")

[ad_1]

imaginima/E+ via Getty Images

Even in a bear market, Vanguard Total World Stock ETF (NYSEARCA:VT) is one of the best ETFs you can buy for the long run. Investors seeking a diworseified refuge from current market conditions may want to consider this fund.

Diworseification Isn’t All That Bad

One of the main critiques about VT is that it diversifies into underperforming markets, thus lowering the fund’s total return. Yes, and that is by design.

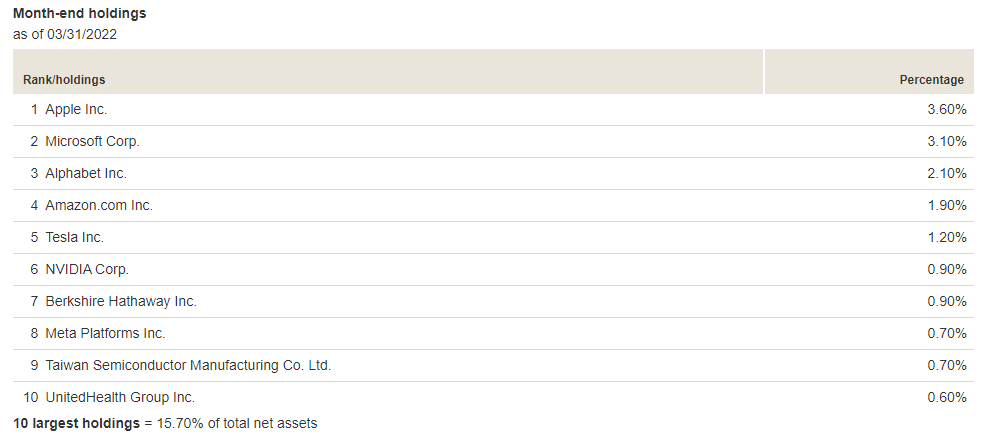

VT is an ETF that seeks exposure to companies across every market sector, geography, and currency. With exposure to over 9,500 stocks in free-float-adjusted market-cap-weighted proportions, it holds nearly every publicly-traded stock in the world. For the month ending March 2022, its top 10 holdings shown in the table below accounted for nearly 16% of the fund. For a fund that owns shares in almost every company in the world, it is amusingly concentrated towards the US market. Indeed, US equity constitutes nearly 60% of this fund’s holdings.

VT’s top 10 equity holdings constitute a small part of its portfolio. (Vanguard)

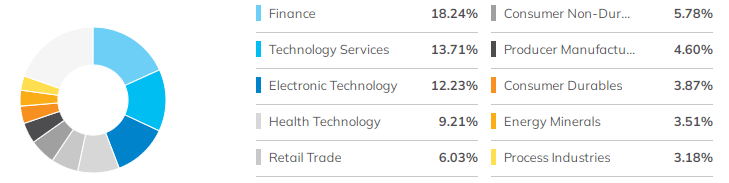

From a diversification standpoint, this is the most equity diversification you could ask for. The Vanguard 500 Index Fund ETF (VOO), for example, has its top 10 holdings constituting 30% of the fund. By holding market-cap weights of virtually every company on Earth, VT becomes the Vanguard ETF that tries hardest to get its shareholders the highest risk-adjusted return possible. These companies are even decently spread out across all sectors, as shown in the figure below.

VT’s sector exposure is well diversified. (ETF.com)

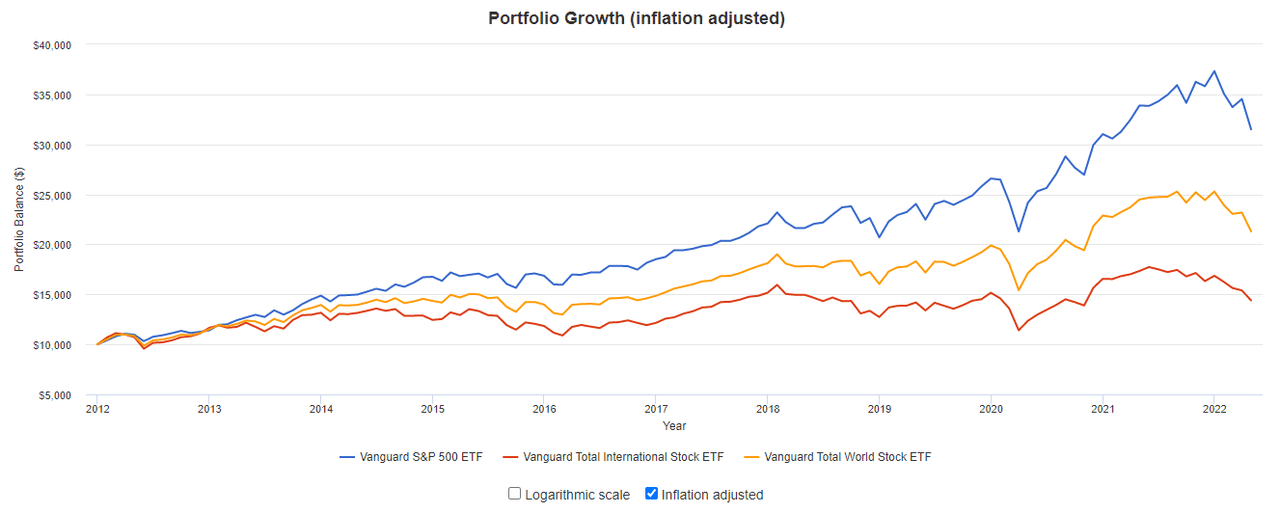

In the short run, however, diversification’s implied promise of impeccable risk-adjusted returns may not be kept. In the figure below, VOO, in blue, beat out VT, in yellow, by almost 4% annualized with a slightly lower standard deviation. This is largely due to the poor performance of international equity, approximated by the Vanguard Total International Stock Index Fund ETF (VXUS). Investors who were long on US equity doubled their money since the COVID-19 flash crash, but the same cannot be said for investors in the global stock market. Still, there are two things that are worth considering.

VT underperforms the S&P 500 over the last 10 years. (PortfolioVisualizer)

The first thing is that betting on VT means you did not have to bet on the US. There is a certain margin of safety in doing so because it protects you from the case where the US substantially underperforms the global market. There are arguments that US markets will always be the most prosperous, but these arguments may not materialize. In fact, the US market hasn’t generated the largest returns historically; that honor belongs to the Australian market. US markets haven’t even been the largest in the world forever. Countries take turns dominating the global market capitalization, and there is nothing to say that the US won’t eventually be superseded by another nation. You could argue that the US will continue to outperform over your investing horizon, but you could also argue that it’s not worth taking that gamble with your financial future.

The second thing is that for everyone long on the US market, there is someone short on the US market. For everyone who made a fortune betting on the S&P 500, there is someone who lost a fortune betting against the S&P 500. The shares of foreign companies don’t disappear when seemingly nobody is interested. Someone has to be holding the bag. Everyone needs to own everything, so everyone owns the market portfolio – the global market portfolio. This means that the world will, on average, match the returns of VT. This puts you at the 50th percentile of returns before fees, which isn’t all that bad. After fees, however, this ends up making you quite a bit above average; the only fee you pay is $7/year on $10,000 invested. If markets continue to be as efficient as they are, your outperformance is very likely. Nearly 80% of fund managers failed to beat the market last year after fees, but this wouldn’t have happened to you.

Creating A Two-Fund Portfolio With VT

I do not regard VT as a one-fund portfolio like a target-date fund because concentrating all of your portfolio into one asset class is inherently dangerous. Peculiar is the investor who uses the safest stock ETF to pursue the riskiest investment strategy sans leverage – even the leverage crowd takes advantage of risk parity. 100% VT is dangerous for the same reason why 100% stock portfolios in general are dangerous; VT is subject to violent drawdowns that can take years to recover. Certainly, via VT you are already exposed to stock markets that haven’t recovered since 2008, or even earlier, since the 1990s.

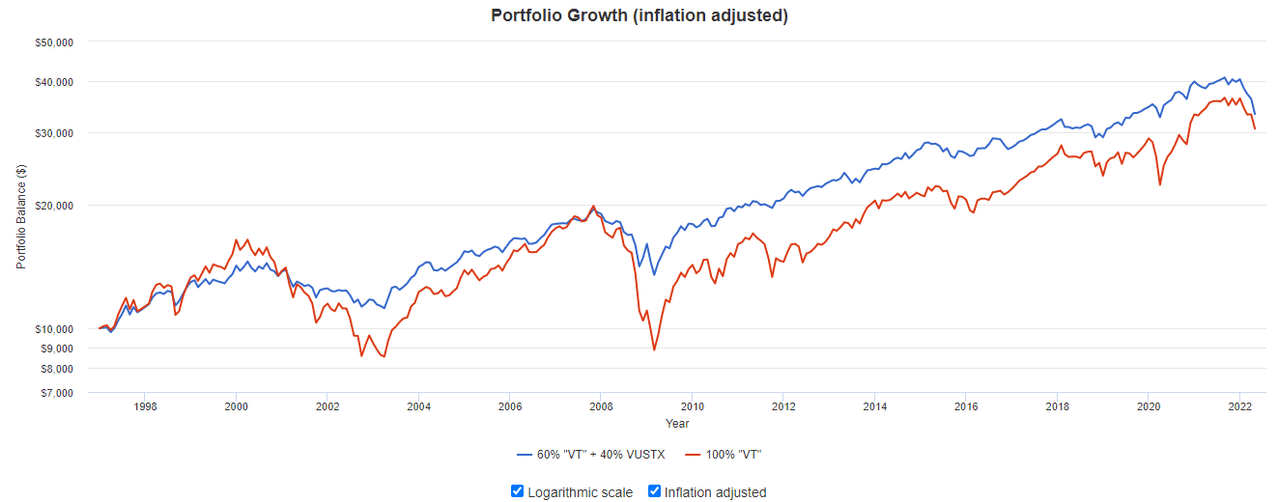

I would pair VT with a long-term bond fund like the Vanguard Long-Term Treasury Index Fund (VUSTX) to reduce volatility. In this article, I wrote about how long-term Treasuries compliment stock index funds to minimize drawdown and return standard deviation while increasing risk-adjusted returns better than any other asset class. Below is a graph of 60% “VT” and 40% VUSTX and 100% “VT”. In this case, “VT” is simulated by 50% VTSMX and 50% VGTSX, which has been a good approximation to the real VT since its inception.

Pairing VT with bonds can improve risk-adjusted returns over a 100% stock portfolio. (PortfolioVisualizer)

As is consistent with modern portfolio theory, a balanced stock-bond allocation can dramatically minimize an investor’s volatility while capturing the majority of the upside. In this case, maximum drawdown is halved and standard deviation is down 40%. Due to rebalancing, the stock-bond portfolio even beat out the 100% stock portfolio.

This approach is based on Taylor Larimore’s Three-Fund Portfolio, which constitutes a Total US Stock Market Index Fund, Total International Stock Market Index Fund, and Total Bond Market Index Fund. However, Mr. Larimore prefers 20% allocated to international equity, which invalidates VT as a simple investment. If you want global market-cap weights, then you could very well simplify Mr. Larimore’s three funds down to two funds by using VT. Mr. Larimore also prefers a total bond market index, and in a recent interview, Dr. William Bernstein even suggested short-term Treasuries. It seems that nobody can agree on this, so I still stand by my opinion of using long-term Treasuries. As Marco Pierre White says, it’s your choice.

Some Reasons You Might Not Want VT

I do not own VT in my own portfolio, but I do use a combination of other funds to approximate VT’s holdings. This is slightly more labor-intensive on my end, but it does not impact my ability to stick to my investment plan. It’s more enjoyable to put my money into two funds instead of one fund, and I feel like I’m doing something special. That being said, I would have no qualms replacing my non-tilted equity holdings with VT since it is not substantially different from what I’m doing anyway.

Everyone has their own financial goals, and VT’s equity holdings may not be in line with everyone’s needs. If your home country is underrepresented in VT, you might find significant currency volatility. You may opt to bias your portfolio towards your home country’s equity holdings, in which case VT becomes irrelevant. If you are a citizen of anywhere outside of the US, you should probably not purchase VT and instead look at equivalent tax-efficient funds. For example, if you are a citizen of the EU, you might end up choosing the Vanguard FTSE All-World UCITS ETF (VWCE). Choose the ETF that gives you the best deal.

Buy VT Today

As far as whether the average retail investor should buy right now, well, yes, absolutely. You’ll be in it for the long game. If stocks keep going down, then that’s unfortunate, but you’ll still be doing better with VT compared to 90% of active funds after 20 years. If stocks go up, then you’ll be glad you bought the dip. I do expect stocks to plummet a bit further, but I’m not concerned about finding the bottom. Most investors’ dollar cost average into their portfolios anyway, so market timing errors eventually come out in the wash.

Seeking Alpha’s Quant gives VT a Buy rating with 3.65/5. It’s always nice when the machine learning algorithms agree with an investor’s intuition. Right now, the P/E ratio is hovering around the historical average, so we should expect average returns going forward. This is around an annualized 8%.

At the end of the day, there are far worse strategies out there than investing in capitalism. While investing in VT is not going to make you a billionaire, its returns will probably be good enough if you have some time on your hands.

[ad_2]

Source links Google News