Just how significant of an effect higher rates will have will depend on how quickly the central bank moves

Article content

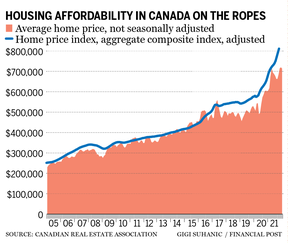

The era of ultra-low pandemic interest rates, which has helped drive Canadian home prices to all-time highs, may be coming to end.

Advertisement

This advertisement has not loaded yet, but your article continues below.

Article content

Many economists anticipate that the Bank of Canada will begin hiking its benchmark overnight rate as early as today, ushering in a pricier borrowing environment with potential implications for heavily indebted Canadians and the red-hot housing market.

Just how significant of an effect higher rates will have will depend on how quickly the central bank moves.

When the Bank of Canada raises the overnight rate, the prime rate banks use to lend will increase by the same amount.

Mortgage expert Rob McLister told the Financial Post that those holding variable-rate mortgages will be hit first, with the costs passed along between one day and one week following a rate hike.

McLister added that a 0.25 per cent rate increase, which is the amount the market is expecting as a first hike, would have no impact on qualifying since the minimum qualifying rate is already more than 235 basis points over five-year fixed rates.

Advertisement

This advertisement has not loaded yet, but your article continues below.

Article content

“For prospective prime borrowers, discounted five-year fixed rates would have to jump over 36 basis points for borrowers to start facing qualification challenges. And it would only be an issue for more highly indebted mortgage applicants (I’d estimate roughly 1 in 5 mortgage applicants),” McLister wrote in an e-mail.

It would only be an issue for more highly indebted mortgage applicants

Rob McLister

James Laird, co-founder of rate comparison site Ratehub.ca, also pointed to an immediate impact on variable rate holders.

“Their mortgage rate will increase, which will cause their mortgage payment to increase in February,” Laird said in a recent report.

The report further broke down the numbers, using an example of a homeowner who put 10 per cent down on a $700,000 home, close to the national average recently calculated by the Canadian Real Estate Association, with a five-year variable rate of 0.85 per cent over 25 years. The total mortgage would come to $649,530 with a monthly payment of $2,404.

Advertisement

This advertisement has not loaded yet, but your article continues below.

Article content

A 0.25 per cent rise would bring that variable rate up to 1.10 per cent and bring that monthly payment up to $2,477. Similarly, a 50-basis point hike would bring increase would raise the variable mortgage up to 1.35 per cent and pull the monthly payment up to $2,551, an increase of about $147 a month.

Fixed-rate mortgage holders will not see the same immediate impact, but those with upcoming mortgage renewals should be wary.

-

Investors are no more to blame for housing prices now than they were before

-

How the COVID-19 pandemic is changing commercial real estate

-

Concord loses appeal in dispute with Singapore tycoon over failed Vancouver waterfront deal

“Anyone who currently has a fixed-rate mortgage … should plan ahead and start to estimate and budget what their mortgage payments will be when their mortgage renewal comes up,” Laird said. “Depending on when each household entered their mortgage, today’s fixed rate might be higher than their current term’s rate.”

Advertisement

This advertisement has not loaded yet, but your article continues below.

Article content

The overnight rate sat at the effective lower bound of 0.25 per cent during the pandemic, pushing the national average home price up to a record $720,850 in November , according to data from the Canadian Real Estate Association (CREA). In March of 2020, that average stood at just $540,000.

McLister anticipates that over time, rate increases will cause the demand for housing to drop as buying becomes more expensive relative to renting, borrowers see their budgets stretched and mortgage qualification becomes more difficult. However, the first rate hike could see the opposite effect and spark a mini run on the market as buyers who have been on the fence rush to lock in lower rates.

“A small number of buyers will front-run future Bank of Canada hikes,” McLister wrote.

Advertisement

This advertisement has not loaded yet, but your article continues below.

Article content

A small number of buyers will front-run future Bank of Canada hikes

Rob McLister

John Pasalis, president and broker of record at Toronto-based housing data and brokerage firm Realosophy Realty, agrees that a series of aggressive rate increases would take some demand out of the market, though a modest 25-basis point hike likely won’t move the needle on housing demand.

“I don’t think a quarter (point) rate hike is going to have any material difference,” Pasalis told the Financial Post.

In Vancouver, Saretsky Group real estate specialist Steve Saretsky expects that rate hikes will largely hit the housing market in the latter half of the year as the increases work their way through the system.

“I’m looking towards rate hikes filtering through the housing market I think is probably an end-of-2022 story,” Saretsky said. “If you get three, four rate hikes … I think that’s probably where you start to see that (market slowdown).”

Advertisement

This advertisement has not loaded yet, but your article continues below.

Article content

Saretsky added that real estate investors are particularly vulnerable. Speculative investors were skittish at the outset of the pandemic, waiting to see where the market was headed before diving in later on. Research from the Bank of Canada late last year found that the number of investors taking out mortgages in the second quarter doubled on a year-over-year basis.

“I think is everybody’s well aware that the investor base plays a very significant role in the housing market today in terms of driving additional demand,” Saretsky said, and that the ability to carry mortgage payments is crucial.

“I think that ultimately buyers basically buy (mortgage) payments,” he said.

• Email: shughes@postmedia.com | Twitter: StephHughes95

Advertisement

This advertisement has not loaded yet, but your article continues below.