[ad_1]

J-Elgaard/E+ via Getty Images

This monthly article series shows a dashboard with aggregate industry metrics in healthcare. Companies used to calculate these metrics are the largest holdings of the Health Care Select Sector SPDR ETF (XLV). Therefore, this is also a review of XLV.

Shortcut

The next two paragraphs in italic describe the dashboard methodology. They are necessary for new readers to understand the metrics. If you are used to this series or if you are short of time, you can skip them and go to the charts.

Base Metrics

I calculate the median value of five fundamental ratios for each industry: Earnings Yield (“EY”), Sales Yield (“SY”), Free Cash Flow Yield (“FY”), Return on Equity (“ROE”), Gross Margin (“GM”). The reference universe includes large companies in the U.S. stock market. The five base metrics are calculated on trailing 12 months. For all of them, higher is better. EY, SY and FY are medians of the inverse of Price/Earnings, Price/Sales and Price/Free Cash Flow. They are better for statistical studies than price-to-something ratios, which are unusable or non-available when the “something” is close to zero or negative (for example, companies with negative earnings). I also look at two momentum metrics for each group: the median monthly return (RetM) and the median annual return (RetY).

I prefer medians to averages because a median splits a set in a good half and a bad half. A capital-weighted average is skewed by extreme values and the largest companies. My metrics are designed for stock-picking rather than index investing.

Value and Quality Scores

I calculate historical baselines for all metrics. They are noted respectively EYh, SYh, FYh, ROEh, GMh, and they are calculated as the averages on a look-back period of 11 years. For example, the value of EYh for healthcare providers in the table below is the 11-year average of the median Earnings Yield in this industry.

The Value Score (“VS”) is defined as the average difference in % between the three valuation ratios (EY, SY, FY) and their baselines (EYh, SYh, FYh). The same way, the Quality Score (“QS”) is the average difference between the two quality ratios (ROE, GM) and their baselines (ROEh, GMh).

The scores are in percentage points. VS may be interpreted as the percentage of undervaluation or overvaluation relative to the baseline (positive is good, negative is bad). This interpretation must be taken with caution: the baseline is an arbitrary reference, not a supposed fair value. The formula assumes that the three valuation metrics are of equal importance.

Current Data

The next table shows the metrics and scores as of last week’s closing. Columns stand for all the data named and defined above.

|

VS |

QS |

EY |

SY |

FY |

ROE |

GM |

EYh |

SYh |

FYh |

ROEh |

GMh |

RetM |

RetY |

|

|

HC Equipment |

-27.59 |

2.89 |

0.0283 |

0.1940 |

0.0223 |

13.86 |

67.86 |

0.0340 |

0.2844 |

0.0339 |

14.16 |

62.90 |

-11.48% |

-8.78% |

|

HC Providers |

0.56 |

0.44 |

0.0537 |

1.3632 |

0.0669 |

18.39 |

20.82 |

0.0528 |

1.4642 |

0.0626 |

15.91 |

24.40 |

-7.25% |

-1.32% |

|

Pharma/Biotech |

13.83 |

50.42 |

0.0454 |

0.2261 |

0.0461 |

41.02 |

79.97 |

0.0378 |

0.2565 |

0.0346 |

20.36 |

80.49 |

-8.06% |

-12.45% |

|

Life Science Tools |

-26.65 |

3.64 |

0.0271 |

0.1468 |

0.0255 |

15.74 |

58.99 |

0.0301 |

0.2961 |

0.0317 |

15.62 |

55.38 |

-9.13% |

-10.36% |

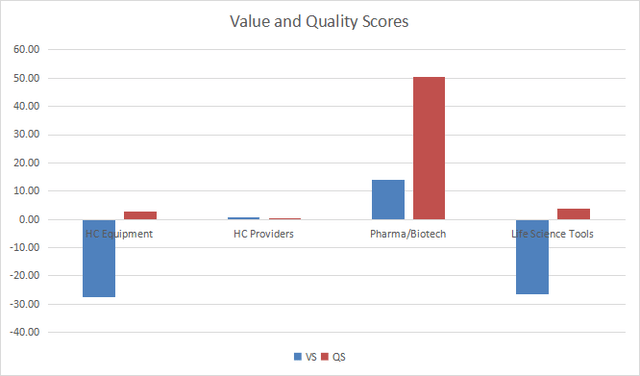

Value and Quality Chart

The next chart plots the Value and Quality Scores by industry (higher is better).

Value and quality in healthcare (Chart: author; data: Portfolio123)

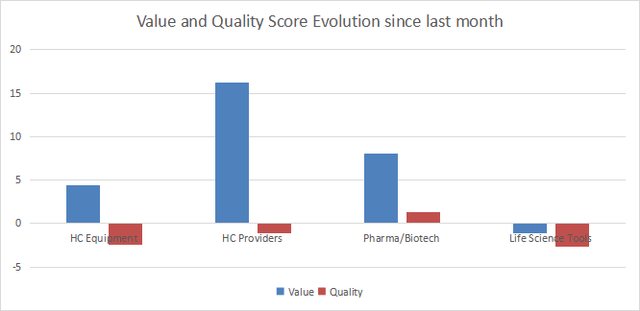

Evolution Since Last Month

The value score has significantly improved in healthcare providers and to a lesser extent in pharmaceuticals/ biotechnology and healthcare equipment.

Value and quality variations (Chart: author; data: Portfolio123)

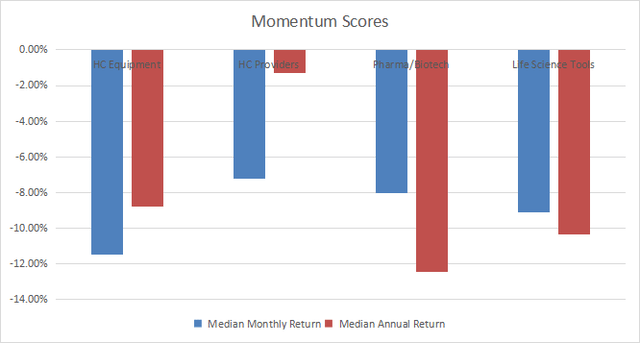

Momentum

The next chart plots median returns by subsector.

Momentum in healthcare (Chart: author; data: Portfolio123)

Interpretation

Pharma/biotech has been the most attractive subsector for months regarding my metrics. Now it is undervalued by about 14% relative to 11-year averages and quality metrics are far above the historical baseline. Healthcare providers are very close to their baseline in both value and quality. Life science tools and healthcare equipment are overvalued by more than 25%. Their quality scores are close to the baseline.

IXJ: An Alternative to XLV

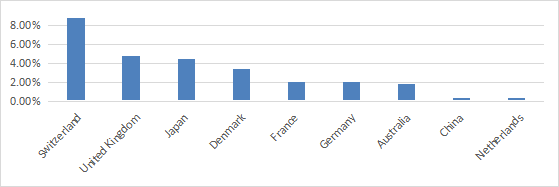

The iShares Global Healthcare ETF (NYSEARCA:IXJ) has been tracking the S&P Global 1200 Health Care Index since 11/13/2001. It holds 117 stocks (plus cash and equivalent in various currencies), has an expense ratio of 0.43% and a distribution yield of 1.21%. The underlying index selects international healthcare companies weighted based on float-adjusted market capitalization. About 71% of asset value is in U.S. companies. The next chart shows the weights of other countries.

Countries ex-US (chart: author, data: Fidelity)

The next table lists the top 10 holdings with basic fundamental ratios. Their aggregate weight is 40.7% of asset value. Tickers of non-US companies below are those listed in the U.S., but the fund holds shares in primary exchanges.

|

Ticker |

Name |

Weight % |

EPS %growth TTM |

P/E TTM |

P/E fwd |

Yield% |

Location |

|

JNJ |

Johnson & Johnson |

6.76 |

31.16 |

24.08 |

17.43 |

2.53 |

NYSE |

|

UNH |

UnitedHealth Group Inc |

6.66 |

3.86 |

26.95 |

22.71 |

1.18 |

NYSE |

|

PFE |

Pfizer Inc |

4.14 |

121.74 |

11.78 |

7.62 |

3.12 |

NYSE |

|

ABBV |

AbbVie Inc |

3.93 |

146.28 |

22.19 |

11.00 |

3.64 |

NYSE |

|

LLY |

Eli Lilly and Co |

3.44 |

0.93 |

44.70 |

35.83 |

1.30 |

NYSE |

|

MRK |

Merck & Co Inc |

3.37 |

102.06 |

16.64 |

12.63 |

2.97 |

NYSE |

|

OTCQX:RHHBY |

Roche Holding AG |

3.28 |

-0.13 |

18.31 |

15.27 |

3.06 |

SIX |

|

TMO |

Thermo Fisher Scientific Inc |

3.14 |

-3.52 |

28.91 |

24.32 |

0.22 |

NYSE |

|

NVS |

Novartis AG |

3.08 |

208.83 |

8.13 |

14.32 |

3.78 |

SIX |

|

AZN |

Astrazeneca PLC |

2.91 |

-121.77 |

N/A |

19.57 |

2.19 |

London |

Ratios: Portfolio123

IXJ is more diversified than XLV, which has almost 54% of asset value in the top 10 holdings and 19% in the top 2 (UNH and JNJ).

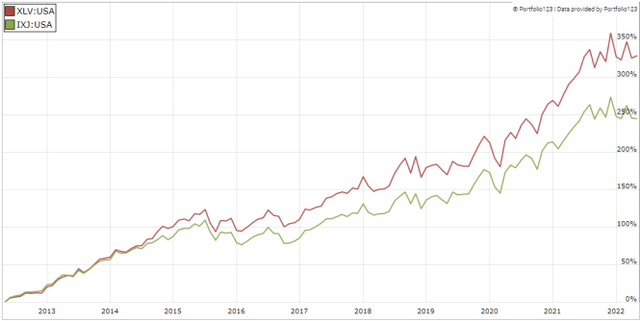

In the last 10 years, XLV has outperformed IXJ with a total return of 325% (15.6% annualized) vs. 241% (13.1% annualized). Risk measured in drawdowns and standard deviation of monthly returns is similar in both ETFs.

IXJ vs. XLV (Chart: Portfolio123)

IXJ may be an alternative to XLV for investors seeking an international exposure and a lower concentration in top holdings. If concentration is the only concern, the Invesco S&P 500 Equal Weight Health Care ETF (RYH) may be a better choice.

Dashboard List

I use the first table to calculate value and quality scores. It may also be used in a stock-picking process to check how companies stand among their peers. For example, the EY column tells us that a large pharma/biotech company with an Earnings Yield above 0.0454 (or price/earnings below 22.03) is in the better half of the industry regarding this metric. A Dashboard List is sent every month to Quantitative Risk & Value subscribers with the most profitable companies standing in the better half among their peers regarding the three valuation metrics at the same time. The list below was sent to subscribers several weeks ago based on data available at this time.

|

MRNA |

Moderna Inc |

|

INVA |

Innoviva Inc |

|

QDEL |

Quidel Corp |

|

COLL |

Collegium Pharmaceutical Inc |

|

OGN |

Organon & Co |

|

DVA |

DaVita Inc |

|

ORGO |

Organogenesis Holdings Inc |

|

THC |

Tenet Healthcare Corp |

|

QURE |

UniQure NV |

|

ITOS |

iTeos Therapeutics Inc |

It is a rotating list with a statistical bias toward excess returns on the long-term, not the result of an analysis of each stock.

[ad_2]

Source links Google News