[ad_1]

Andrii Dodonov

As you no doubt already know, the 2022 bear-market has been distinguished by a large shift in investor sentiment away from high-valued growth stocks and into more value oriented and dividend paying companies. That being the case, investors are looking for income from their investments – and that is exactly what the SPDR Portfolio S&P 500 High Dividend ETF (NYSEARCA:SPYD) is designed to provide. SPYD currently yields 4.6%, has an affordable 0.07% expense fee, and is selling at a deep valuation discount as compared to the S&P500. That being the case, today I’ll take a closer look at the SPYD ETF to see if it might be a suitable holding in your portfolio.

Investment Thesis

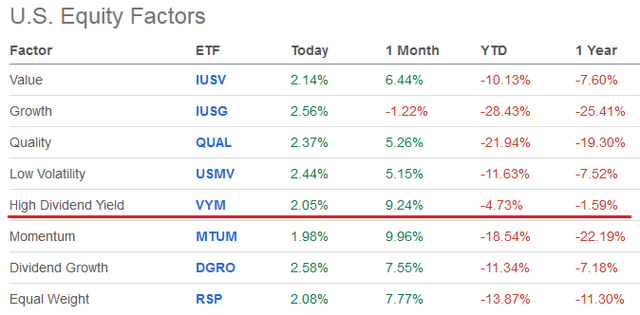

As the Federal Reserve has raised interest rates in order to combat inflation, the market has pivoted away from growth to value & income. Indeed, over the past year, the “High Dividend Yield” group has outperformed all other “equity factors” and beaten “Growth” by 23%+:

Seeking Alpha

So, today I’ll take a closer look at a diversified ETF approach to allocating capital to the high dividend yield space. Specifically, the SPYD ETF. You can find additional information on the State Street Global Advisors’ SPYD homepage.

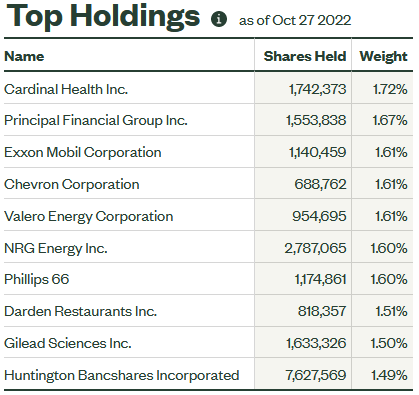

Top-10 Holdings

The top-10 holdings in the SPYD ETF are shown below and equate to what I consider to be a well-diversified portfolio across 80 companies:

State Street Global Advisors

The #1 holding with a 1.7% weight is Cardinal Health (CAH). Cardinal is an integrated healthcare services & products company with a global footprint. CAH provides customized solutions for hospitals, healthcare systems, pharmacies, clinical laboratories, and physician offices as well as for at-home patients. The stock is +61.7% over the past year, yields 2.6%, and trades with a forward multiple of only 14.7x.

Holdings #3-#7 are all energy companies – led by Exxon Mobil (XOM) with a 1.6% weight. XOM delivered Q3 earnings on Friday that saw net-income hit an all-time record of $19.66 billion – or $4.68/share. However, investors were less than enthused with a rather tepid 3.4% quarterly dividend increase to $0.91/share (or $3.64 on an annual basis). Exxon stock is up 72% over the past year, yet still yields 3.2%.

Chevron (CVX), the #4 holding, also reported earnings on Friday that were a big beat on both the top- and bottom-lines (by $0.71/share and $5.2 billion, respectively). Chevron generated a massive $12.3 billion of free-cash-flow during the quarter, or an estimated $6.34/share. The average sales price of Chevron’s natural gas production was a whopping $10.36/MMcf in Q3, up from $6.28 in last year’s third quarter. Chevron stock is up 59% over the past year, yields 3.2%, yet trades with a forward P/E of only 9.4x.

The #7 holding with a 1.6% weight is Phillips 66 (PSX). As I explained in my recent article on PSX, the company has a higher distillate yield as compared to its peers. (see PSX: A Coiled Spring). As a result, PSX has been killing it on diesel margin. The company is also the largest importer of Canadian oil sands production as a primary feedstock and is benefiting greatly from the current wide discount in WCS to WTI: the Dec 2022 futures closed indicate a $28/bbl WCS discount. PSX is up 35%+ this year and yields 3.7%. I expect PSX to report excellent Q3 earnings next week.

The top-10 holdings are rounded out by #10 Huntington Bancshares (HBAN). HBAN is headquartered in Columbus, OH and is the holding company for The Huntington National Bank – which provides commercial, consumer, and mortgage banking services in the U.S. HBAN operates via four segments: Consumer & Business Banking, Commercial Banking, Vehicle Finance, and Regional Banking & The Huntington Private Client Group. The stock yields 4.1% and trades with a forward P/E = 10.4x.

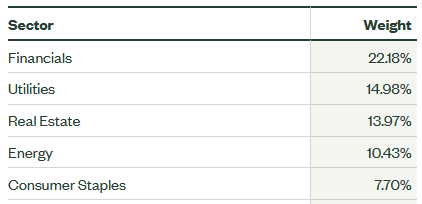

Generally speaking, the overall SPYD portfolio is significantly over-weight the following sectors:

State Street Global Advisors

For instance, the SPDR Financial Sector ETF (XLF) currently equates to 11.4% of the S&P500 while the SPDR Energy Sector ETF (XLE), for example, equates to only 5.3% of the S&P500. As can be seen in the above graphic, the SPYD ETF is ~2x over-weight those two sectors.

Valuation

As mentioned earlier, the SPYD ETF trades at a significant valuation discount to the S&P500:

| SPYD ETF | S&P500 | |

| P/E Ratio | 10.8x | 20.3x |

| Price-to-Book | 1.6x | 3.9x |

That being the case, investors should definitely consider that the SPYD not only provides strong income, but it is also very conservatively positioned in terms of valuation risk.

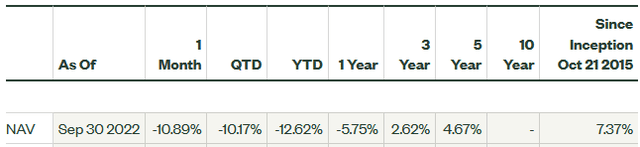

Performance

The SPYD ETF has an noticeably tepid performance track-record: the average NAV 5-year annual return is only 4.7%:

State Street

However, note that during most of the past 5-years encapsulated a low interest rate market that greatly favored growth over value and/or income. That is, SPYD’s returns as shown above are likely not indicative of “full-cycle” market returns or what to expect over the near- and mid-term during which interest rates will quite likely be considerably higher as compared to the last 5-years.

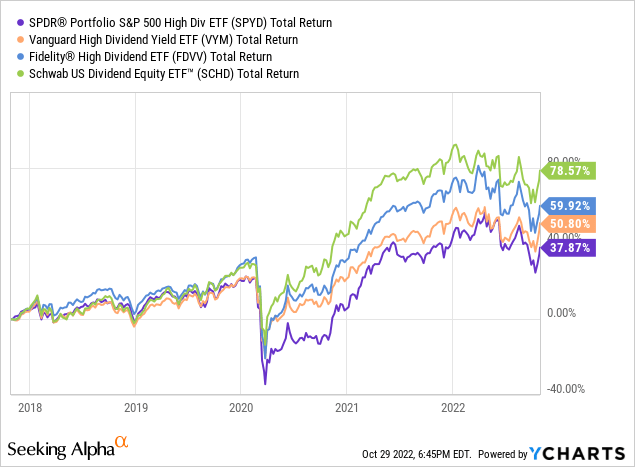

The following graphic shows the 5-year total returns of the SPYD ETF versus several of its peers, including: the Vanguard High Dividend Yield ETF (VYM), the Fidelity High Dividend ETF (FDVV), and the Schwab U.S. Dividend Equity ETF (SCHD):

As can be seen, the SPYD ETF is the worst performing fund of the chosen group and has severely lagged my favorite dividend fund, SCHD, by a whopping 40%+. Note SCHD also has a lower expense ratio (0.06% versus SPYD’s 0.07%). While SCHD’s current 30-day yield of 3.49% is significantly lower than SPYD’s 4.59%, it is clear that from a total returns perspective, SCHD is the superior investment.

Risks

As just shown, the biggest risk of investing in the SPYD ETF might be a lack of total returns. That said, and while I do favor the SCHD ETF, note that it trades at a significantly higher valuation level as compared to SPYD: SCHD has a P/E ratio of 13.4x and a price-to-book of 3.2x (double the price-to-book of SPYD). From that perspective, if we continue to struggle in a weak overall market (excepting the big rally last week …), I would think the SPYD ETF has significantly less downside risk as compared to SCHD.

The other risk is that SPYD might represent a conglomeration of “value trap” type stocks – stocks that pay out a lot of cash-flow as dividends instead of investing for the future.

Summary & Conclusions

A well diversified portfolio should certainly have some investments for income. For me personally, I get the majority of my dividend income from individual energy stocks (indeed, I own three of the energy companies in the SPYD’s top-10 holdings), the SCHD ETF, and through shares of Broadcom (AVGO) – which currently yields 3.5%. And while the opportunity for dividends from a diversified ETF is an attractive option, the SPYD ETF is not the one for me, and likely isn’t for you either. I say that because while the SPYD dividend yield is attractive, the fund appears to be stretching to get that yield by investing in companies that are relatively dormant in terms of capital appreciation. That being the case, my advice is that investors should SELL SPYD and move the proceeds into the SCHD ETF instead. You’ll lose 1.1% in yield, but your total returns should be significantly higher for years to come.

[ad_2]

Source links Google News