Our last fixed income insight focused on the 4 stages of the interest rate cycle. We conclude that we entered stage 3 at the end of the second quarter. Despite demonstrating that Treasury yields eventually tend to stabilize even as the Federal Reserve hikes aggressively – and outright decline during periods of earnings recession – many investors still don’t understand how RBA can be overweight long-term Treasuries given high inflation and our view that the Fed is nowhere close to a pivot*.

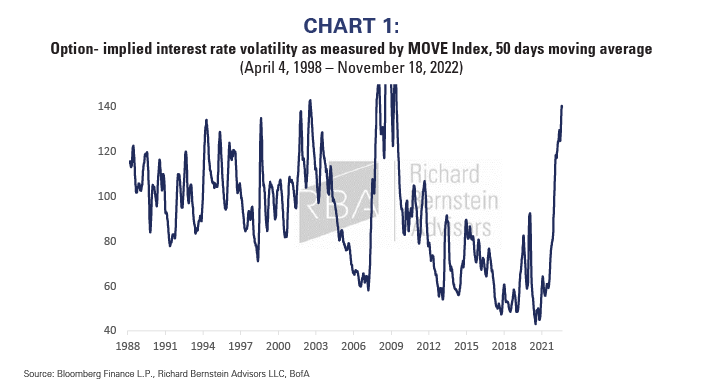

For all the concern about interest rates over the last several months, remember that on June 14th the 10-year yield hit what was then a cycle peak of 3.47%. The 10-year yield has stayed within 50bps of that June peak, apart from a few weeks. Although catching yields at their top would always be preferable, the unprecedented volatility and detachment from fundamentals have made that nearly impossible in 2022 (Chart 1).

Instead of trying to time the market, our process looks for inflection points that will drive medium to longer term performance. To this point, the times to really be worried about higher yields were in Stages 1 and 2 of the rate cycle (when we were very underweight duration) as the Fed tried to “hunt elephants with a pea shooter” and lost control of inflation expectations, growth and realized inflation (Chart 2). During this time, the 10-year yield increased 300bps from 0.5% on August 4th, 2020, to 3.5% on June 14th, 2022. Perhaps more astounding, 212bps of that increase, coinciding with a 15% loss in 7-10-year Treasuries, came in the 6 months between last December and June as the Fed hiked just 75bps and was still engaged in Quantitative Easing (QE).

Since June 14th, however, the Fed has engaged in massive Quantitative Tightening (QT) and has hiked 300bp with the market pricing in 100bp of additional increases. If periods of aggressive Fed action were the worst times to own long-term Treasuries, then such unprecedented hikes during this period should have led to massive losses. Instead, as of November 28th, the return of the 7-10-year Treasury index is just -0.1% since June 14th (Chart 3). How could this be the case?

Content continues below advertisement

Remember, the Fed hikes short-term interest rates to slow long-term growth and inflation. They also often continue to do so at a time even when growth begins to slow, many inflation measures have peaked, and an earnings recession is imminent. The reason for the hawkish tendency today is clear: The Fed is laser focused on two numbers: 3.7% (unemployment) and 7.7% (CPI) and cannot make the mistake of loosening policy prematurely. Consequently, the risk of recession continues to climb the longer employment remains tight and inflation elevated.

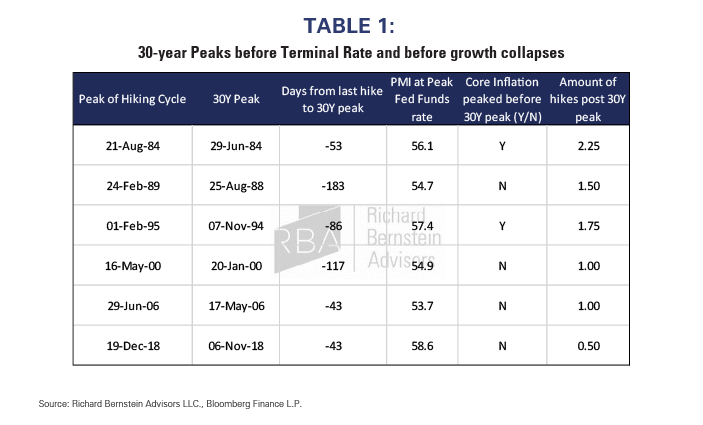

As a result, long-term Treasury yields tend to peak well before the rate hiking cycle concludes. Since the Fed began targeting the Fed Funds rate in 1982, on average, 30-year Treasury yields have peaked 3 months before the Fed reaches the terminal rate (Table 1). Further, on average the Fed hikes rates 133bps more after the 30-year yield peaks. The 30-year yield also tends to peak at a time when inflation is still near cyclical highs for that period, economic growth is slowing, and earnings are about to turn negative. This sounds awfully familiar to today’s macro environment.

If the 20-year yield falls by 150bps over the next 12 months – levels we last saw in April 2022 – the total return would equal 21%. What other investment has the potential to reward investors with a 20% return against a backdrop of an earnings recession and tightening liquidity? We think we are at a place where risk/reward is compelling for long-term Treasuries.

* In this case we define a pivot as going from tight policy, including holding the Fed Funds Rate at a high level, to cuts.

Michael Contopoulos

Director of Fixed Income

Please feel free to contact your regional portfolio specialist with any questions:

Phone: 212 692 4088

Email: sales@rbadvisors.com

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.