")

[ad_1]

AlxeyPnferov

Main Thesis And Background

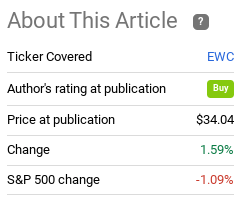

The purpose of this article is to evaluate the iShares MSCI Canada ETF (NYSEARCA:EWC) as an investment option at its current market price. This is a fund that is exclusively focused on Canadian equities, with a bias towards large and medium sized companies. I have owned and recommended EWC for a while, reiterating this stance back in August. Since then, EWC has continued to modestly beat the S&P 500:

Fund Performance (Seeking Alpha)

As I look ahead to 2023, I continue to believe Canadian equities should have a place in my portfolio. I have made some rotations throughout Q4, but EWC is one fund I plan on adding to, not divesting from. Even though the share price has risen a bit, in my view a buy case can still be made. I will explain why in the paragraphs below.

Why Canada? There Is No Silver Bullet Diversification Play Out There

To begin, I want to level set expectations on portfolio management. I personally see value in Canadian equities (and EWC by extension) and see the fund as a reasonable way to diversify from my U.S./Tech heavy portfolio. To me this is a no-brainer. But there are other ways one can diversify. Europe and Australia are competitive developed markets. And emerging markets like China and East Asia remain beaten down and could be potential value plays. In short, there are a number of different options – so why choose Canada?

In fairness, Canada is not the only non-U.S. investment I have. But I like the country and the expense of other riskier geographical regions. Canada is a mature, democratic country, with less geo-political risk than we are seeing in Europe and even Australia right now given its ongoing spate with China. There is some safety in North America given the continents locale away from some of the world’s more contentious areas. In addition, the nation’s large-cap stock index is heavily reliant on Financials and Energy. This is not necessarily “good” or “bad” as it depends on one’s own objectives and portfolio. But for U.S. investors like myself that are overweight the S&P 500 – and therefore large-cap Tech stocks – I see this exposure in a positive light.

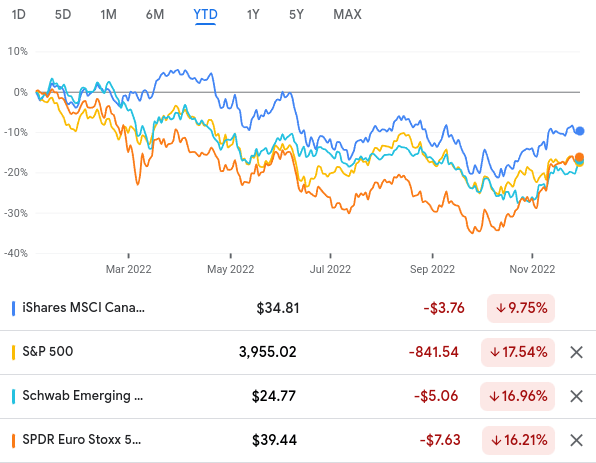

I think these are important because having some relative safety in my diversification tactic is important. This is because I don’t see any “sure thing” when it comes to any country overseas right now. They all have pros and cons, so why not pick one that has less political risk and has been a reasonable performer in a difficult year? (For perspective, the following graphic shows EWC’s performance, along with the S&P 500 and an Emerging Market Index and European index):

YTD Performance (Google Finance)

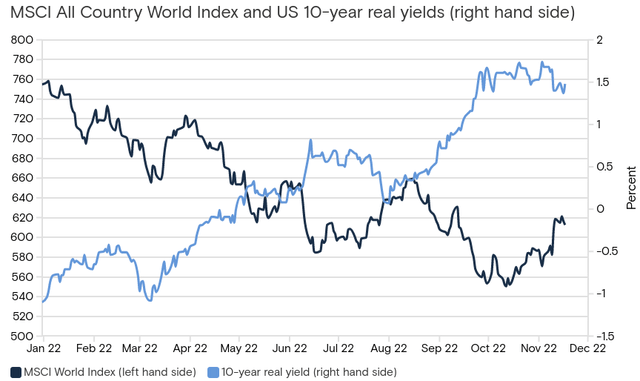

As you can see, EWC is a clear winner, although performance is still in the red. There is no getting around that, but the point I am making is there has not been a nation or geographical area that has been immune to the challenges of 2022. While some stocks and sectors, notably Energy, have been big winners this calendar year, broader country or region indexes have not. The “world” has been impacted as a whole by the Russia-Ukraine conflict, slowing economic metrics, and rising interest rates, especially in the United States. In fact, the World Index has been moving in a very clear inverse relation with the 10-year Treasury yield here at home:

Stocks vs. Yields (Goldman Sachs)

The point I am making here is that the globe has been impacted by many of the same factors. Nobody has really been immune, but some have handled it better than others. Canada is one such country, and I see a similar environment in early 2023 as we have now. This makes me continuously bullish on this exposure, even if the outlook is challenged by these macro-forces at the same time.

Canadian Consumers Have Been Resilient

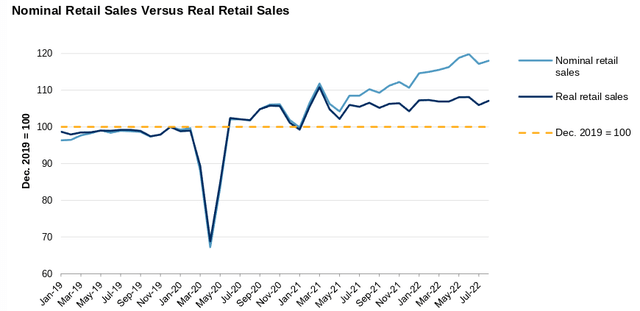

Digging deeper into Canada specifically, one bright spot has been the consumer. Despite a rising rate environment, inflationary pressures, and a gloomier economic environment, Canadian households have been willing to spend. While rising prices have sent sales up inherently, if we look at “real” sales figures (which factor in inflation), we still see growth in Canada on a year-over-year basis:

Retail Sales (Canada) (S&P Global)

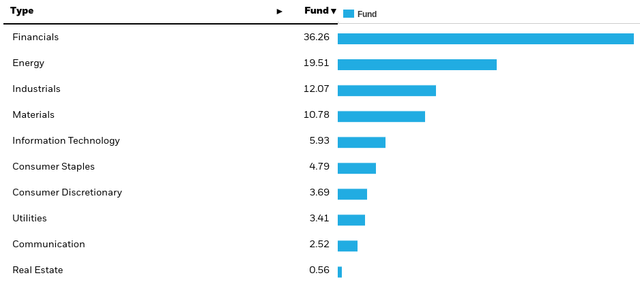

The conclusion I draw here is that household spending has continued to propel economic growth in Canada. This has been driven by a resilient labor market conditions and excess savings. Neither of these factors are guaranteed to persist in early 2023, but I don’t see a high likelihood of an immediate reversal. While EWC is not overly reliant on the Consumer directly, with only 8.5% exposure to Consumer Discretionary and Consumer Staples, a healthy consumer picture is still vital to overall economic health:

EWC’s Sector Weightings (iShares)

Ultimately, I see the consumer backdrop as favorable for equities as a whole right now. This should support EWC, even if the impact is mostly indirect. As long as Canadians are willing and able to part with their cash, the chances of a recession decline.

Bank Of Canada Is Slowing Pace Of Rate Hikes

As the chart in the prior paragraph shows, a bet on EWC is a heavy bet on the Canadian Financials sector. At over 36% total assets, one would have to be bullish on this sector idea in order to justify buying this ETF. Fortunately, I am, and that is a key reason I will be adding to my exposure through early 2023.

This stems from the fact that I see the interest rate environment in Canada as a bit of a “best of both worlds” scenario. Financials can benefit disproportionately from a higher rate environment as they pass on higher borrowing costs to their customers. But, raised rates too high, and the economy faces a restrictive environment that can lead to less loan/mortgage originations and a higher probability of delinquency or default. This creates a bit of a balancing act. Banks and other lenders want higher rates, but not to the point where they see demand dry up and/or their customers stop paying them back. So finding the right balance is key.

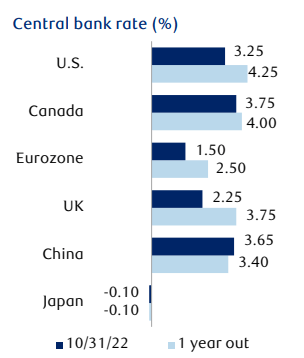

The good news is that I do believe Canada has the right balance. The nation has a higher benchmark than most of the globe, given its central bank started to raise rates sooner and more aggressively than its counterparts:

Global Benchmark Rates (1-year out is a forecast) (World Bank)

With this backdrop Canadian banks have been performing reasonably well, especially since widespread delinquencies have not been occurring.

The other side of the equation is how restrictive this level is. This brings us to the other set of good news – the Bank of Canada has started to pump the brakes at bit. This is evidenced by its decision to raise rates by “only” .50 basis points when it last met in late October:

Latest Move By Central Bank (Bank of Canada)

I view this positively because it demonstrates the Bank of Canada is being reactive to changing economic conditions. The growth outlook has moderated a bit, with probabilities of a recession rising. It is also taking in to account that interest rates in Canada are already high by global standards. With a less hawkish attitude, it should calm investors to a degree. But at the same token, the last action was still to raise rates, limiting the chances of a rate cut any time soon. To me, this signals rates will be at current levels for a while, and these are levels that should allow banks and lenders to grow their profits. As an owner of EWC, this is a win-win.

I Like The Energy Exposure, But It Also Presents Risks

Beyond Financials, Energy is a major component to the Canadian index that EWC tracks. Once we consider the Materials sector as well, we see that almost one-third of total assets are tied some way or another to commodity prices. This has served Canada well in the past, but it poses serious risks if the economy – domestic or global – declines into a prolonged recession.

Importantly, we can look at current conditions to see why this is a paramount risk. With Covid cases spiking in China, the government there has imposed some very strict lockdown measures. The resulting impact on oil (and other commodity prices) has been swift. While prices have rebounded a bit over the past week, they are still down sharply over the past month:

WTI Crude Spot Price (Bloomberg)

If 2022 has taught us anything about the oil market it is this. One, it will continue to be very volatile. Two, it has provided investors with a great hedge when everything else is seemingly floundering.

So – what does this mean? It suggests that if economic conditions are consistent in Q1 2023, then Energy is likely to have a good run and EWC is likely to benefit from it. But we have to also weigh the counter-argument, which is that economic conditions will weaken, oil prices will decline and/or be volatile with an emphasis on the downside, and this exposure will harm performance.

In my opinion this remains a reasonable place to be as we wrap up the year and begin a new one. But I will manage expectations by saying that every sector bull market runs out of steam eventually. If we see central banks continue to hike interest rates, China remains heavily locked-down, and investor worries mount, then Energy seems ripe for a downward correction. The sector has performed extremely well, and investors may be looking to take some chips off the table. This is especially true at the start of the year if investors were waiting for a fresh calendar before triggering tax gains. Therefore, while I remain an Energy bull and see this exposure as a tailwind for EWC, readers should give serious thought to the counter-argument that it could be a drag on performance going forward. This risk should not be ignored.

The Domestic Yield Curve Is A Reason For Buying Foreign

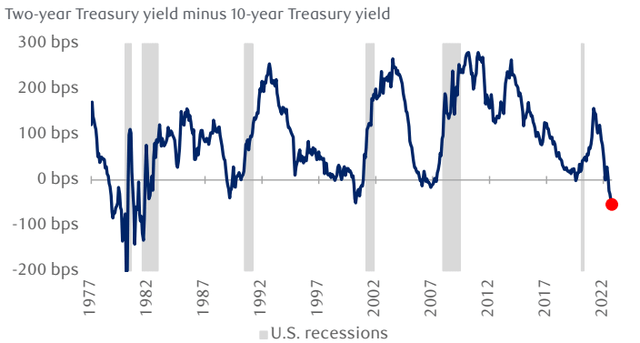

My final point touches on a key risk I see here at home – an impending recession. The U.S. has managed to perform very well coming out of the worst of the pandemic, but challenges remain. With interest rates elevated and consumer and investor sentiment very weak, a recession in 2023 is looking likely. The bond market is definitely telling us to prepare for one, as the treasury yield curves has reached its most inverted level since the Fed’s last inflation battle in the 1980’s:

Yield Curve (St. Louis Fed)

I am not trying to come across as overly alarmist. I have been raising my cash holding to be sure, but the bulk of my portfolio is still U.S. stocks. So while I have been divesting a bit, I am still heavily exposed to large-cap U.S. companies and am hoping for a strong year in 2023.

But I am planning for a difficult year. If the market surges and I make less than I otherwise would have, so be it. But after the run the indices have had over the past month, I am taking some short-term profit and waiting for better entry points on the S&P 500 and Dow. In the interim, aside from taking advantage of higher interest rates in savings accounts and municipal bonds, I am looking outside U.S. borders again for value. With the inverted yield curve telling me to be cautious domestically, I think Canada has plenty to offer. This is fundamental to why I am buying EWC at the moment – the relative economic potential.

Bottom-line

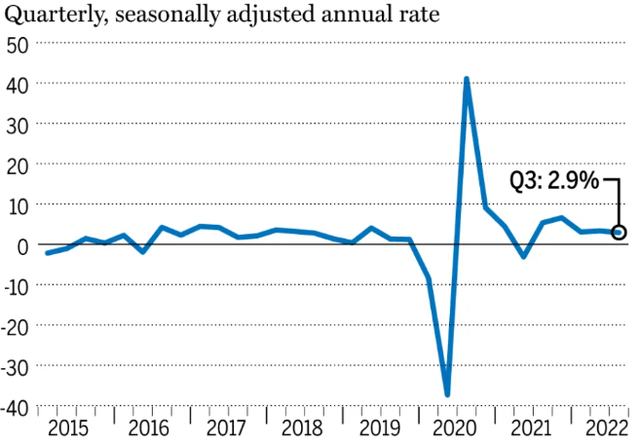

EWC has had its ups and downs in 2022 and, to be fair, it has been mostly down. But the fund has recently gotten a bit higher and I see that as a sign to have confidence going forward. In relative terms, Canada has been a reasonable place to hide out. The economy is developed, quite stable by global standards, and continues to chug along in positive growth territory:

Canada’s GDP Growth (Quarterly) (Yahoo Finance)

When looking overseas for exposure, Canada’s growth story here seems like a safer bet to make. I trust developed markets more than emerging markets right now will all the headwinds facing the world. This, combined with sectors that will benefit from a continued higher interest rate and inflationary backdrop, makes EWC a good spot to park some cash. Therefore, I reiterate my “buy” rating on this fund, and encourage readers to give it some thought as we approach the end of the year.

[ad_2]

Source links Google News