[ad_1]

As I wrote earlier this week, the S&P 500 has officially fallen to bear market levels. Rapid inflation across the economy has affected consumers and businesses, raising questions about spending and corporate profits.

These pressures have pushed interest rates higher across the curve, breaking a four-decade pattern of falling yields. This has prompted the Fed to tighten more aggressively, as evidenced by the 75 basis point rate hike this week. Altogether, these events have led investors to swiftly re-evaluate asset prices across financial markets, resulting in steep declines this year.

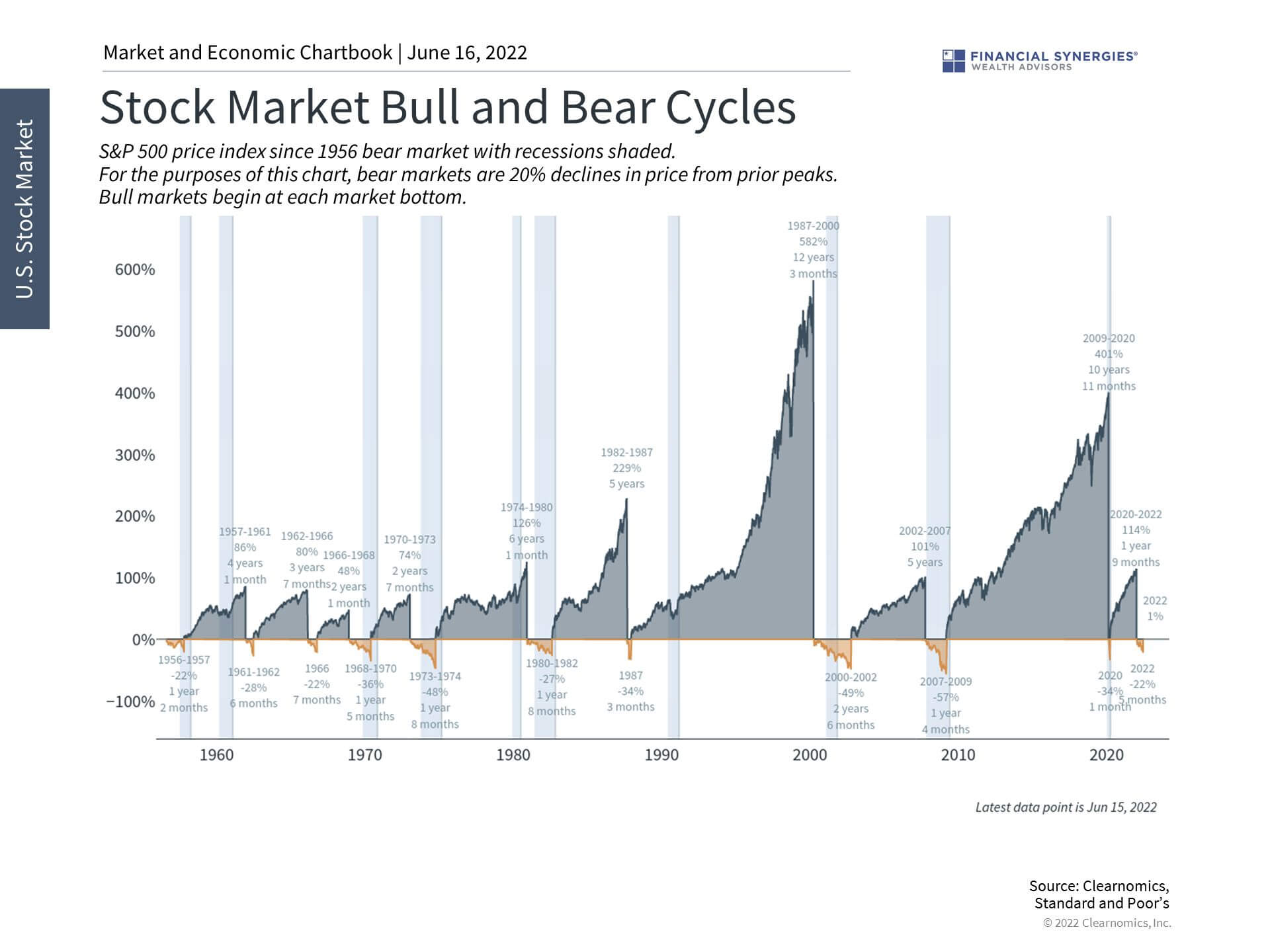

Markets have fallen into bear market territory

For all investors, this is a challenging period that can be financially and emotionally stressful. In times like these, it’s important to remember that staying patient and disciplined in times of market volatility is one of the core principles of long-term investing.

Should we be scared of the markets?

Cautious, yes. Wary, perhaps. Scared? No.

Here’s why:

- Many of the stocks leading the fall were high-flyers during the pandemic, so the pullback could be a healthy correction of overblown prices. And, overall, stocks are less risky now than they have been in years.

- Bear markets don’t last forever. On average, they tend to linger for roughly 15 months. However, the 2020 bear market only lasted 33 days. In addition, as you can see from the chart above, bull markets are much longer and more impactful than the bears.

- Half of the market’s best days have happened during a bear market, so we should expect some good days ahead.

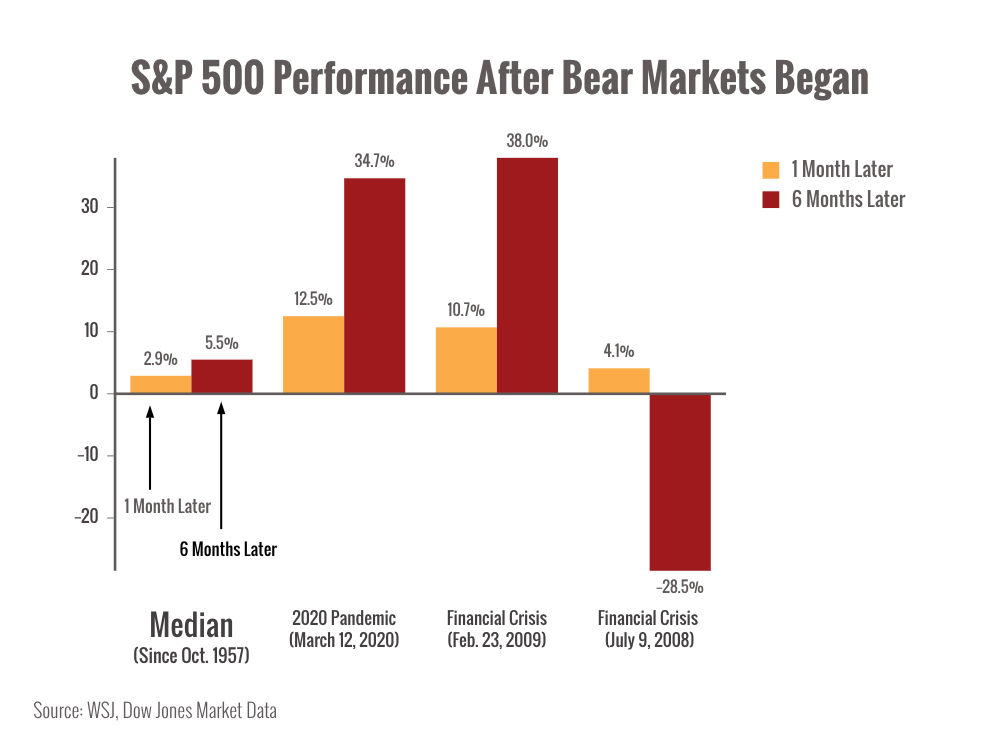

To give you some more historical perspective, here’s what happened during the last few bear markets:

You can see that in a couple of cases, markets bounced back within months. However, the 2008 bear market was a sustained pullback that lasted much longer.

Is history always an accurate predictor of the future? Not always. But we can look to it for hints about what may come.

Markets fluctuate on a regular basis in response to a variety of market, economic and geopolitical factors. Having the knowledge and experience to separate important changes in long-term trends from short-term reactions can help us to be positioned for future opportunities.

In The Intelligent Investor, Benjamin Graham, the father of value investing and Warren Buffet’s mentor, wrote a parable about a manic investor, “Mr. Market.” Every day, Mr. Market offers to buy or sell you stock at a price based not on the fundamental value of the asset but on his mood. In many cases, this mood is determined by what the stock has done in the past day or two, not by a more objective measure of what it is worth. It is up to you, as the more rational investor, to be disciplined and diligent in deciding if the price on any given day is attractive.

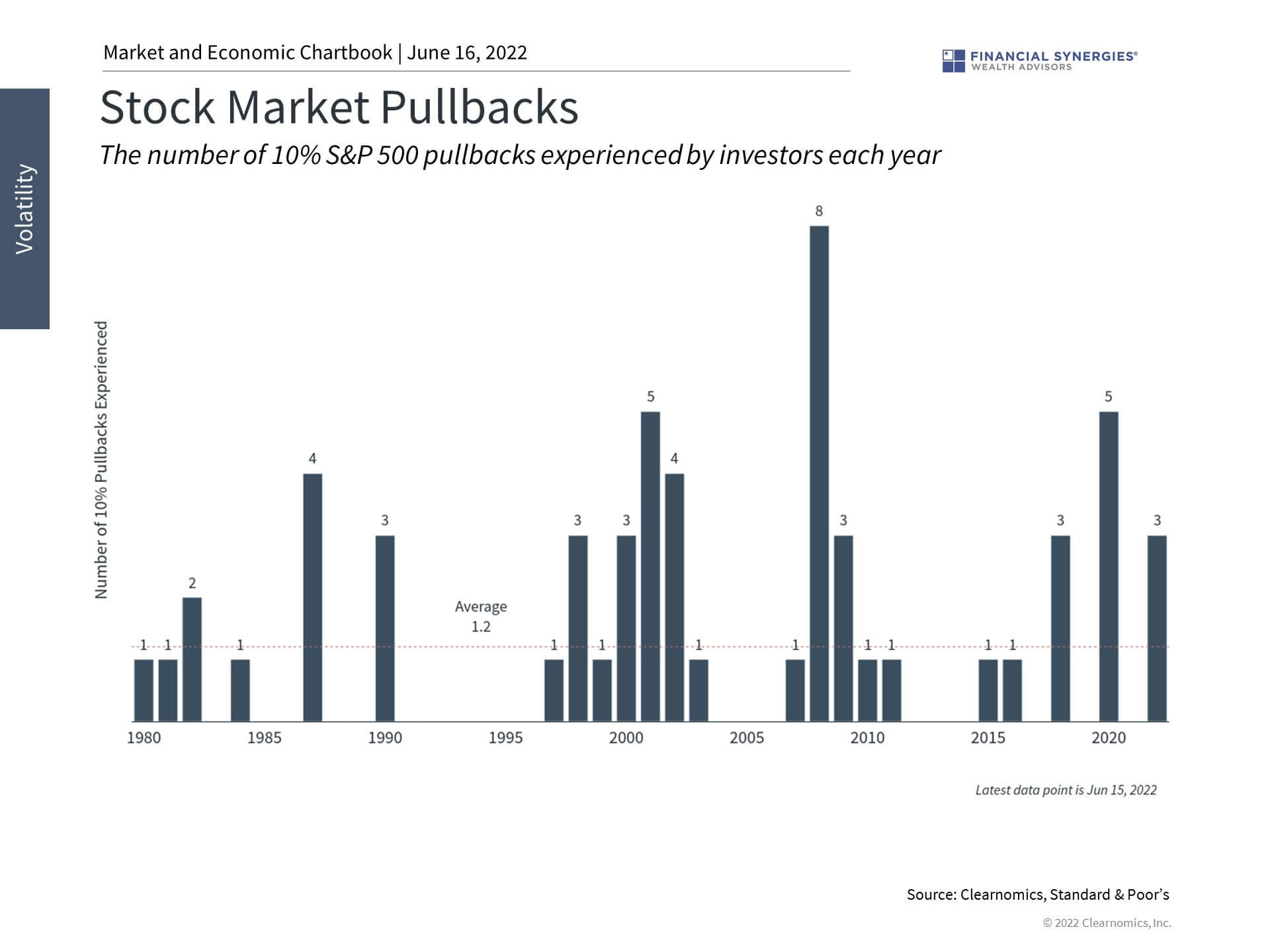

Stock market pullbacks and bear markets are normal

It’s straightforward to see that there may be days when Mr. Market has underpriced these assets, making it an attractive time to buy and hold. It’s the long-term investor who can decide what to do on any given day. In many cases, they could choose to ignore the price swings proposed by Mr. Market, especially if they have studied market history. This is true no matter how large the fluctuations or whether we assign them labels such as “correction” or “bear market.”

Unfortunately, it is human nature to be drawn to assets with prices that are rising and avoid ones that are falling. This is true even when this has little impact on what a stock may do next. The irony is that when stocks are the most attractively valued, investors want them the least. Recent price movements should have little bearing on what an asset is truly worth, so learning to overcome this bias takes time and experience. After all, many investors wish they had been more disciplined after the market began to recover in mid-2020.

The questions are always “what is priced in” and “what should be priced in.” Rising interest rates should prompt a re-evaluation of asset prices. In technical finance terms: the discount rate is higher today than it was even at the start of the year.

This means that the present value of future cash flows is lower, which disproportionately impacts investments with large uncertain payoffs in the distance. In simple terms: it’s hard to know what to pay today to receive $1 in the future because it’s very unclear how high interest rates may go.

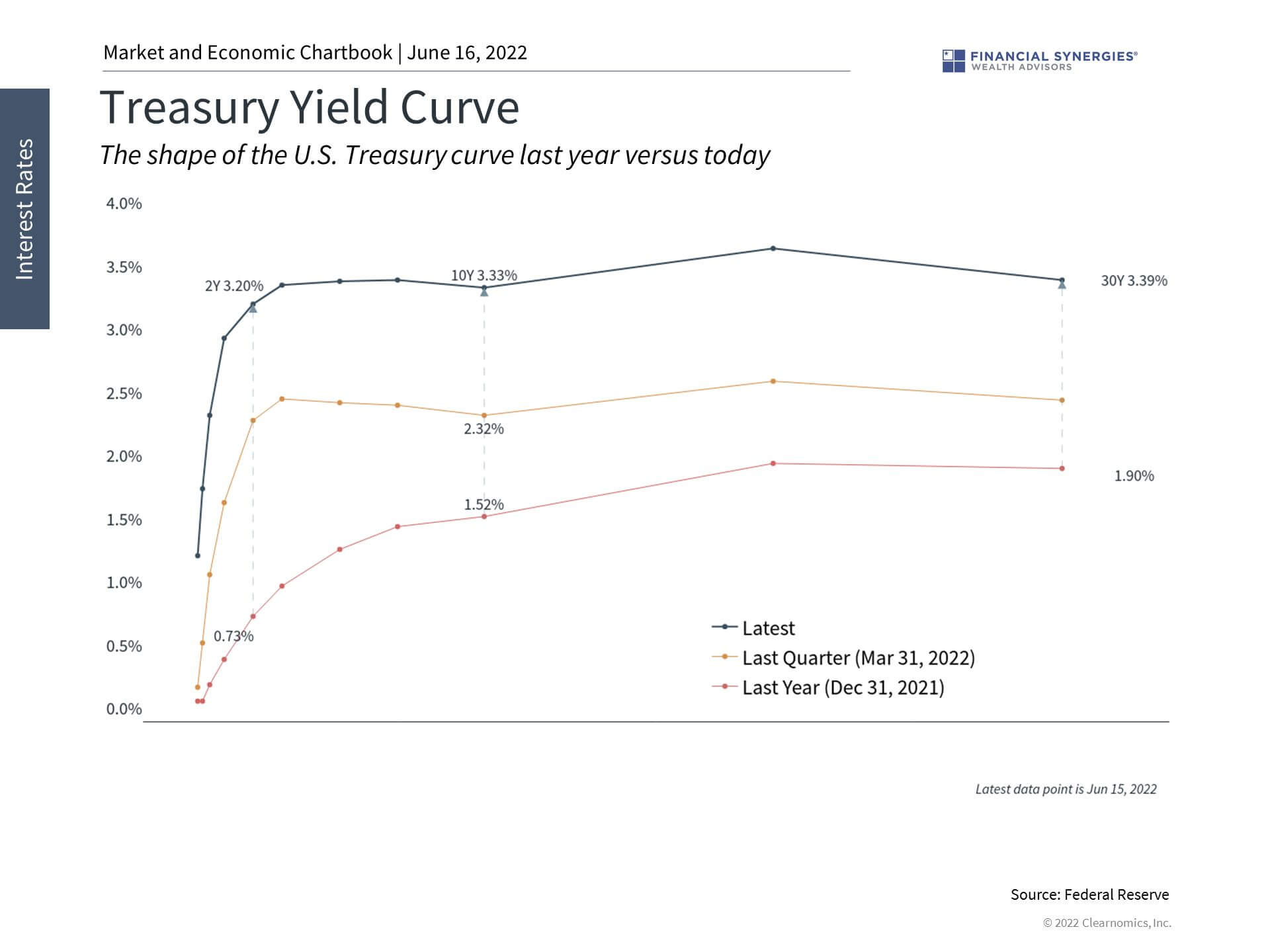

Interest rates have climbed steeply after falling for 40 years

At the same time, markets have been worried about these factors since inflation began to pick up a year and a half ago. Markets have been well ahead of the Fed which has, by their own admission, been behind the curve in responding to higher prices across the economy. It’s not difficult to argue that markets are pricing in the worst-case scenario of a Fed-induced recession in order to ease these price pressures. If this is the case, any unexpected slowing of inflation, e.g. if energy or food prices decline, would be viewed as positive for markets. This is especially true because the economy is, by many other measures, still strong.

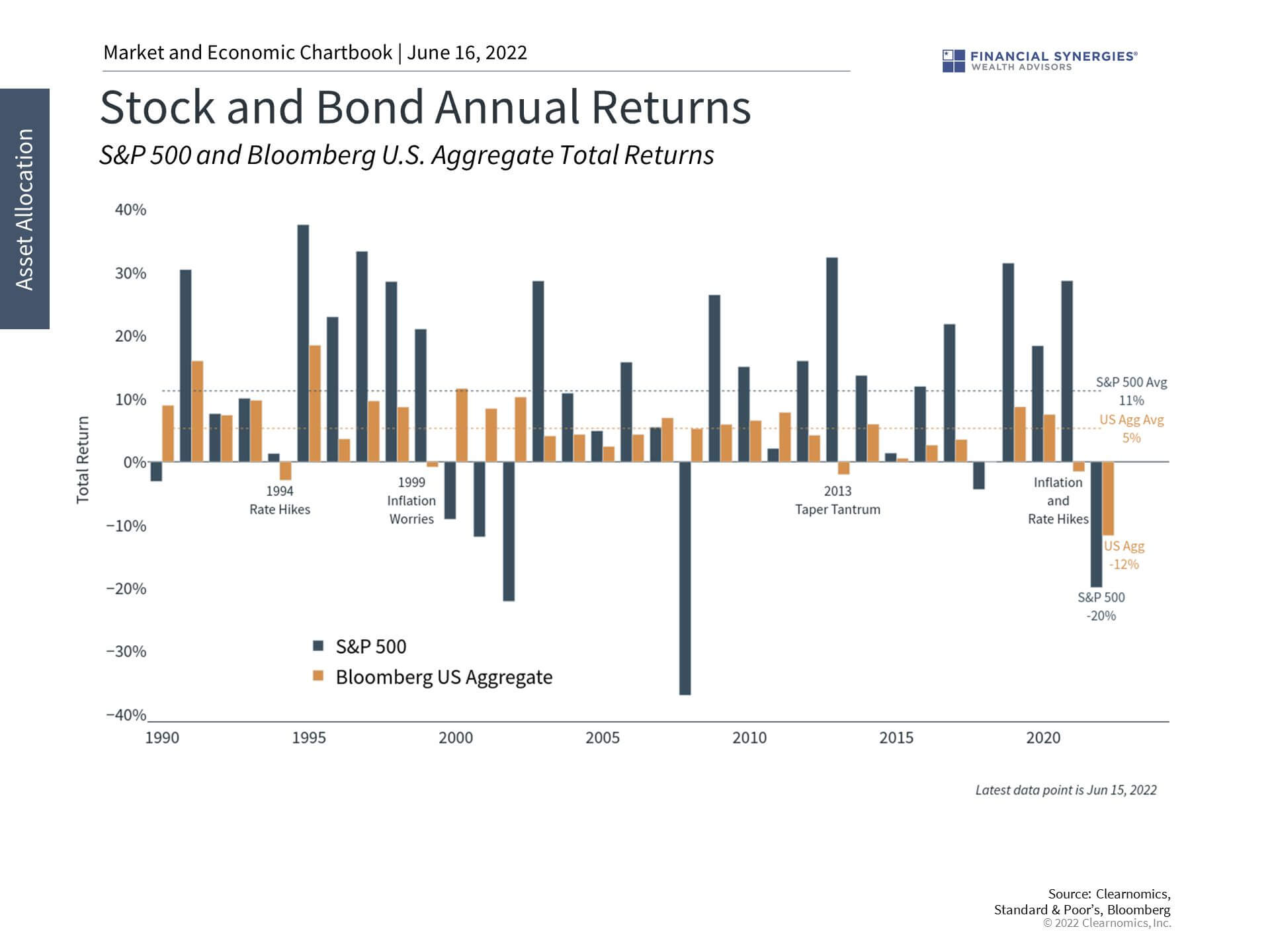

Perhaps what makes this bear market especially difficult is that nearly all asset classes have been impacted. It is unusual for stocks and bonds to be down at the same time, but this is in many ways a reversal of the “everything rally” of the previous two years, and arguably since the global financial crisis.

This is also because inflation has pushed interest rates higher which hurts bonds exactly when many investors needed them the most. Falling bond prices have occurred across several episodes over the past 30 years, during other periods of rising rates and inflation concerns, only to recover soon thereafter.

Both stocks and bonds have struggled this year due to rising interest rates

So, what next?

Obviously, don’t panic.

Markets will likely continue to be extremely volatile over the next weeks and months as investors digest the Fed’s aggressive rate hikes as well as concerns about an economic slowdown.

The latest estimates still don’t point to a recession in 2022, but that could change.

On the other hand, the next rounds of inflation data might show that prices are cooling off, which could give the Fed breathing room and avoid more aggressive hikes later.

We’ll have to wait and see.

As markets find a level and the inflation story evolves, we will maintain a long-term perspective. Although painful, market corrections and even bear markets are normal. Not only do markets historically recover, but this can happen when investors least expect it. Although the S&P 500 is 21% below its all-time high, it has experienced similar or fewer major pullbacks this year compared to 2020, 2018, 2009 (when the market was rapidly recovering), and throughout the early 2000s. While these were all difficult periods, the best course of action was to stay patient, hold a balanced portfolio, and avoid being unduly influenced by Mr. Market.

Source: Clearnomics

[ad_2]

Source links Google News