistically significant time in market action in that there is a strong edge to fading rallies in the VIX. Specifically, since the VIX hit the highest level seen in 10 trading days, we can numerically say that since 1992, similar increases in the VIX have resulted in a lower level in the index over the next month around 65% of the time. This tangibly means that there is a strong possibility that the VIX will revert towards the mean over the next month. This will bring down returns in VIX ETPs at even greater rates than can simply be explained by roll yield.

Conclusion

We’ve taken a broad look at volatility both from a study of volatility itself as well as an examination of the most popular volatility ETPs. Volatility is highly mean reverting, which means that even if you could simply hold an instrument in perpetuity which returned the changes of the VIX, your long-run returns would likely be negligible. The most popular volatility ETPs offer exposure to an index which is heavily exposed to roll yield, which means that long-run returns are likely to be strongly negative. The VIX itself has hit fresh highs over the last week, which is strongly suggestive of lower outright levels of the VIX which will decrease values of most long volatility ETPs over the next month. It’s time to sell volatility, and it’s time to short volatility ETPs.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

[ad_2]

Source link Google News