")

[ad_1]

Tirachard/iStock via Getty Images

Main Thesis / Background

The purpose of this article is to evaluate the ProShares Online Retail ETF (NYSEARCA:ONLN) as an investment at the current market price. This fund takes an approach to own retailers that principally sell online or through other non-store channels, rather than traditional brick and mortar retailers.

This is an ETF I have generally cautioned readers against buying for some time, including when I covered it at the end of last year. In hindsight, this outlook is vindicated to a degree. While avoiding it was absolutely the right move, I should have been more bearish with that outlook. The reason being that ONLN has hit bear market territory since that review was published:

Fund Performance (Seeking Alpha)

With this drop, ONLN has officially entered “bear market” territory if we use the publication date of my last article as the base. This is worrisome, of course, but it also presents opportunity. At this juncture, I feel the fund and the underlying holdings within it probably have more upside than downside going forward. Simply, this move seems a bit unjustified when I consider some of the positives, especially with regards the top holdings. As a result, I feel an upgrade to “buy” for ONLN is warranted, and I will explain why in detail below.

Inflation and Interest Rates Remain Headwinds

To begin, I want to highlight some of the reasons behind the decline in ONLN over the past few quarters. As I mentioned above, I think the steep losses the fund has seen offers an opportunity for buying now. That said, it is important to understand the why behind these losses, so readers can decide for themselves in their agree with my thesis or if they believe there is more pain to come.

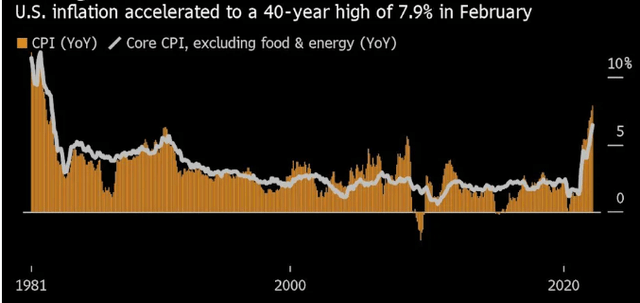

A key reason behind the general weakness in retail, whether for e-commerce focused plays like those in ONLN or within the retail sector more broadly, is inflation. This is a sore spot for most of the market – save for commodity, material, and energy plays which have thrived in this environment. While many market pundits continued the line of “transitory” for quite a long time (despite little to no evidence supporting that view), the actual inflation story has done nothing but get worse over time. While investors, households, and economists were hoping 2022 might bring some relief, the actual result has been accelerating inflation, as seen below:

Inflation (Yahoo Finance)

This broad inflation metric helps explain the weakness in retail and consumer-oriented plays of late. Inflation is eating away at take-home pay and savings, whether it is at the gas pump, restaurants and grocery stores, or discretionary apparel and department stores. Rising prices tend to be followed by declining or stagnating retail sales, and that has been the case in the last few months.

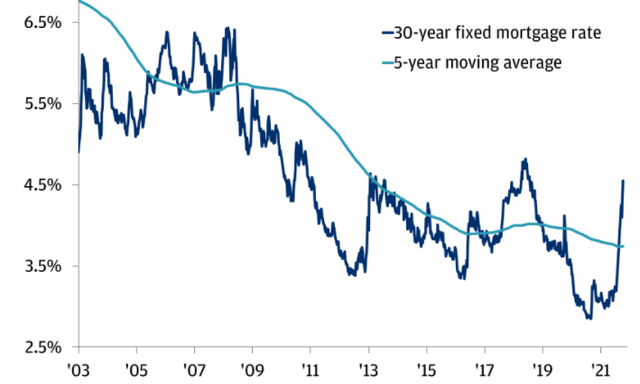

Aside from macro-metrics like this, American households are feeling the pinch closer to home as well. It is not just at the store or the gas station where Americans are having to shell out more cash. As inflation has risen, so have yields and interest rates. This has trickled down to the mortgage market as well. In fact, mortgage rates are rising at a faster pace than central banks have acted, with the 30-year mortgage in the U.S. nearing 5%:

Mortgage Rates (JPMorgan Private Bank)

The point here is that American, and global, consumers are in a tough spot. Wages and employment are rising, yes, but inflation and interest rates are rising a bit faster. This is pressuring consumer sentiment and forward spending plans, which has been a challenge for funds like ONLN, and many others.

Retail Sales Have Been Inconsistent

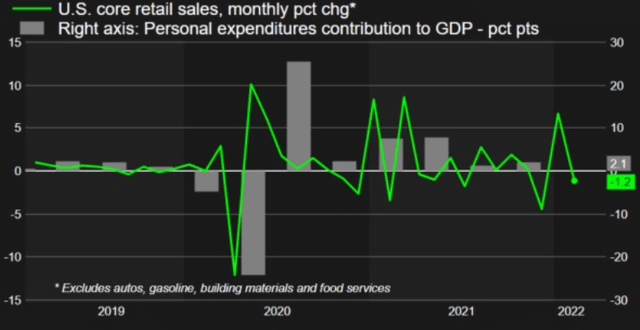

Another relative pain point has been the inconsistent retail picture over the past year. Simply, retail sales growth has not been able to maintain a trend in either direction. This is not too surprising, given strained supply-chains, inflation metrics, and geo-political risks in Europe and Asia. While the trend has not been too bad, isn’t hasn’t been too good either, which has kept investors from bidding up retail shares in the short-term:

Retail Sales (Reuters)

I look at this graphic a few ways. One, it suggests the U.S. consumer has actually been fairly resilient given how difficult the macro-environment is. This supports holding on to exposure to this key demographic. Further, while the back and forth is a bit unnerving for investors, the fact that the trend is not in a consistent downward trajectory suggests to me that perhaps the sell-off in retail funds like ONLN is a bit unjustified. This is at the crux of my “buy” thesis at the moment. Is the retail picture challenging? Of course. Are American consumers nervous and worried about the future? Of course. But are retail sales really that poor to suggest a 20% decline in ONLN since the start of the year is a valid reaction? I think not.

Others may disagree here, but my takeaway is that ONLN’s performance has not been accurately reflected by conditions on the ground. This is why I see a buy case emerging, even though challenges definitely remain in place.

Buying The Dip In The Top Holdings

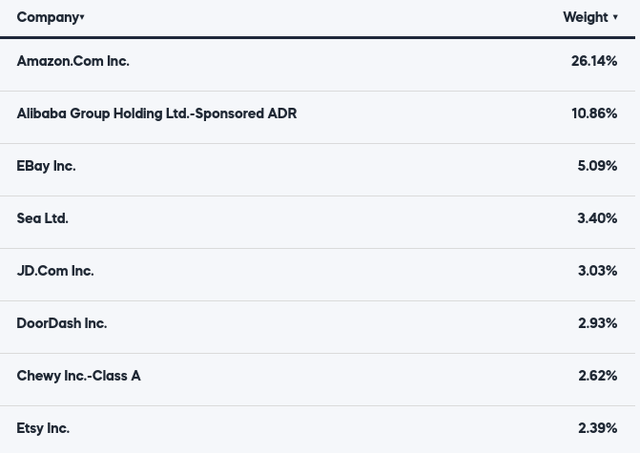

I now want to shift the discussion to some of the underlying holdings in ONLN. While this is a diversified ETF that holds 39 companies, readers should realize when they buy this fund they are buying quite a bit of exposure to two companies. This is a bit more top heavy than I personally like in an ETF, but it has been the case since I began following it years ago. In the case of ONLN, this means investors are getting more than 37% exposure to Amazon (AMZN) and Alibaba Group (BABA):

ONLN’s Top Holdings (ProShares)

Now, whether or not this is a “good” thing depends on each individual investors. What their outlook is for these companies, their risk tolerance, and whether or not they view buying a concentrated fund as a positive thing.

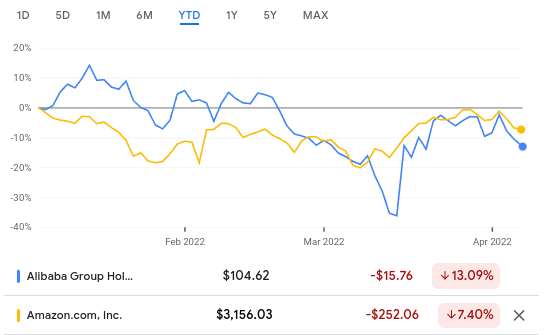

For me, I don’t generally view such concentration favorably. Yet, I think at this juncture the buy case is too glaring to let this deter me. Companies like AMZN and BABA have been growing for a long time, and the weakness in 2022 has gotten me interested in both of them:

YTD Performance (Google Finance)

Looking at BABA first, readers should note this is reflective of a broader trend of selling Asian, and specifically Tech-oriented Asian, stocks. While BABA’s decline is not too comforting, if we look at the broader Hang Seng Tech index, we see it is near bear market levels for the year. This accompanies to the wider Hand Seng Index, whose drop has been less than half on a year-to-date basis:

YTD Performance (Yahoo Finance)

To be fair, readers could surely look at this graphic as a reason to avoid Asian tech, BABA, and ONLN by extension. But I am taking the contrarian view here. Bear markets level generally get me interested, especially when the broader trend is still in-tact. Online buying / e-commerce is one such trend that is not going away, and that helps shore up my confidence for both AMZN and BABA, and ONLN as a whole.

Further, there are a couple other reasons I think BABA in particular. One, management has shown a commitment to return capital to shareholders via share buybacks. In fact, their buyback program has been accelerating over time, coinciding with the stock’s drop in price. This tells me management is fairly confident the price is undervalued:

BABA Share Buybacks (Bloomberg)

Now, a casual look at this graphic would suggest buying because BABA has been conducting buybacks has not be a winning strategy. And I would agree. Despite the initial announcement, as well as continuous boosts to the buyback plan, the stock has continued to fall. But that lies at the heart of the inherent disconnect between the value management sees, and the market sees.

In truth, a lot of BABA’s decline probably stems from macro-factors that have affected Chinese stocks, especially Tech stocks, as a whole. So while this is relevant to BABA, it extends beyond the company. That is why I see value here, because the market may be unduly punishing this particular company, especially with such an aggressive share buyback program underway.

For those who may not follow the Chinese market as closely, a recap of why there has been such a broad decline stems from a number of factors. One, Chinese regulators have been more aggressive in doling out fines, arrests, and tighter rules for the future. Two, the U.S. government has a renewed interest in forcing Chinese companies to delist in the U.S. if they don’t meet accounting transparency laws. This would be a major blow, as it would probably soften demand here, and elsewhere around the world, for these stocks. Three, a surge in Covid-cases has prompted lockdowns across China, which has clouded the short-term outlook for large-cap firms. This is especially true of consumer-oriented firms (i.e. BABA) as consumers have locked down again.

All of these are serious concerns, but I believe the regulatory pressures and Covid-related pressures will smooth out in time. The reasons for the sell-off in these shares are valid, but long-term the story looks much better. This makes buying during a time of pessimism the right move in my view.

How Can One Be Optimistic?

The prior paragraph looked mostly at BABA, but I think there is value in buying the weakness in AMZN as well. Beyond that, I see the merit in retail, especially online retail, at these levels.

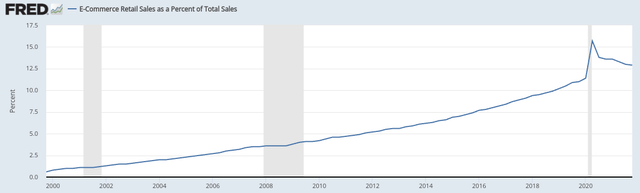

Broadly speaking, one trend that continues to lend merit to buying in to e-commerce retail plays (of which AMZN is a primary player) is the rising level of total retail sales being conducted online. In fairness, this percentage has come down over the past two years, but that is because it saw such a massive spike during the worst of the pandemic. If we look at pre-Covid numbers, we see the current percentage of e-commerce sales (as a percent of total sales) remains well above pre-crisis levels:

E-Commerce Retail Sales as a Percent of Total Sales (St. Louis Fed)

This is an encouraging trend if we look at the past decade and not just focus on the slip from the last two years. For me, I continue to see a future where more and more commerce is conducted online. This is simply a rising trend that is not going to reverse for the foreseeable future. This makes plays like AMZN, BABA, and ONLN the right moves when you can buy them during times of market distress.

Another point I would bring up is that while rising yields and interest rates are punishing tech stocks and growth names in particular, I believe this fear is a bit over-hyped. I see a scenario where the Fed moves its benchmark rate into the 2.5% – 3% range. This is very manageable for large-cap corporations that are time tested, whether it is AMZN or any the average company in the S&P 500.

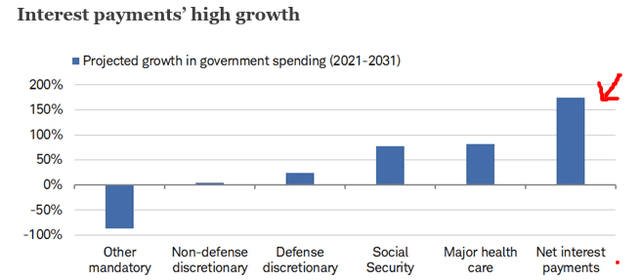

I bring this up because while central banks are getting more hawkish and investors are starting to price in more rate hikes, I want to moderate the outlook on this front. While the Fed may have an appetite for a more aggressive rate hiking cycle, the realities of government over-spending are going to hamstring them a bit. If we bake in a modest increase in interest rates, we see that over time the U.S. government is going to have to outlay more and more of its revenues on servicing debt payments:

Projected Gov’t Spending (Charles Schwab)

This is a macro-fundamental that is relevant for the market as a whole. But I see it especially relevant for growth-oriented funds/sectors/stocks because those are the ones being pressured the most by the hawkish rate changes. My view is that interest rates will go up a bit more, by 1.5-2.0%, and then the Fed is going to have to put on the brakes. The government simply can finance its annual borrowing levels if rates go up much more than that.

Bottom-line

ONLN has had a rough 2022, there is no denying that. However, I see enough positives at the moment to feel comfortable predicting brighter days are ahead. Importantly, the concentration of the fund and the tech-heavy nature of many of the holdings make this a riskier play. But with risks can come rewards, and I see ONLN posting gains in the months ahead. As a result, I am putting a “buy” rating on ONLN, and suggest readers give this idea some consideration at this time.

[ad_2]

Source links Google News