")

[ad_1]

Midstream MLPs are a very popular investment in the Seeking Alpha dividend investment community and for good reason. Midstream MLPs offer strong growth prospects, cheap valuations, and very juicy tax-advantaged distribution yields. The ALPS Alerian MLP ETF (AMLP) is the most popular ETF in this industry, with over $8.5 billion in AUM, so I thought taking a look at the fund might be of interest to readers and investors.

AMLP tracks a broad-based index of U.S. midstream MLPs and yields a whopping 8.10%. Although the fund seems, at first glance, to be a perfect choice for dividend investors or those looking for MLP exposure, I don’t believe this to be the case. AMLP’s excessive 0.85% expense ratio and tax-inefficient structure mean most investors would achieve substantially higher total shareholder returns by investing in other funds or in MLPs directly. As such, I believe that AMLP is a particularly poor investment choice and should be avoided.

Fund Basics

- Sponsor: Alerian

- Dividend Yield: 8.10%

- Expense Ratio: 0.85%

- Underlying Index: Alerian MLP Index

- Holdings: 23

- Subject to 21% corporate tax rate

Fund Overview

AMLP is administered by Alerian, an investment management firm focusing on energy infrastructure corporations and MLPs. AMLP tracks the Alerian MLP Index, provided by the same company, a market-cap weighted index of U.S. midstream MLPs with a minimum market capitalization of $75 million. Midstream corporations are excluded, as are energy companies specializing in other energy industry sectors, as are most micro-caps. Interested readers can take a look at the fund’s methodology here, but I think I’ve included the most relevant points.

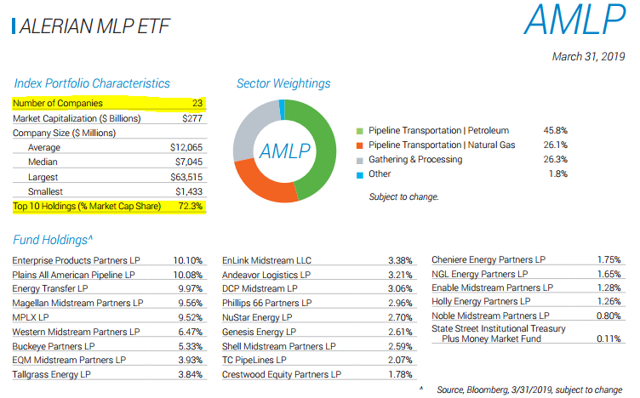

AMLP focuses on a rather niche sub-industry, U.S. midstream MLPs. As such, the fund’s holdings are comparatively few in number and relatively concentrated, this isn’t a low-risk, highly diversified ETF.

(Source: AMLP Fact Sheet)

AMLP’s holdings are also somewhat tilted towards higher-yielding, lower-quality stocks, as most blue-chip companies in this sector, such as Enbridge (ENB) and TC Energy (TRP), are organized as corporations.

AMLP was clearly meant to provide broad-based exposure to midstream MLPs to investors. Although there is definitely some logic to this, I believe that the fund’s exclusion of corporations from its holdings is a significant drawback for investors, as:

- It forces the fund to structure as a corporation and pay applicable corporate taxes, decreasing shareholder returns.

- It is partly responsible for the fund’s excessively high fees, also decreasing shareholder returns.

- It has caused the fund to significantly underperform relative to its benchmark, something very rare for an index fund.

- It is partly responsible for the fund’s historical underperformance relative to its peers, a situation that I believe is likely to continue into the future.

Corporate Structure and Taxes

First a bit of context. MLPs are generally a very tax-efficient investment. MLPs themselves are not liable for corporate taxes, although their shareholders are generally required to pay somewhat higher income taxes and file a special K-1 tax form. In practice, shareholders are usually able to defer these extra taxes due to certain tax benefits, and the burden is usually very light, so the situation is a net benefit for most MLP investments. AMLP is unable to benefit from these tax breaks, as the fund is primarily invested in MLPs:

Under current law, the Fund is not eligible to elect treatment as a regulated investment company due to its investments primarily in MLPs. The Fund must be taxed as a regular corporation for federal income purposes.

(Source: AMLP Fact Sheet)

Corporate taxes can be very hefty, so this is a significant negative for the fund and its shareholders. AMLP has had to pay an effective corporate tax rate of 12-14% in the past, directly decreasing total shareholder returns by the same amount. Moving forward, the fund’s effective tax rate will most likely decrease, due to the recent spate of corporate tax cuts, and as the fund is carrying sizable losses from previous years, but the situation is still far from ideal.

On a more positive note, AMLP’s investors don’t have to file a complicated K-form, and most of the fund’s dividend consists of tax-deferred return of capital distributions. Taxes are higher when turnover is greater, and that includes situations when MLPs convert to corporations, as the fund excludes the latter from its holdings.

AMLP is simply too tax-inefficient of an investment vehicle. Most investors would pay substantially less in taxes, and therefore receive substantially higher total shareholder returns, by investing elsewhere.

See here for more information about the fund’s tax situation.

Excessively High Fees

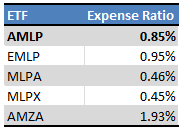

AMLP’s corporate/tax structure also complicates matters for the investment manager and is partly responsible for the fund’s very high expense ratio of 0.85%. Although most funds in this particular industry subsector are very expensive, two funds, MLPA and MLPX, are significantly cheaper:

(Source: Chart by Author)

AMLP’s very high fees are, in my opinion, a dealbreaker. Index funds are rarely this expensive – it makes very little sense to overpay for passive management, especially so considering that AMLP has comparatively few holdings. The fund’s excessive fees only serve to decrease total shareholder returns, as we shall soon see.

Underperformance Relative to Benchmark

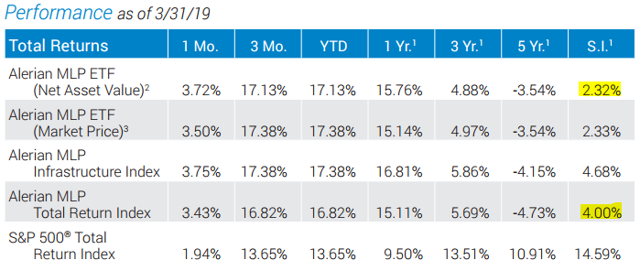

AMLP’s taxes and fees have been a very sizable drag on the fund’s past performance, and have prevented the fund from accurately replicating the performance of its index. AMLP’s annual total returns since inception have been 1.7% lower than its underlying index – a staggering amount. Extremely few index funds underperform their benchmark by this much. On a slightly more positive note, the fund’s performance has significantly improved during the past few years due to not being liable for corporate taxes during the same time period.

(Source: AMLP Fact Sheet)

Investors are paying excessive fees and taxes for very subpar performance. More importantly, the fact that AMLP has underperformed its index for so much means the fund is simply not an adequate investment vehicle to achieve its intended goal. Investors are not getting what they are paying for.

Underperformance Relative to Peers

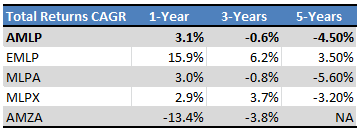

AMLP compares somewhat unfavorably to most of its peers. The fund generally underperforms, and its relative performance isn’t measurably improving:

(Source: Chart by Author)

AMLP’s underperformance is, in my opinion, due to the issues previously raised: excessively high fees, inefficient tax structure, and lack of investments in midstream corporations. It is not a coincidence that the First Trust North American Energy Infrastructure ETF (EMLP) and the Global X MLP & Energy Infrastructure ETF (MLPX), the best-performing funds, both invest in corporations; diversification is almost always a benefit for investors, and excluding the strongest midstream corporations from a fund is simply not a good idea.

Conclusion and Alternatives

AMLP offers investors a simple way to invest in midstream MLPs. Although this is a reasonable investment objective, the fund’s excessively high fees and taxes have led to subpar investor performance in the past, and are likely to do so in the future. Investors looking for investment opportunities in the midstream space should consider alternatives. MLPX is a particularly strong fund in this industry, due to its strong performance and comparatively low fees and taxes. I previously wrote about MLPX here. I also think creating a personal portfolio of MLPs is easily doable, as there are simply not that many companies in the industry.

Thanks for reading! If you liked this article, please scroll up and click “Follow” next to my name to receive future updates.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

[ad_2]

Source link Google News