[ad_1]

Editor’s note: Seeking Alpha is proud to welcome FM Research as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

imaginima/iStock via Getty Images

Vanguard’s Total International Stock Index Fund ETF (NASDAQ:VXUS) remains a strong buy. Ex-U.S. equity in general has garnered a sour reputation over the last decade, but there is a bull case amid the worrisome recent performance.

Fund Management At Its Best

VXUS is a massively diversified fund that stakes ownership in over 7,800 businesses across the globe, guided by tracking the FTSE Global All Cap ex-U.S. index. As far as safe bets go, the average investor will be hard-pressed to find any fund more secure for their money. Investing in VXUS grants exposure to stocks across 46 countries, stocks from many of which are inaccessible via U.S. markets directly. A noteworthy number of these stocks are worth paying attention to, if not for their business fundamentals but for their rapid growth.

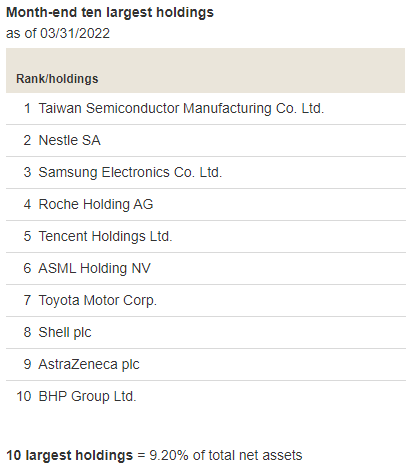

VXUS holds formidable companies such as Taiwan Semiconductor Manufacturing Co. Ltd. (TSM) and ASML Holding N. V. (ASML), which are up over 200 and 350% over the last 5 years, respectively. With returns comparable to those of Apple (AAPL), hundreds of these ex-U.S. businesses are driving global corporate profits, catering to billions of consumers from all corners of Earth.

After all, ex-U.S. industries represent roughly 40% of the free-float-adjusted market-cap-weighted global market, and these are companies investors lack exposure to in typical S&P 500 or total U.S. stock market ETFs. Bear in mind that the companies which own name-brands such as Toyota (TM), Shell (SHEL), Louis-Vuitton (OTCPK:LVMUY), Samsung (OTC:SSNLF), and fan-favorite Nintendo (OTCPK:NTDOY) are based outside of the U.S. Samsung and Toyota are even in its top 10 holdings, among other household names as indicated in Vanguard’s table below.

Interestingly, the top 10 holdings don’t even account for 10% of the total net assets – compare this to an S&P 500 index fund where the top 10 assets constitute a whopping 30% of net fund assets. For typical long-term investors who wish to avoid uncompensated risks and are wary of holding a significant portion of their retirement accounts in any one company, VXUS’s extreme diversification might be desirable.

Top 10 holdings of VXUS (Vanguard Group, https://investor.vanguard.com/etf/profile/portfolio/vxus)

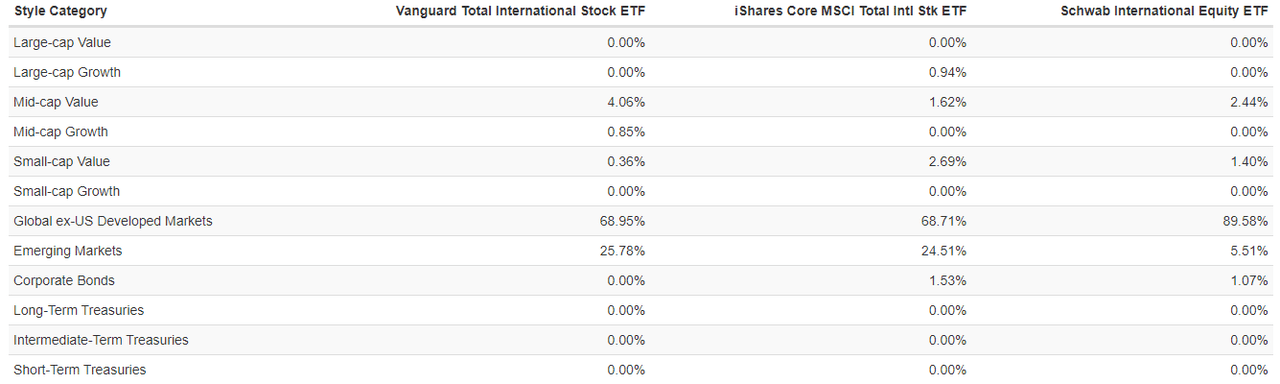

As an ex-U.S. stock ETF, VXUS is notable in that it does not shy away from emerging market assets; VXUS holds roughly 25% of its assets in this risky asset class. The underlying index is important because not every international index treats emerging markets the same way, and choosing an international fund among the sea of potential funds can be tricky. For comparison, take two of VXUS’s competitors: the iShares Core MSCI Total International Stock ETF (IXUS) and the Schwab International Equity ETF (SCHF). While IXUS’s asset allocation is close to that of VXUS by tracking the similar enough MSCI ACWI ex-U.S. IMI index, SCHF foregoes comparable emerging market exposure by tracking the FTSE Developed ex-U.S. index, despite having “International Equity” in the name.

VXUS also beats out IXUS’s roughly 4,200 holdings. While the diversification benefit of holding those extra few thousand companies is probably minimal, it is clear that Vanguard is giving you all the international equity exposure they can get their hands on, all the way down to their choice of index. Other differences in asset allocation are provided by Portfolio Visualizer in the table below.

Asset allocation breakdown of three international equity funds: VXUS, IXUS, and SCHF. (Portfolio Visualizer)

Investors seeking exposure to over 7,800 companies would expect to pay significant custodial fees for the privilege, but they would be mistaken. In fact, Vanguard even recently lowered expense ratios for this fund from dirt cheap to even cheaper. Investors have an opportunity to benefit from Vanguard’s half century of fund management expertise for pennies on $1000 invested. This combination of quality and price is something that struggles to be rivaled against by even the most elite ETFs. The expense ratio of 0.07%, as is the case with many Vanguard funds, remains orders of magnitude below the industry average of 0.41%.

Vanguard remains a trailblazer for giving the retail investor their fair share of market returns, and they carry on the tradition with VXUS. For those unfamiliar with expense ratios, these 34 basis points, exponentially compounding over an investing lifetime, can mean the difference between an early retirement and an extra decade of service. Vanguard ETFs also do not distribute capital gains, making VXUS more tax efficient than funds that do distribute these gains.

For investors worried about purchasing assets at desirable prices, it is true that shares of VXUS are traded like shares of any other stock. Instead of being purchased at the NAV of the underlying stocks at the end of a trading day, VXUS share prices are determined by the market. However, shares of VXUS are liquid enough that this is largely insignificant.

Investors have already taken notice of the tremendous value this ETF has to offer. With a turnover rate under 8%, investors are generally complacent holding their money here. Total assets of Vanguard’s Total International Stock Index Fund, of which VXUS is the ETF share class, recently exceeded $386 billion. Among all funds, this is amusingly neck-at-neck with the total fund assets of the legendary SPDR S&P 500 ETF Trust (SPY).

A Decade of Lackluster Performance

A stellar surface assessment of VXUS, however, does not explain its mediocre, market-trailing performance as of late. It is no secret that international equity has been dismissed over the last decade as investors are quick to point towards astronomical U.S. market returns as the opportunity cost of investing internationally. After all, while the S&P 500, using SPY as a proxy, boasted a compounding annual growth rate of nearly 15% over the last 10 years, VXUS did not even graze 6% in the same time period. Indeed, this means that while SPY could have doubled your money twice since the subprime mortgage crisis, VXUS would not even have doubled your money once. Even after the COVID-19 flash crash, VXUS’s recovery has not been nearly as stellar as that of SPY.

In many ways, this makes sense. Geopolitical conflict, including literal wars, are adversely affecting international markets and even shutting them down outright. This happened as recently as late February. Concerns about emerging market stability, for example with recent volatility in the Chinese markets due to government intervention that dragged mega-cap stocks down to single-digit P/E multiples, does not instill confidence either. Furthermore, given that the U.S. is handling inflation remarkably well in light of some international currency crises, the elephant in the room concerning the Turkish lira, it can be extremely tempting to hang onto the relative power of the U.S. dollar and invest exclusively in U.S. equity.

To be fair, investors with portfolios long on 100% U.S. markets are in good company with some of the best investors of all time. Successful U.S.-centric investors such as the late Vanguard founder Jack Bogle have even discouraged investors from investing overseas. That said, our hero Mr. Bogle admits he’s in the minority and suggests investors to think for themselves.

Why You Should Invest in VXUS Anyway

As is the case with all negatives, there is light at the end of the tunnel. The fact that the S&P 500 has outperformed VXUS is not significant on the time scale markets operate on. We also know that past performance does not predict future results, and if we have learned anything from our predecessors, we know that oftentimes the opposite is true. Reversion to the mean plays do happen, and they are happening right now.

Ray Dalio of Bridgewater Associates, for example, has a long position on emerging markets via a number of ETFs, and while that is certainly incurring tremendous risk and probably inadvisable for retail investors, VXUS allows us to hedge 75% of that risk with developed market equity. Other investing legends such as Charlie Munger and Mohnish Pabrai have entered multi-million dollar positions on the emerging market powerhouse company Alibaba, which further suggests that the big dogs are already seeking opportunities overseas.

There are also arguments that U.S. equity is overvalued. These arguments are well-founded. The historical average P/E ratio of the S&P 500 hovers around 16x over the last century and a half, but currently this market index has a multiple well over 20x. The Shiller CAPE, another popular metric that tracks market expensiveness, has even reached levels comparable to the dot-com bubble. As a reminder, the dot-com bubble was a disaster. On the economic policy end, there are speculations that quantitative easing and rampant inflation are eventually going to spell doom for the U.S. economy. The list goes on and on.

For investors who are uneasy about the current economic situation in the U.S., exposure to a slightly uncorrelated asset class that in theory generates comparable risk-adjusted returns, namely via the affordable VXUS, may make sleeping at night a bit easier. Subscribers to modern portfolio theory may want to secure a fraction of their portfolios dedicated to ex-U.S. equity anyway, regardless of personal sentiment. Conventional wisdom recommends investors allocate 20% of their equity overseas. For those especially concerned about currency stability, VXUS also partially acts as a currency hedge for those who worry that the USD rate of inflation will exceed the global average.

VXUS, notably, boasts a relatively consistent 3% dividend yield. For investors who shy away from modern-day Treasury bond yields and rising interest rates threatening the bond market, VXUS can potentially serve as a hybrid investment that seeks the risk premium of stocks while securing fixed income. While some foreign taxes are withheld for U.S. citizens, these are often recoverable in your tax refund – VXUS is one of the funds where investors are eligible for a foreign tax credit due to its high allocation to ex-U.S. assets. Aggressively oriented dividend growth investors may also be interested in VXUS because of its reasonable dividend yield that has historically exceeded that of the S&P 500. Certainly, 3% is already beating out some Treasury bonds.

Perhaps the biggest reason to invest in VXUS is that the market is pessimistic about it, and this has been priced in. Shares are trading at almost 12x earnings, which places this fund at value levels. Growth has outperformed value in recent years, but Nobel laureates have shown us that value ought to beat out growth in the long run. In addition to its apparent value status, VXUS is one of the few international funds that seeks exposure to small cap equity; occasionally, index funds will gloss over small caps because of liquidity risks, and thus forfeit any small-cap premia.

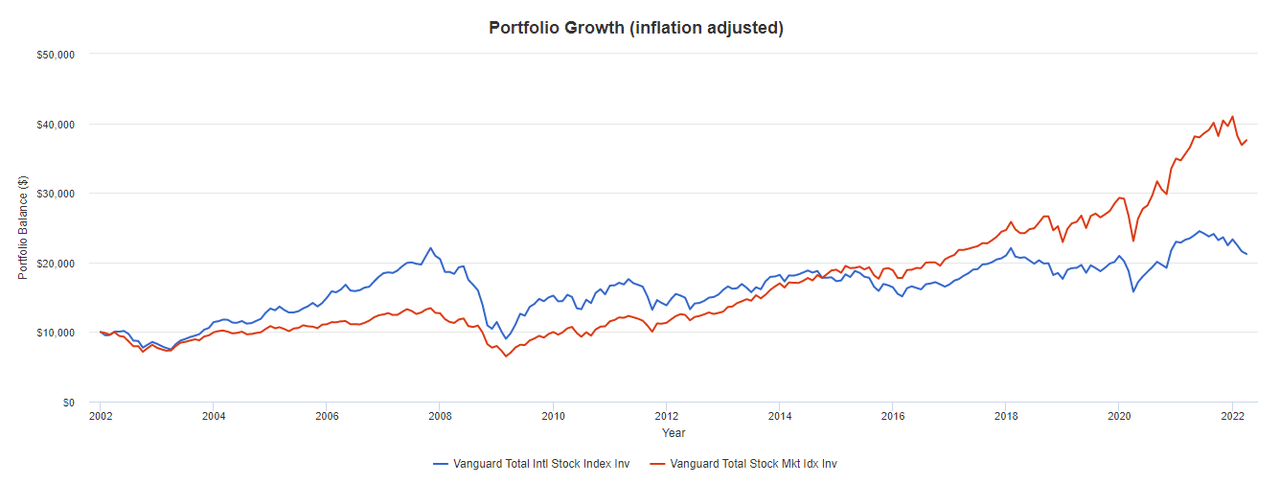

All things considered, it seems unlikely that returns will be this low forever. See, for example, the Portfolio Visualizer figure below charting the progress of $10,000 over the 20-year period spanning January 2002 to April 2022, using the oldest share classes of VXUS, in blue, and the Vanguard Total Stock Market Index Fund ETF (VTI), in red. Sometimes the U.S. markets are higher, and sometimes the ex-U.S. markets are higher. If history is any guide, ex-U.S. markets are bound to recover from their current slump, just as the U.S. markets recovered around 2015.

US and ex-US stocks have taken turns outperforming each other over the last 20 years. (Portfolio Visualizer)

As a basic reversion to the mean play, the return to trading at 16x earnings constitutes an immediate 33% return. With increasing globalization and free trade, we should expect valuations to soar even higher. U.S. stocks have already benefited from this, for example, with corporate profit margins rising in the years following the North American Free Trade Agreement and China’s inclusion into the World Trade Organization. Increasing valuations even partially explain recent U.S. overperformance, as the two started occurring at roughly the same time. There is no reason to believe that similar economic catalysts for foreign companies will not present themselves in the future, and thus improve their profit margins overseas as well.

Investing in VXUS can be thought of as a value play, and value plays are often scary because they tend to deal with struggling businesses that need to entice investors with high dividend yields. After all, there’s a reason why these stocks are cheaper than others, and it’s not because investors are eager to throw their money at them. That said, this is where money gets multiplied. Everyone has fantasies about purchasing Bitcoin early or stocking up on TSLA when it was at $50/share. How do we know that VXUS isn’t at similarly attractive prices? The ramp up back to the equity yield this fund deserves won’t be quick – that is the price we pay for diversification – but if we are to believe in the Siegel constant, then now is a great time to enjoy the ride.

Take Your Risk and Earn Your Reward

The past is bleak, the present is bleaker, and the future is uncertain. The world is feeling its way through the tribulations of novel and unforeseen global events. It is in moments like this where market risk is palpable, and where your risk premium is truly earned and deserved. After all, humans have always found a way past troubles, and stock markets have always recovered. I don’t know what the future holds, but I’m betting on success.

[ad_2]

Source links Google News