According to Invesco, the Invesco S&P SmallCap Energy ETF (NASDAQ:PSCE) is an exchange-traded fund, the “Fund,” is:

Based on the S&P SmallCap 600® Capped Energy Index (the “Index”), the Fund will normally invest at least 90% of its total assets in the securities of small-capitalization US energy companies that comprise the Underlying Index. The Index is designed to measure the overall performance of common stocks of US energy companies. These companies are principally engaged in the business of producing, distributing or servicing energy related products, including oil and gas exploration and production, refining, oil services and pipelines.”

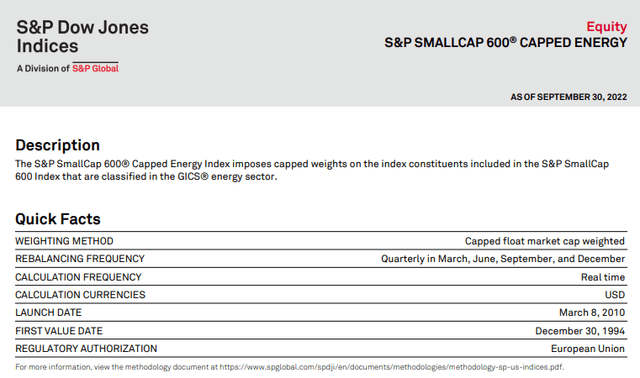

The Index upon which PSCE is based is outlined below by S&P.

S&P Dow Jones Indices

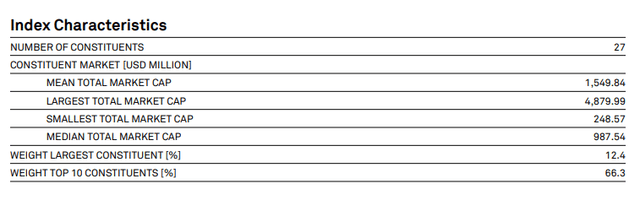

S&P Dow Jones Indices

S&P Dow Jones Indices

The detailed Methodology is explained within this paper for anyone who is interested in “getting into the weeds.”

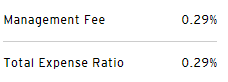

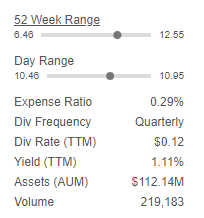

Expense Ratio and Assets Under Management (“AUM”)

The Expense Ratio equals the Management Fee of 0.29%. And the Fund has about $112 million AUM.

Invesco

Seeking Alpha

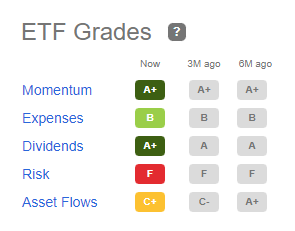

Seeking Alpha grades Expenses as a “B” for ETFs.

Seeking Alpha

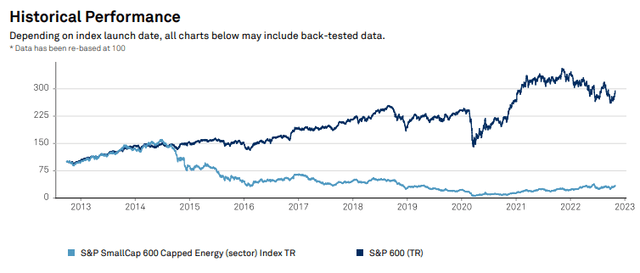

The Index was launched in March 2010. Over the past 10 years it has grossly underperformed the broader equity market.

S&P Dow Jones Indices

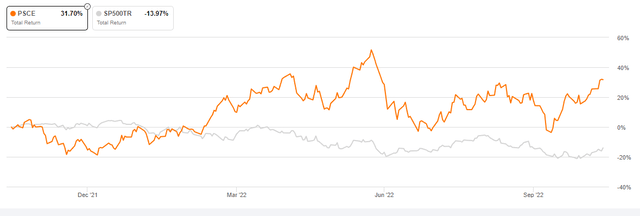

However, over the past year, the Fund has returned 31.7%, as compared to a loss of 13.97% in the SP500TR due to the overall strength of the energy market.

Seeking Alpha

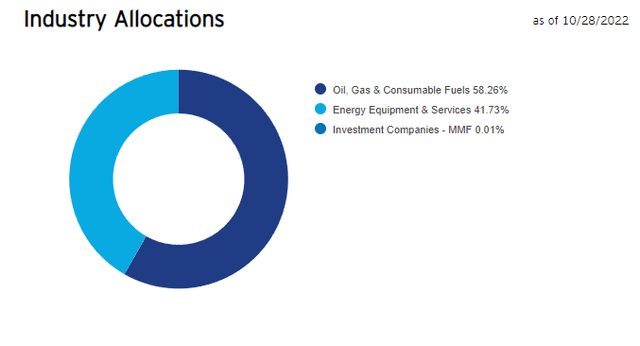

The Fund is mostly invested in companies that produce fuels, but there is a significant allocation (42%) in the Energy Equipment and Services subsector.

Invesco

Invesco

Invesco

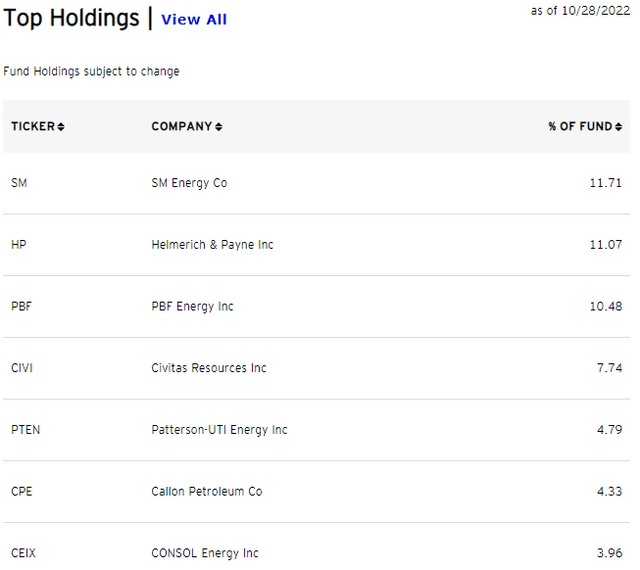

Analysis of Top Holdings

In my analysis of the annual returns, PSCE had a total return of 31.70 %. The three top performers were PBF Energy Inc. (PBF) at 199.80%, CONSOL Energy Inc. (CEIX) at 131.88% and Patterson-UTI Energy, Inc. (PTEN) at 92.32 %. The other holdings in the top ten had lower returns and two had losses. The top ten accounted for about 65 % of the Fund’s total allocations and provided a weighted average return of 47 %. And I therefore estimate that the Other Holdings had a 35 % allocation which produced a weighted-average loss of about 42 %.

PSCE

Invesco S&P SmallCap Energy ETF

31.70%

Top Holdings

Allocation

RoR

Wt. RoR

SM

SM Energy

11.71%

40.08%

4.69%

HP

Helmerich & Payne Inc

11.07%

57.96%

6.42%

PBF

PBF Energy Inc

10.48%

199.80%

20.94%

CIVI

Civitas Resources Inc

7.74%

39.12%

3.03%

PTEN

Patterson-UTI Energy INC

4.79%

92.32%

4.42%

CEIX

CONSOL Energy Inc

4.33%

131.88%

5.71%

CPE

Callon Petroleum Co

3.96%

-17.03%

-0.67%

NBR

Nabors Industries Ltd

3.65%

19.79%

0.72%

INT

World Fuel Services Corp

3.63%

-19.54%

-0.71%

TALO

Talos Energy Inc

3.24%

66.02%

2.14%

Subtotal

64.6%

46.69%

Other Holdings

Subtotal

35.4%

-42.33%

-14.98%

Total

31.70%

Source: BRS.

PBF Energy Inc. (PBF)

According to its Annual Report:

We are one of the largest independent petroleum refiners and suppliers of unbranded transportation fuels, heating oil, petrochemical feedstocks, lubricants and other petroleum products in the United States. We sell our products throughout the Northeast, Midwest, Gulf Coast and West Coast of the United States, as well as in other regions of the United States, Canada and Mexico and are able to ship products to other international destinations. As of December 31, 2021, we own and operate six domestic oil refineries and related assets. Based on the current configuration (as disclosed in the “Refining” section below) our refineries have a combined processing capacity, known as throughput, of approximately 1,000,000 bpd, and a weighted-average Nelson Complexity Index of 13.2 based on current operating conditions. The complexity and throughput capacity of our refineries are subject to change dependent upon configuration changes we make to respond to market conditions, as well as a result of investments made to improve our facilities and maintain compliance with environmental and governmental regulations. We operate in two reportable business segments: Refining and Logistics.”

Last Thursday, PBF “posted third quarter results that comfortably beat Wall Street estimates as the petroleum refiner continued to benefit from strong customer demand for its products and higher gross margins.”

U.S. refining margins may have peaked (see my article, CVR Energy: Refinery Margins May Be Peaking, for discussion); however, quarterly earnings in the sector are likely to remain elevated for numerous quarters to come.

CONSOL Energy Inc (CEIX)

According to its Annual Report:

We are a leading, low-cost producer of high-quality bituminous coal, focused on the extraction and preparation of coal in the Appalachian Basin due to our ability to efficiently produce and deliver large volumes of high-quality coal at competitive prices, the strategic location of our mines and the industry experience of our management team.

Our most significant assets are the PAMC and CONSOL Marine Terminal. Coal from the PAMC is valued because of its high energy content (as measured in Btu per pound), relatively low levels of sulfur and other impurities, and strong thermoplastic properties that enable it to be used in metallurgical, industrial and power generation applications. We take advantage of these desirable quality characteristics and our extensive logistical network, which is directly served by both the Norfolk Southern and CSX railroads, to aggressively market our product to a broad base of strategically selected, top-performing power plant customers in the eastern United States. We also capitalize on the operational synergies afforded by the CONSOL Marine Terminal to export our coal to industrial, power generation and metallurgical end-users globally.”

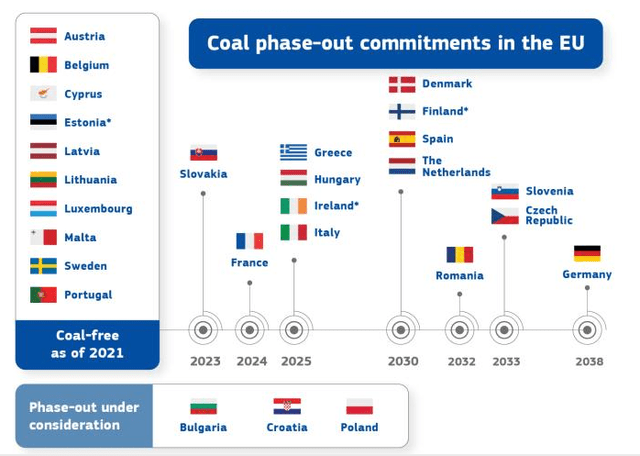

The energy crisis in Europe, caused by the Russian-Ukrainian conflict, has resulted in the EU’s mission to shift away from Russian energy oil and gas. Hence, the rebound in the demand for American-supplied coal.

“Coal accounts for about 20% of total electricity production in the EU,” according to the European Commission. Of course, the EU is transitioning away from fossil fuels, but the current crisis needs to be met by non-Russian energy sources.

The coal phase-out has been planned as outlined below. The increase in demand for American coal is likely to be short-term but could endure for another year or two or possibly longer, as the EU replaces Russian natural gas supplies. I view it as a risky investment but may do well short-term.

European Commission

Patterson-UTI Energy Inc (PTEN)

According to its Annual Report:

We are a Houston, Texas-based oilfield services company that primarily owns and operates one of the largest fleets of land-based drilling rigs in the United States and a large fleet of pressure pumping equipment.

Our contract drilling business operates in the continental United States and internationally in Colombia and, from time to time, we pursue contract drilling opportunities in other select markets. As of December 31, 2021, we had a drilling fleet that consisted of 184 marketed land-based drilling rigs in the United States and eight in Colombia. A drilling rig includes the structure, power source and machinery necessary to cause a drill bit to penetrate the earth to a depth desired by the customer. We also have a substantial inventory of drill pipe and drilling rig components that support our contract drilling operations.

We provide pressure pumping services to oil and natural gas operators primarily in Texas and the Appalachian region. Substantially all of the revenue in the pressure pumping segment is from well stimulation services (such as hydraulic fracturing) for completion of new wells and remedial work on existing wells. Well stimulation involves processes inside a well designed to enhance the flow of oil, natural gas, or other desired substances from the well. As of December 31, 2021, we had approximately 1.1 million fracturing horsepower to provide these services.

We also provide cementing services through the pressure pumping segment. Cementing is the process of inserting material between the wall of the well bore and the casing to support and stabilize the casing. Our pressure pumping operations are supported by a fleet of other equipment, including blenders, tractors, manifold trailers and numerous trailers for transportation of materials to and from the worksite as well as bins for storage of materials at the worksite. We also provide a comprehensive suite of directional drilling services in most major producing onshore oil and gas basins in the United States. Our directional drilling services include directional drilling, measurement-while-drilling and supply and rental of downhole performance motors. We also provide services that improve the statistical accuracy of directional and horizontal wellbores.”

Last Thursday, PTEN reported:

better-than-expected Q3 results and raised its guidance for 2022 adj. earnings. The company now expects 2022 consolidated adj. EBITDA of over $650M vs. prior outlook of more than $600M. Q4 rig count in the U.S. is projected to average 132 rigs, with an average of 81 rigs operating under term contracts. Patterson-UTI (PTEN) also raised its 2022 capex outlook to ~$425M to factor in ramping up of customer-funded rig upgrades for delivery in 2023 and acquisition of additional pumps with tier 4 engines vs. its earlier forecast of $390M.”

The outlook for relatively high U.S. crude oil prices, though probably lower than they were during 2Q22, is supportive of domestic drilling programs generally, and PTEN, specifically.

Conclusions

The small cap energy sector does include some names with strong earnings prospects, given the dramatic shift in the world oil order following Russia’s invasion of Ukraine. But not all companies in the sector have the same prospects, as reflected by the large variance in returns among the names. The three top performers have good future prospects, but this article does not attempt to evaluate the entire sector.

For that reason, I believe it would be more prudent to be more selective than the Index, upon which the Fund is based. Therefore, I would not buy the Fund itself. I’d rather be more selective.