[ad_1]

sx70

The pandemic tailwinds spurred a phenomenal rally in the speculative growth names. The great expectations rebound that followed the March 2020 sell-off opened the door for higher investor demand for funds targeting specific growth-rich equity baskets, and the asset management industry responded with a slew of ETF launches.

The Invesco Nasdaq Next Gen 100 ETF (NASDAQ:QQQJ) was born in October 2020, when mid-size tech stocks that, in theory, should bear solid growth premia were still in the limelight. Yet the capital rotation had already begun, and the issue is that 2021 was dominated by a different narrative, noticeable for an end of the so-called ‘value drought’ of the 2010s. And the growth style fell out of favor.

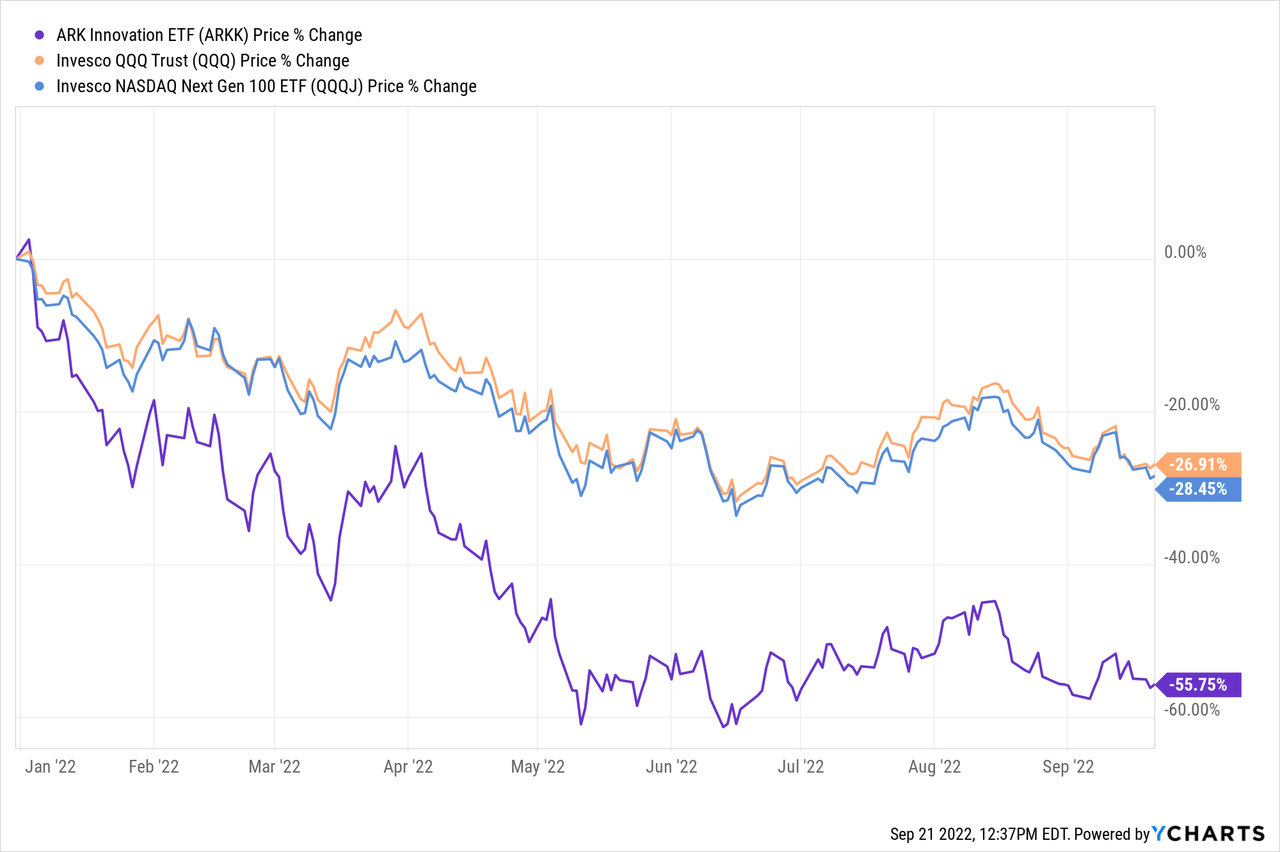

Later, 2022 has not put in a period like the pandemic days outperformance completely, actually throwing it into reverse. Examples of dismal performance are aplenty, from the Invesco QQQ ETF (QQQ), a bellwether tech names cohort, and ARK Innovation ETF (ARKK) to, of course, QQQJ, which is supposed to represent names that are yet to qualify for the elite Nasdaq 100.

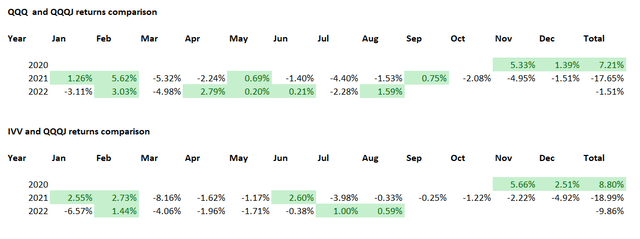

To investor chagrin, this ETF was late to the party. The music did not stop completely in 2021 as it advanced by ~9.8%, yet the last months of the year had already been something of a dire warning as its return was negative in both November and December as investors started to slowly position for an end of the ultra-loose monetary policy in 2022. Back then, it underperformed both the iShares Core S&P 500 ETF (IVV) and QQQ.

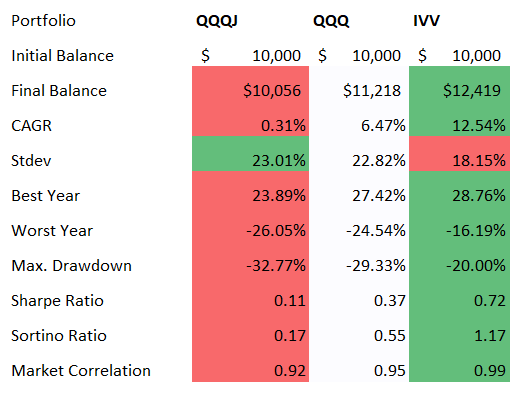

Created by the author using data from Portfolio Visualizer

This year, its strategy has been under heavy pressure, despite comparatively strong July and August dominated by the bad news is good news narrative. As a consequence, its returns in the November 2020 – August 2022 period are weaker both compared to the S&P 500 ETF (which fared better thanks to the value component) and QQQ, while its standard deviation was the highest.

Created by the author using data from Portfolio Visualizer

Inflation is surprisingly persistent, and the suggestion that the July CPI and PPI data were the harbingers of price growth returning to normalcy and the prospect of a full-scale recession dissipating appeared to be a premature one. And as massive interest rate hikes are looming, this is not an environment to top up allocations to pricey mid-size equities, especially from the IT and communication services sectors.

The fund’s investment mandate is to track the Nasdaq Next Generation 100 index, which is supposed to represent the one hundred largest companies outside of the Nasdaq 100. Precisely like in the case of its bellwether-focused counterpart, financials cannot qualify for inclusion.

QQQJ’s investment strategy was a perfectly calibrated one for the pandemic market, and, in fairness, could be a beneficiary of the tech-dominated bull run of the 2010s. At least, the backtested index data going back to December 2009 included by Nasdaq in the NGX Relative Performance vs. US Funds presentation are supportive of this suggestion.

What is under the hood at the moment? We see 99 equities, with the top ten accounting for 22%. The weighted-average market capitalization stands at around $17.99 billion, as of my calculations, which implies the mix is less of a mid-cap one, tilted towards players I would call the novices in the large-cap echelon. These names should have comparatively higher quality than their smaller counterparts, yet also stronger upside potential and more robust growth prospects compared to mega-cap bellwethers. However, in the bear market, the quality factor is of greater importance.

It should be noted that QQQJ does have a footprint in the mega-cap universe, yet via just one stock, Sanofi (SNY), a ~$100 billion French pharmaceuticals company, with less than 1% allocated. Mid-caps (sub-$10 billion) have a comparatively significant share of the net assets, close to 18%, yet not large enough to define the fund’s price trajectory.

Sectors that dominate the mix are tech (38.6%), healthcare (20%), and consumer discretionary (12.9%). In line with the index methodology, financials are absent. Besides, there are trace amounts of energy, materials, and utilities stocks. Each sector is represented by just one company. Together, they account for only 4.3%. For example, Diamondback Energy (FANG), a $28.7 billion oil & gas company, has ~1.92% weight.

Surprisingly, QQQJ is not as terribly valued as one might assume by looking at the sector allocation. There is a meaningful share of high-quality stocks. However, nuances deserve attention.

As of my calculations, the weighted-average EV/Sales ratio stands at 6.9x, while P/S, a similar multiple but unadjusted for debt, comes at 6.6x. Let us be crystal clear, this is not cheap, at all, even by the traditionally generously priced tech sector standards. The median multiples for it are 2.7x and 2.62x, respectively. Also, the rather expensive healthcare sector has median EV/S and P/S at 4.16x and 4.38x.

Delving deeper, almost 57% of the QQQJ holdings have a D- Quant Valuation grade or worse. Yet this is much better compared to the elite QQQ, which is burdened by ~76% of comparatively overpriced companies (this certainly has something to do with the size premium). Also, in QQQ, value names account for just 6.9% of the portfolio, and the smaller peer beats it here with ~16.2%.

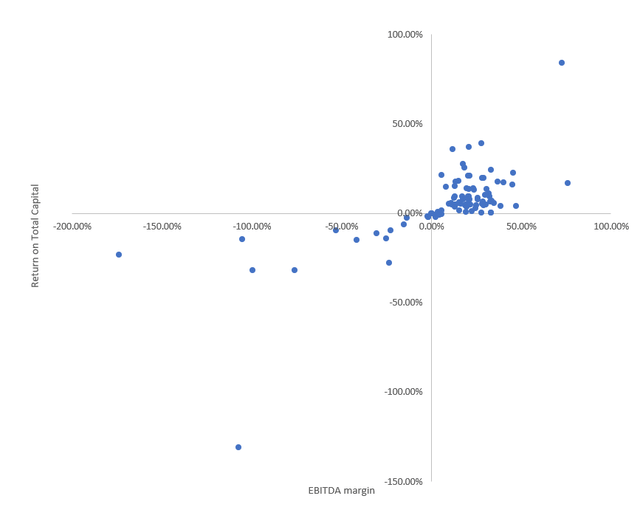

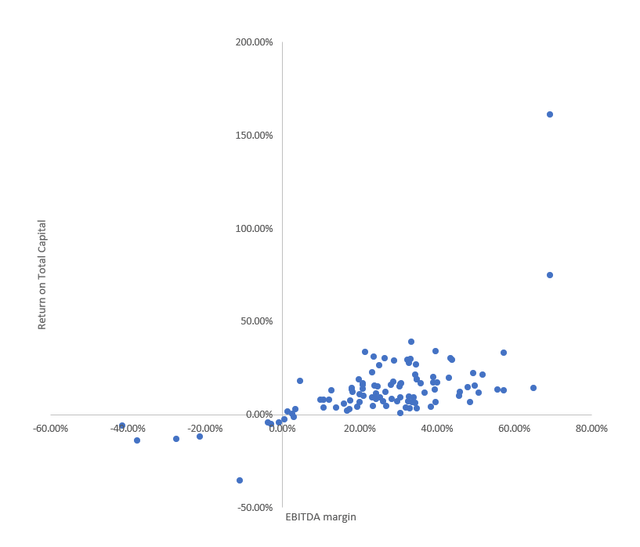

For the quality factor, it would be pertinent to include the following scatter plot combining the EBITDA margins and Returns on Total Capital.

QQQJ holdings analysis (Created by the author using data from Seeking Alpha and the fund)

Here is another chart summarizing the same metrics for the QQQ players. Investors can judge by themselves which one has an edge regarding quality, while I should note that QQQJ clearly has more outliers with dreadful margins and returns.

QQQ holdings analysis (Created by the author using data from Seeking Alpha and the fund)

Finally, just 69 stocks in QQQJ have a B- Profitability grade or better (~81% of the net assets), and QQQ is way ahead here, with 97 and ~99% weight. This is more likely a direct consequence of the size factor, as smaller companies tend to have weaker fundamentals, and vice versa.

Final Thoughts

A due remark should be made on expenses. In short, they are comparatively comfortable, at just 15 bps. Yet, there are other factors that make QQQJ a risky investment at the moment.

Doves are not in vogue. Investors are no longer discussing a quarter percentage point hike. It simply looks faint. Serious measures are needed, and the market now expects a range between 75 and 100 bps. No doubt, the recession risk increases. In this environment, investing in an expensive and volatile equity basket with quality softer compared to the market is a precarious move. In this regard, I believe it is worth watching from the sidelines.

[ad_2]

Source links Google News